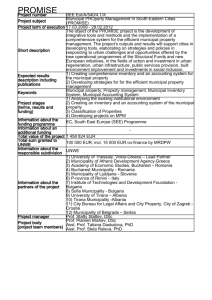

FINANCE DIRECTORATE,

SHAREHOLDING MANAGEMENT DEPARTMENT

MUNICIPAL ENTITY

QUARTERLY NEWSLETTER

Analyst

2008/2009 Quarter 1: 1 July 2008 – 30 September 2008, ISSUE NO. 06

As parent municipality to the municipal entities we aim to keep our municipal entity boards of

directors and staff abreast of all current news, legislation and policies directly affecting the

municipal entities. This will enable directors to be continuously informed as well as ensuring that

we meet the legislative requirement as parent municipality to ensure that both the municipality and

the municipal entity comply with the Municipal Systems Act, the Local Government: Municipal

Finance Management Act and any other applicable legislation.

Contents

The newsletter’s intend to convey information relating to the Local Government: Municipal Finance

Management Act, Local Government: Systems Act, Companies Act, Corporate Governance and any

information relevant to municipal entities.

THE LOCAL GOVERNMENT LEGISLATION:

THE MUNICIPAL FINANCE MANAGEMENT ACT:

Municipal Asset Transfer Regulations

National Treasury has promulgated Municipal Asset Transfer Regulations for

municipalities and municipal entities. The Regulations came into force on the

1 September 2008 and sets out the procedural requirements for both the sale and

lease of municipal entity owned capital assets. The Regulations also govern the

process for the transfer of capital assets between a municipality and its municipal

entities. The Regulations are onerous and need to be studied closely to ensure

compliance. A copy of the regulations is available at the National Treasury website:

http://www.treasury.gov.za/legislation/mfma/reg_gaz/1-31346%20228%20Nat%20Treas.pdf

Directors and Trustees bidding for an award by the City

Issue 4 of the Quarterly Newsletter dealt with the exemption of Regulation 44 of the

Supply Chain Regulations. The exemption allows a municipality to make an award to

a non executive director of a municipal entity. A municipal entity may make an award

to a director of another municipal entity (a municipal entity may not make an award

to one of its own directors). It is a requirement that a bidder disclose:

1. that he/she serves on the board of a municipal entity

2. that he/she serves as a executive or non executive board member

1

3. the name of the municipal entity

If the bidder is not a natural person, then the name of any director, manager or

principal shareholder, who is a municipal entity director, must be disclosed.

These requirements pertain to Trustees as well.

New Budget Formats Guide

National Treasury has issued Budget Format Guides. One of the specific aims of the

budget formats guide is to ensure that a municipal entity will approve a budget on

the similar basis to its parent municipality in order to achieve effective financial

control. As the parent municipality and its municipal entities apply the same

accounting standards and budget, this will further assist in the consolidation of the

Annual Financial Statements.

The guidelines are available on the National Treasury Website at the following link:

http://www.treasury.gov.za/legislation/mfma/guidelines/budget%20formats/

default.aspx

Budget Submission 2009/2010

Section 87 of the MFMA mainly governs the preparation of the budget of a municipal

entity. It starts off by placing the responsibility on the board of directors or trustees

to submit a proposed budget for the entity to the parent municipality, not later than

150 days before the start of the entity’s financial year. This date may even be sooner

upon request by the parent municipality. Working this timeframe back to the

calendar means that the proposed budget must be submitted to the City by the end

of January of a particular year. It should however reach the City in time to be

included in the report submission process to Council. This starts early in the month of

January, as it needs to pass through various portfolio committees and the Mayoral

Committee before it is presented to Council. Therefore, the City requests that the

proposed budget reaches the City by no later than approx. 6 January 2009. The

practical implication of this is that with December being a holiday period, such a

proposed budget should be approved by the directors / trustees by the beginning of

December.

Section 87(5)(d) requires that the budget of a municipal entity must include a multiyear business plan for the entity that –

(i) set key financial and non-financial performance objectives and measurement

criteria as agreed with the parent municipality;

(ii) is consistent with the budget and integrated development plan (IDP) of the

entity’s parent municipality;

(iii) is consistent with any service delivery agreement (SDA) or other agreement

between the entity and the entity’s parent municipality; and

(iv)reflect actual and potential liabilities and commitments, including particulars of

any proposed borrowing of money during the period to which the plan relates.

Therefore, besides the budget, the business plan is a major document of importance

to the City, both of which take a long time to prepare. That is why the City on

commencement of the new financial year, immediately starts with the preparation of

the following years’ budget. It is important to note the various documents of the City

such as the IDP or SDA’s, must be considered when preparing the business plan.

2

Section 87(5)(e) also requires that the budget must comply with section 17(1) and

(2) of the MFMA. Section 17(1) requires that the budget must be in the format as

prescribed by National Treasury. This format was changed recently by National

Treasury (see relevant article elsewhere in the newsletter). The changes are

substantial and will require proper planning and systems will need to be altered to

cater for the changes. The idea is however that the budget forms the starting point

for eventual reporting in the annual financial statements.

The central message to this article which we want to convey to you is therefore:

PLEASE START EARLY WITH YOUR 2009/10 BUDGET!

GENERAL:

Matters of Interest

Non Executive Directors Winter 2008 Report has been completed by

PriceWaterhouseCoopers. The report deals with best practices for non executive

director fees. The report may be found at:

http://www.pwc.com/za/eng/pdf/pwc_ned_winter_2008_report.pdf

Note: The PDF file is 3.88MB

Please contact Louise Muller (021 4003940) or Richard Wootton (021 4002701) if you have any

queries in respect of this newsletter.

Although every effort is made to check the accuracy and quality of the information supplied, The

City cannot be held responsible for any errors that may arise.

Copyright(c) City of Cape Town 2007. All rights reserved. No part of this newsletter may be reproduced or transmitted in any form

without written permission from the City of Cape Town, Finance Directorate, Shareholding Management Department.

3