Operating Under a New Farm Bill and a Challenging Market

advertisement

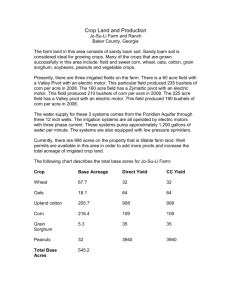

Operating Under a New Farm Bill and a Challenging Market Darren Hudson Larry Combest Chair of Agricultural Competitiveness Dept. Agricultural & Applied Economics Texas Tech University Presentation to COOP Directors Development Program February 9, 2009 Amarillo, TX Objectives • Look at new farm bill ACRE provision for Texas agricultural products • Examine some current trends in agricultural markets Some Background • Average Crop Revenue Election (ACRE) added as a program option for producers in 2008 Farm Bill. • Beginning with 2009 Crop, producers have option of selecting ACRE or CCP for each “farm” (FSA unit number) – Once the election to move to ACRE is made, cannot go back to CCP • Complex decision with many variables. – Ultimately about total farm income Some Background • ACRE is an average revenue guarantee based on two benchmarks—farm level and state level revenue • Provides a payment to farmers when: 1. State-level revenue for a commodity falls below the statelevel revenue guarantee AND 2. Farm-level revenue falls below that farm’s revenue benchmark. Key Differences Between ACRE and CCP Program CCP ACRE Loan Rate 52¢/lb 36.4¢/lb Direct Payment Rate 6.67¢/lb 5.336¢/lb Both payment programs (CCP and ACRE) are based on 83% of base acres for the 2009-2011 crops and 85% of base acres for the 2012 crop. Review of CCP Calculation Procedure n: o t t o C For For all commodities, the maximum CCP payment rate is when the market price is at or below the loan rate. For the case of cotton above, that is 12.6¢/lb. ACRE Calculations • The ACRE benchmark state yield is derived by finding the “Olympic year” average yield for the state: ACRE Calculations • ACRE State Revenue Guarantee – Average of 2 recent year’s MYA price X ACRE benchmark state yield X 90% • ACRE State Actual Revenue – State average yield per planted acre X the higher of MYA price or (0.7 X loan rate) State Level Trigger • If ACRE Actual State Revenue less than ACRE State Revenue Guarantee – All farmers in the state with that crop meet the first condition for receiving ACRE payments State Level Trigger--Cotton Year MYA Price State Yield (lb/ac) Olympic Average State Yield (lb/ac) State Revenue Guarantee ($/ac) State Actual Revenue ($/ac) Trigger Met? -----Irrigated----02/03 0.43 696.78 562.85 187.91 302.33 NO 03/04 0.60 454.40 578.43 268.13 270.91 NO 04/05 0.43 842.38 522.52 240.78 360.37 NO 05/06 0.47 918.26 578.06 234.35 434.43 NO 06/07 0.46 877.80 703.30 296.86 408.09 NO 07/08 0.57 1043.48 805.66 376.72 599.17 NO -----Dryland----02/03 0.43 200.46 236.30 78.89 115.85 NO 03/04 0.60 349.86 220.06 102.01 187.94 NO 04/05 0.43 121.65 262.08 120.77 215.65 NO 05/06 0.47 316.36 262.08 106.25 251.35 NO 06/07 0.46 216.06 362.11 152.84 81.57 YES 07/08 0.57 219.06 362.11 169.32 382.80 NO State Level Trigger--Sorghum Year MYA Price State Yield (lb/ac) Olympic Average State Yield (lb/ac) State Revenue Guarantee ($/ac) State Actual Revenue ($/ac) Trigger Met? -----Irrigated----02/03 4.14 72.70 71.77 245.44 300.98 NO 03/04 4.26 66.00 71.30 269.51 281.16 NO 04/05 3.19 77.40 69.90 234.34 246.91 NO 05/06 3.33 85.90 70.00 205.38 286.05 NO 06/07 5.88 78.00 72.87 302.00 458.64 NO 07/08 6.95 88.00 76.03 438.98 611.60 NO -----Dryland----02/03 4.14 45.50 53.53 183.08 188.37 NO 03/04 4.26 49.00 50.13 189.50 208.74 NO 04/05 3.19 59.00 51.37 172.21 188.21 NO 05/06 3.33 54.60 51.17 150.12 181.82 NO 06/07 5.88 40.00 49.70 205.98 235.20 NO 07/08 6.95 60.00 49.70 286.94 417.00 NO State Level Trigger--Wheat Year MYA Price State Yield (lb/ac) Olympic Average State Yield (lb/ac) State Revenue Guarantee ($/ac) State Actual Revenue ($/ac) Trigger Met? -----Irrigated----02/03 3.56 38.80 49.17 140.27 138.13 YES 03/04 3.40 46.30 48.23 151.07 157.42 NO 04/05 3.40 46.20 47.00 143.82 157.08 NO 05/06 3.42 49.10 44.83 137.59 167.92 NO 06/07 4.26 35.00 47.20 163.12 149.10 YES 07/08 6.65 56.00 43.77 214.87 372.40 NO -----Dryland----02/03 3.56 26.10 29.20 83.31 92.92 NO 03/04 3.40 23.10 29.20 91.45 78.54 YES 04/05 3.40 26.90 27.37 83.74 91.46 NO 05/06 3.42 27.90 26.60 81.64 95.42 NO 06/07 4.26 19.00 26.97 93.20 80.94 YES 07/08 6.65 33.00 25.37 124.54 219.45 NO State Level Trigger--Corn Year MYA Price State Yield (lb/ac) Olympic Average State Yield (lb/ac) State Revenue Guarantee ($/ac) State Actual Revenue ($/ac) Trigger Met? -----Irrigated----02/03 2.32 187.40 167.80 323.94 434.77 NO 03/04 2.42 180.70 172.83 368.65 437.29 NO 04/05 2.06 193.00 178.20 359.25 397.58 NO 05/06 2.00 179.00 182.37 333.18 358.00 NO 06/07 3.04 179.00 182.37 413.61 544.16 NO 07/08 4.00 200.00 184.23 583.65 800.00 NO -----Dryland----02/03 2.32 64.80 82.90 160.04 150.34 YES 03/04 2.42 73.30 75.73 161.54 177.39 NO 04/05 2.06 92.50 78.57 158.39 190.55 NO 05/06 2.00 70.60 78.93 144.21 141.20 YES 06/07 3.04 72.00 73.30 167.15 218.88 NO 07/08 4.00 99.00 71.97 227.99 396.00 NO Example of Cotton Farms Cotton Production Type Base Acres Payment Yield (lb/ac) Irrigated (Farm 1) 121.2 411 Irrigated (Farm 2) 120.3 398 Dryland (Farm 3) 18.3 134 Dryland (Farm 4) 32.6 166 Farm Level ACRE Analysis—Irrigated Year Actual Farm Yield (lb/ac) Five Year Olympic Avg. Farm Yield (lb/ac) ACRE Farm Benchmark Revenue ($/ac) Actual Farm Revenue ($/ac) Second Trigger Met? ----------Farm 1---------02/03 672.00 518.00 203.26 291.58 NO 03/04 0.00 569.33 304.41 0.00 YES 04/05 1098.00 408.33 222.73 469.72 NO 05/06 1016.00 460.67 218.62 480.67 NO 06/07 737.00 574.33 283.67 342.63 NO 07/08 25.00 808.33 434.43 14.36 YES ----------Farm 2---------02/03 703.00 518.00 204.31 305.03 NO 03/04 0.00 348.33 191.57 0.00 YES 04/05 1036.00 410.00 190.70 443.20 NO 05/06 942.00 237.33 197.03 445.66 NO 06/07 578.00 579.67 273.66 268.71 YES 07/08 910.00 659.33 399.98 522.52 NO Farm Level ACRE Analysis—Dryland Year Actual Farm Yield (lb/ac) Five Year Olympic Avg. Farm Yield (lb/ac) ACRE Farm Benchmark Revenue ($/ac) Actual Farm Revenue ($/ac) Second Trigger Met? ----------Farm 1---------02/03 216.00 276.33 116.13 93.72 YES 03/04 0.00 234.00 132.62 0.00 YES 04/05 1141.00 234.00 134.89 488.12 NO 05/06 1181.00 234.00 116.99 558.73 NO 06/07 158.00 534.67 265.55 73.45 YES 07/08 0.00 505.00 277.16 0.00 YES ----------Farm 2---------02/03 0.00 103.00 51.54 0.00 YES 03/04 427.00 103.00 70.02 254.58 NO 04/05 0.00 108.33 55.47 0.00 YES 05/06 609.00 74.00 47.89 288.12 NO 06/07 13.00 182.00 97.96 6.04 YES 07/08 616.00 146.67 89.29 353.71 NO Average Revenue Analysis Farm Farm Revenue Under CCP Farm Revenue Under ACRE Average % Difference Farm 1 (Irrigated) 44,748 34,416 30% Farm 2 (Irrigated) 52,116 41,772 25% Farm 3 (Dryland) 4,889 3,949 24% Farm 4 (Dryland) 5,671 5,220 9% Average farm revenue over the 2002-2008 period under either the ACRE or CCP programs, with all other farm program payments included. The averages are significantly different, indicating higher average returns for CCP. The variances are not significantly different, indicating that CCP is no more risky (in terms of revenue) than ACRE. Upshot • ACRE not a particularly appealing alternative for Texas agriculture. • State size means state average “masks” a lot of underlying heterogeneity in state yields. • Geographic diversity in state agriculture limits correlation between farm and state level yields. A View of the Markets A View of the Market A View of the Markets Relative Prices Corn Price Cotton Price 6.00 0.70 4.05 0.55 Ratio Month = 8.57 Sep = 5.36 Dec Although the absolute prices still favor corn, the relative price differences have moderated some. Water Requirements Ethanol Ethanol Ethanol Source: Revised Renewable Fuel Standard for 2008, Issued Pursuant to Section 211(o) of the Clean Air Act as Amended by the Energy Independence and Security Act of 2007. Federal Register 73, 31(Feb. 2008):8665‐8667. Ethanol Ethanol Capacity is now above RFS. Anecdotal evidence suggests that plant building cost was somewhere around $2/gal capacity in 2007 and now auctions of bankrupt plants cannot meet minimum bids of $0.80/gal capacity Ethanol Conclusions • ACRE is not a likely program choice for most Texas agricultural producers • Water/drought situation points toward more alternative crops than corn; business risk puts pressure on cotton plantings • RFS has created a structural shift in corn (and, by consequence, other markets), but we have about maxed out the impact of RFS without further expansion of mandate • Farm safety net remains strong and farm economy appears to be weathering economic downturn reasonably well