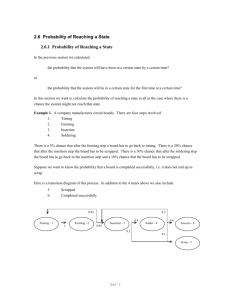

Markov Chains

advertisement

Markov Chains

Definition, Chapman-Kolmogorov Equations,

Classification of States, Limiting Probabilities,

Transient Analysis, Time Reversibility

Chapter 4

1

Stochastic Processes

A stochastic process is a collection of random variables

X t , t T

Typically, T is continuous (time) and we have X t , t 0

Or, T is discrete and we are observing X n , n 0,1, 2,...

at discrete time points n that may or may not be evenly spaced.

Refer to X(t) as the state of the process at time t.

The state space of the stochastic process is the set of all

possible values of X(t): this set may be discrete or

continuous as well.

Chapter 4

2

Markov Chains

In this chapter, consider discrete-state, discrete-time:

A Markov chain is a stochastic process X n , n 0,1, 2,...

where each Xn belongs to the same subset of {0, 1, 2, …},

and P X n1 j X n i, X n1 in1 ,..., X 1 i1 , X 0 i0 P X n1 j X n i

for all states i0, i1,…, in-1 and all n 0 .

Say Pij P X n 1 j X n i

Then Pij 0 for all i, j

For any i, Pij 1

j 1

Let P Pij

be the matrix of one-step transition probabilities.

Chapter 4

3

n-step Transition Probabilities

Given the chain is in state i at a given time, what is the

probability it will be in state j after n transitions? Find it by

conditioning on the initial transition(s).

Pijn P X m n j X m i

P X m n j X m i, X m 1 k P X m 1 k X m i

k 0

P X m n j X m 1 k P X m 1 k X m i

k 0

Pkjn 1 Pik

k 0

Chapter 4

4

Chapman-Kolmogorov Equations

In general, can find the n-step transition probabilities by

conditioning on the state at any intermediate stage:

Pijn m P X n m j X 0 i

P X n m j X n k , X 0 i P X n k X 0 i

k 0

Pkjm Pikn

k 0

Let P(n) be the matrix of n-step transition probabilities:

P

n m

n m

P P

So, by induction, P n P n

Chapter 4

5

Classification of States

State j is accessible from state i if Pij 0 for some n 0

If j is accessible from i and i is accessible from j, we say that

states i and j communicate (i j).

Communication is a class property:

(i) State i communicates with itself, for all i 0

(ii) If i communicates with j then j communicates with i

(iii) If i j and j k, then i k.

Therefore, communication divides the state space up into

mutually exclusive classes.

If all the states communicate, the Markov chain is irreducible.

n

Chapter 4

6

Recurrence vs. Transience

Let fi be the probability that, starting in state i, the process will

ever reenter state i. If fi = 1, the state is recurrent, otherwise

it is transient.

If state i is recurrent then, starting from state i, the process

will reenter state i infinitely often (w/prob. 1).

If state i is transient then, starting in state i, the number of

periods in which the process is in state i has a geometric

distribution with parameter 1 – fi.

n

P

Or, state i is recurrent if n1 ii

and transient if n1 Piin

Recurrence (transience) is a class property: If i is recurrent

(transient) and i j then j is recurrent (transient).

A special case of a recurrent state is if Pii = 1 then i is absorbing.

Chapter 4

7

Recurrence, Transience and Other Properties

Not all states in a finite Markov chain can be transient (why?).

All states of a finite irreducible Markov chain are recurrent.

If Piin 0 whenever n is not divisible by d, and d is the largest

integer with this property, then state i is periodic with

period d.

If a state has period d = 1, then it is aperiodic.

If state i is recurrent and if, starting in state i, the expected

time until the process returns to state i is finite, it is

positive recurrent (otherwise it is null recurrent).

A positive recurrent, aperiodic state is called ergodic.

Chapter 4

8

Limiting Probabilities

Theorem: For an irreducible ergodic Markov chain, p j lim Pijn

n

exists for all j and is independent of i. Furthermore, pj is

the unique nonnegative solution of

p j p i Pij , j 0

i 0

p

j 0

j

1

The probability pj also equals the long run proportion of

time that the process is in state j.

If the chain is irreducible and positive recurrent but

periodic, the same system of equations can be solved for

these long run proportions.

Chapter 4

9

Limiting Probabilities 2

The long run proportions pj are also called stationary

probabilities because if P X 0 j p j

then P X n j p j for all n, j 0

Let mjj be the expected number of transitions until the

Markov chain, starting in state j, returns to state j (finite if

state j is positive recurrent). Then m jj 1 p j

If X n , n 0 is an irreducible Markov chain with stationary

probabilities , and r is a bounded function on the state

space. Then with probability 1,

lim

N

N

n 1

r Xn

N

r j p j

j 0

Chapter 4

Long run

average reward

10

Transient Analysis

Suppose a finite Markov chain with m states has some

transient states. Assume the states are numbered so that T

= {1, 2, …, t} is the set of transient states, and let PT be the

matrix of transition probabilities among these states.

Let R be the t x (m-t) matrix of one-step transition

probabilities from transient states to the recurrent states and

PR be the (m-t) x (m-t) matrix of transition probabilities

among the recurrent states: the overall one-step transition

probability matrix can be written as

PT R

P

0

P

R

If the recurrent states are all

absorbing then PR = I.

Chapter 4

11

Transient Analysis 2

• If the process starts in a transient state, how long does it

spend among the transient states?

• What are the probabilities of eventually entering a given

recurrent state?

Define dij = 1 if i = j and 0 otherwise.

For i and j in T, let sij be the expected number of periods that

the Markov chain is in state j given that it started in state i.

T

sij d ij Pik skj

k 1

Condition on the first transition,

and note that transitions from recurrent

states to transient states are impossible

Chapter 4

12

Transient Analysis 3

Let S be the matrix of sij values. Then S = I + PTS. Or,

I PT S I

1

S I PT

For i and j in T, let fij be the probability that the Markov chain

ever makes a transition into j, starting from i. f sij d ij

ij

s jj

For i in T and j in Tc, the matrix of these probabilities is

1

F I PT R

Chapter 4

13

Time Reversibility

• One approach to estimate transition probabilities from each

state is by looking at transitions into states and tracking what

the previous state was.

– How do we know this information is reliable?

– How do we use it to estimate the forward transition probabilities?

Consider a stationary ergodic Markov chain.

Trace the sequence of states going backwards: Xn, Xn-1,…, X0

This is a Markov chain with transition probabilities:

p j Pji

Qij P X m j X m1 i

pi

If Qij = Pij for all i, j, then the Markov chain is time reversible.

Chapter 4

14

Time Reversibility 2

Another way of writing the reversibility equation is:

p i Qij p j Pji

Proposition: Consider an irreducible Markov chain with

transition probabilities Pij. If one can find positive numbers

pi summing to 1 and a transition probability matrix Q such

that the above equation holds for all i, j, then Qij are the

transition probabilities for the reversed chain and the pi are

the stationary probabilities for both the original and the

reversed chain.

Use this, thinking backwards, to guess at transition

probabilities of reversed chain.

Chapter 4

15