University of Oslo, Department of Economics

Ragnar Nymoen, 4 February 2008

Norwegian inflation forecasts, January 2008

This is the eight of a sequence of forecasts of the Norwegian rate of inflation, using a small scale

econometric model to produce automatized inflation forecasts, AIFs. The approach taken, and

model used, is the same as has been useful in analyzing the failure affecting Norges Bank's

inflation earlier forecasts, see Nymoen (2005).

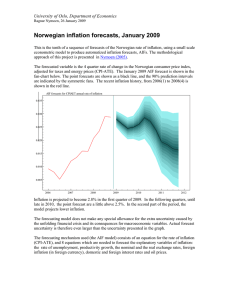

The forecasted variable is the 4 quarter rate of change in the Norwegian consumer price index,

adjusted for taxes and energy prices (CPI-ATE). The forecast based on the end of January 2008

version of the AIF model is shown in the fan-chart below. The point forecasts are shown as a

thick blue line, and the 90% prediction intervals are indicated by the symmetric fans. Based on

the AIF forecasting model, future inflation rates inside this narrower interval are more likely

events than inflations rates outside the narrower forecast band. The recent inflation history, from

2004(1) to 2007(4) is shown by the red line.

0.040

AIF forecast 4 February 2008. Rate of inflation (CPI−AET)

0.035

0.030

0.025

0.020

0.015

0.010

0.005

2004

2005

2006

2007

2008

2009

2010

2011

Inflation is projected to increase in the first three quarters of 2008. For most of the forecast

period the point forecast is between 2% and 2.5%. Late in the period the forecasted rate of

inflation is decreasing. The estimated uncertainty allows for inflation both higher and lower than

the 2.5% inflation target. Towards the end of the forecast horizon, inflation below 2.5% is

regarded by the model as more likely than inflation above 2.5% though.

The forecasting mechanism used (the AIR model) consists of an equation for the rate of inflation

(CPI-ATE), and 8 equations which are needed to forecast the following variables: the (logarithm

of the) rate of unemployment, productivity growth, the nominal and the real exchange rates,

foreign inflation (in foreign currency), domestic and foreign interest rates and oil prices.

University of Oslo, Department of Economics

Ragnar Nymoen, 4 February 2008

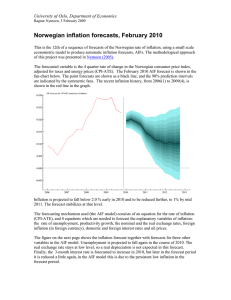

The figure on this page shows the nominal 3 month interest rate (money market rate) which is

forecasted together with inflation and the other variables in the AIF forecasting model. Over the

2008-2010 period as a whole, there is no significant rise in the forecasted interest rate, although

the point forecast shows a continuation of the increases from 2006 and 2007, but in smaller steps.

AIF forecasts 4 February 2008. The 3−month nominal interest rate

0.10

0.09

0.08

0.07

0.06

0.05

0.04

0.03

0.02

2004

2005

2006

2007

2008

2009

2010

2011

0

0