Health Reimbursement Arrangements (HRAs)

advertisement

")

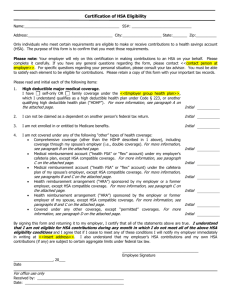

WELCOME ! CPP/FPC Study Group Please sign in ! Presentation Material Review Test Questions ? THE EXAM ? Any Questions ? Concerns ? Health and Accident Benefits Section 4 Health Insurance Plans • Traditional health insurance – Fee for service arrangement • • • • HMO – Health Management Organizations POS – Point of Service PPO – Preferred Provider Organizations Tax Treatment of Contributions Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision Overview Who is eligible to set up an account? (Archer) MSA An MSA is a taxexempt trust or custodial account established for the purpose of paying medical expenses in conjunction with a high-deductible health plan. Self-employed persons and businesses with 50 or fewer employees. Health Savings Accounts (HSA) A tax-exempt trust or custodial account created to pay for the qualified medical expenses of the account holder and his or her spouse or dependents. Health Reimbursement Arrangements (HRAs) An employer funded account that reimburses employees for qualified medical care expenses. Individuals and An employee whose families covered only employer offers an under a qualified HRA. high-deductible health insurance plan. Certain “excepted” plans are permissible (e.g. dental, vision). Health Care Flexible Spending Accounts (FSAs) An employersponsored benefit program under which employees received reimbursement for qualified medical expenses. An employee whose employer offers a health care FSA option. Summary Comparison of HSAs – FSAs – HRAs - MSAs Medical Savings Provision Account MSA Qualified highWhat are the deductible health requirements for the corresponding plan insurance: health plan? For 2011 self only deductible of $2,050$3,050 with an outof-pocket maximum of not more than $4,100; Family deductible must be between $4,100-$6,150 with an out-of-pocket maximum of not more than $7,500. 1Amounts to increase by CPI-U. Health Savings Accounts (HSA) Qualified highdeductible health insurance: For 2011 self-only deductible must be at least $1,200 with an out-of-pocket maximum of not more than $5,950; family deductible must be at least $2,400 with an out4of-pocket maximum of not more than $11,900.1 Plan can provide first-dollar coverage of preventive care. Health Reimbursement Arrangements (HRAs) No health plan requirements. Health Care Flexible Spending Accounts (FSAs) No health plan requirements. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision Do the uniform coverage and 12month election rules apply to the account? MSA Employee and employer, but both cannot contribute in the same year. Who may contribute to the Account? Individual: 65% of Deductible Family: 75% of Deductible Contributions to an MSA can be made in cash in a lump sum at the beginning of the year. Health Savings Accounts (HSA) No. Employer or employee or both. Generally will be the account holder (including salary reduction) or the employer or both. Health Reimbursement Health Care Arrangements Flexible Spending (HRAs) Accounts (FSAs) Not for the HRA. Yes. Applies to high deductible health coverage funded by salary reduction by the employee. Solely the employer. The account holder, employer or both. Usually funded by employees, who choose to salary reduce a certain amount of their pay in an FSA account. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision What are the limits on contributions? MSA Individual = 65% of deductibles Family = 75% of deductible Health Reimbursement Health Savings Arrangements Accounts (HSA) (HRAs) Up to 100 percent of No federal income the deductible tax law limits. amount of the Employers typically accompanying high- set limits, usually deductible health equal to or less than insurance policy. The the amount of the max for 2011 is deductible of $3,050 for self only employees’ health coverage and plan. $6,150 for family coverage. . Health Care Flexible Spending Accounts (FSAs) No limits under federal income tax law. Employers typically set limits. Salary Reductions capped at $2,500 starting in 2013. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision What are qualified medical expenses? MSA Qualified medical care described under Section 213 of the tax code. Health Reimbursement Health Savings Arrangements Accounts (HSA) (HRAs) Qualified medical Qualified medical expenses as defined expenses as in Section 213(d) of defined in Section the Internal Revenue 213(d) of the Code, e.g., amounts Internal Revenue paid for doctors’ Code, including fees, prescription health insurance medicines, and premiums. necessary medical services not paid for by insurance. HSA funds generally cannot be used to pay health insurance premiums; however, there are certain exceptions. See below (“When can funds be used to pay health insurance premiums?”). Health Care Flexible Spending Accounts (FSAs) Unreimbursed qualified medical expenses as defined in Section 213(d) of the Internal Revenue Code, except (in general) for health insurance premiums: e.g., amounts paid for doctors’ fees, prescription medicines, and necessary medical services not paid for by insurance. Health FSA funds generally cannot be used to pay health insurance premiums. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision What are the claim substantiation and adjudication requirements? MSA Claim substantiation is required. Health Reimbursement Health Care Health Savings Arrangements Flexible Spending Accounts (HSA) (HRAs) Accounts (FSAs) Claim substantiation Claim substantiation Claim substantiation by a third party is not is required. is required. required: however the individual HSA owner must maintain the records substantiating their claims. Plan is selfadjudicated by account owner submitting only eligible claims or reporting the taxable distribution. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision When can funds be used to pay health insurance premiums? Health Savings Accounts (HSA) Health Reimbursement Arrangements (HRAs) 1. While receiving unemployment benefits 1. While receiving unemployment benefits Funds can be used to pay for premium under: 2. While receiving COBRA benefits. 2. While receiving COBRA continuation benefits 1. The employee’s health plan MSA 2. A spouse’s health plan 3. The employer’s retiree health plan 4. COBRA continuation coverage. Health Care Flexible Spending Accounts (FSAs) Health care FSAs can not be used to pay insurance premiums of any kind. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision Can funds be used to pay for long-term care coverage? MSA Yes, premiums for qualified long-term care insurance are reimbursable up to the dollar limits specified in IRC 213(d). Health Savings Accounts (HSA) Yes, premiums for qualified long-term care insurance are reimbursable up to the dollar limits specified in IRC 213(d). Health Reimbursement Arrangements (HRAs) Yes, premiums for long-term care insurance are reimbursable. Health Care Flexible Spending Accounts (FSAs) No, the Internal Revenue Service code specifically excludes long term care insurance as a qualified benefit under a cafeteria plan; so long term care insurance premiums are not reimbursable under an FSA. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision Are withdrawals for non-medical expenses allowed? Health Savings MSA Accounts (HSA) Yes, but doing so will Yes, but distributions trigger a 15% tax not used exclusively penalty. to pay “qualified medical expenses” are included as income and are subject to a 10% additional tax. At the death of the individual the ownership of the account can be transferred to the spouse – otherwise the HSA ceases to be an HSA and is included in the gross income of the beneficiary or the individual’s estate. Health Reimbursement Arrangements (HRAs) No. Health Care Flexible Spending Accounts (FSAs) No. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision Can an employer or trustee limit reimbursements? What is the tax treatment of contributions? MSA No. Employee owns the account. Employee contributions are deductible in computing adjusted gross income and are deductible whether or not the individual itemizes deductions. Employer Contributions are excludable from gross income, are not subject to withholding for income tax, and are not subject to other employment taxes. Earnings: Earnings on amounts in an MSA are not taxable prior to distribution from the MSA. Health Savings Accounts (HSA) No. Employee contributions are tax deductible. Employer contributions are excludable from gross income and not subject to employment taxes (e.g., FICA). Health Reimbursement Arrangements (HRAs) Yes. The plan may define covered expenses. Employer contributions are generally excludable from employee’s gross income. Health Care Flexible Spending Accounts (FSAs) Yes. The plan may define covered expenses. Employees pay no federal, Social Security or (in most states) state taxes on FSA contributions. Employers pay no FICA tax on FSA contributions. Summary Comparison of HSAs – FSAs – HRAs - MSAs Health Reimbursement Arrangements (HRAs) Yes. Unused amounts in an HRA may be carried over, subject to any limits set by the employer). Provision Can funds be carried over from one year to the next? MSA Yes. Funds may be carried over indefinitely during a participant’s lifetime. Health Savings Accounts (HSA) Yes. Funds may be carried over indefinitely during a participant’s lifetime. Are accounts portable? Upon a participant’s death, an HSA may be passed on to a surviving spouse without federal tax liability. Yes. The account is owned by the employees. Employee continues to have access to the account when they leave or change jobs. Upon a participant’s death, an HSA may be passed on to a surviving spouse without federal tax liability. Yes. The account is Yes, but only at owned by the discretion of the employees. employer. Employee continues to have access to the account when they leave or change jobs. *New Ruling Health Care Flexible Spending Accounts (FSAs) *Yes for an additional 3 months following the end of the plan year. No. Unused FSA balances are forfeited to the employer if the employee leaves or changes jobs. Summary Comparison of HSAs – FSAs – HRAs - MSAs Provision Does interest accrue on funds deposited in the account? Do 105(h) nondiscrimination rules apply? MSA Yes. No. Health Savings Accounts (HSA) Yes. Interest accrues tax free. “Comparable” contributions required. Employer contributions must be the same for all employees who are “eligible individuals.” However, if employee contributions to an HSA are made through a Section 125 cafeteria plan, employer contributions are subject to the Section 125 nondiscrimination rules, not the comparability rules Health Reimbursement Arrangements (HRAs) There is no requirement that interest accrue but employers have discretion to credit interest to the HRA accounts. Yes, if self-funded. Health Care Flexible Spending Accounts (FSAs) No. Interest is not accrued. Yes. Long Term Care Insurance • Generally treated as accident and health insurance contracts – Amounts received are excluded from income – Per Diem Payments • Capped at $300 per day(2011). COBRA Health Insurance Continuation (Consolidated Omnibus Reconciliation Act of 1985) • Employers: 20 or more employees • Purpose: To allow qualified beneficiaries the opportunity to elect continued group health for specified periods of time under specified qualifying events • Qualifying Event – Death of the covered employee; – The covered employee’s termination of employment (for reasons other than gross misconduct) or reduction in hours worked; – Divorce or separation of the covered employee; – Entitlement of the covered employee to Medicare benefits (upon enrolling in the program); – A dependent child losing that status; and – Bankruptcy proceedings that cause a retired covered employee or the employee’s dependents to lose coverage. COBRA Health Insurance Continuation (Continued) • Duration of Continuation – Termination or reduction of work hours – 18 months – Absence due to military service – 24 months – Beneficiary is disabled – 29 months – Death, divorce, separation, loss of dependent child status or two or more qualifying events – 36 months • Premium Requirement: – 102% of health care premium rate. The 2% is allowance for additional administrative costs. – Up to 150% of premium cost for qualified disabled dependents from the 18th up to the 36th month of coverage • Coverage Election – The election period begins the day the previous coverage terminates – The election period lasts 60 days from that time (no longer) Family and Medical Leave Act • Employers: 50 or more employees • Guarantees employees: – 12 weeks of unpaid leave in a year. – Continuation of health benefits while on leave – employee is responsible for premiums during leave (may be required to pay entire premium, not just EE portion • Eligibility – Employed for at least 12 months (can be nonconsecutive) – Has worked at least 1250 hours within previous 12 months – Expatriates are not covered – employees must work within the United States or any of its territories and possessions. Sick Pay • Essential purpose is to replace the wages of an employee who cannot work because of an illness or injury. • Sick Pay under a Separate Plan – Short Term Disability – Long Term Disability – Third party sick pay taxation requirements • Permanent Disability Benefits • Difference between Sick Pay and Workers Compensation Cafeteria Plans • Provides a choice among taxable (cash) and nontaxable (qualified benefits) • Qualified benefits include: – Coverage under accident and health insurance plans • Medical, Dental, Vision, Etc. – Coverage under dependent care assistance plans – Group term Life insurance – Qualified adoption assistance • Funded by either Flex dollars or salary reductions • Nondiscrimination Testing – Eligibility Testing – Contributions and Benefits Test – Concentration Test – Special Health Benefits Test Tax treatment of Cafeteria Plans • Employer contributions – Excluded from employee’s income – Not subject to federal income tax withholding or employment taxes • Pre-tax contributions – Excluded from employee’s income • Post-tax contributions – Included in employee’s income, however, benefits received are not Questions ? RETIREMENT BENEFITS AND DEFERRED COMPENSATION PLANS Section 4 Retirement and Deferred Compensation Plans • • • • • • • • • • 401(a) - Qualified Pension & Profit Sharing Plans 401(k) - Cash or Deferred Arrangements 403(a) or 403(b) - Tax-Sheltered Annuities 457 - Deferred Compensation Plans – Public Sector and Tax-exempt groups 501(c)(18)(D) - Employee Funded Plans IRA - Individual Retirement Accounts 408(k) – SEP - Simplified Employee Pensions 408(p) – SIMPLE Plans - Savings Incentive Match Plans for Employees of Small Employers ESOP - Employee Stock Ownership Plans Nonqualified Deferred Compensation Plans Qualified Pension and Profit Sharing Plans (IRC 401(a)) •Defined Benefit Plan –5 Characteristics (4-85 2011) –Payroll Dept Responsibilities –Annual benefit limit = $195,000 •Defined Contribution Plan –Individual Accounts –Contribution by Employer –Contribution by Employee (but not always) –Annual Compensation Limit = $245,000 –Annual Contribution Limit = $49,000 •Or 100% of Employee compensation Amounts to remember Plan Type Annual Deferral Limit Annual Catch up Limit Annual Annual W-2 Compensation Contribution Box 12 Limit Limit Code 401(k) $16,500 $5,500 $245,000 $49,000 D 403(b) $16,500 $5,500 $245,000 $49,000 E 457 $16,500 $5,500 $245,000 501(c) $16,500 $5,500 $245,000 $1,000 Married $85,000 $5,000 Single $53,000 $16,500 $5,500 $245,000 $49,000 F 408(p) $10,500 $2,500 $245,000 $49,000 S IRA 408(k) ESOP G $49,000 $49,000 H 401(a) Pension Plans vs. Profit Sharing Plans • Pension Plans – Benefit determined when employee retires – Payable over employee’s life span – Employers contributions are not based on profit – Defined benefit plan or defined contribution plan • Profit Sharing Plans – Allows employees to participate in company profits – Discretionary contribution based on a selected formula by employer – Defined contribution plan only Cash or Deferred Arrangements (IRC 401(k)) •Pre-Tax contributions that decrease Employee’s taxable income Employer can make deferrals without employee consent up to 3% –Employee can then stop deferrals and receive cash or continue •Non Discrimination testing •Contributions to all plans are included in determining limit •Early distribution penalty equal to 10% excise tax •Employee contributions not subject to Federal Income Tax •Contribution amounts are subject to Social Security and Medicare Tax Tax Sheltered Annuities (IRC 403(B)) •Public Schools, Tax Exempt Charities, Religious, Educational Organizations •Requirements •Contribution limits EGTRRA •Employee contributions not subject to Federal Income Tax •Special provision for employees over 15 years of service •Additional information available – IRS Publication 571 Deferred Comp Plans for the Public Sector and Tax-Exempt Groups (IRC 457) •Eligibility •No discrimination testing •EGTRRA Limits •Contributions placed in tax exempt trust for employees and beneficiaries •Distributions cannot be made before employee reaches 70 1/2 years old, separation of employment (retirement) or employee has unforeseeable emergency. •Employee contributions not subject to Federal Income Tax Employee-Funded Plans (IRC 501(c)(18)(D)) •EGTRRA Limits •Employee contributions not subject to Federal Income Tax •Defined contribution plan •Solely funded by employee contributions •Maximum deferral limit is reduced by other CODAs maintained by the employer Individual Retirement Accounts •EGTRRA Limits •After tax amount deductible based on participation in other plans •Deductibility based on Adjusted Gross Income •Employer contributions included in income, but not subject to FIT •Defined Benefit or Defined Contribution Plan •Usually direct deposit contributions – not payroll deductions •Can be SIMPLE plan •ROTH IRA –Contributions not deductible –Not included in income if meet criteria –May contribute double amount of traditional IRA deductible amount Simplified Employee Pensions (IRC 408(k)) (SEP) •Employer’s who cannot provide traditional plans •Is an IRA •Employer must make contribution to plan on behalf of employee based on guidelines –21 years of age –Worked for employer 3 out of last 5 years –Earned at least $500 in 2008 •Salary reduction agreements limited to EGTRRA •Employees can elect a salary reduction agreement if plan was setup before 1997. Savings Incentive Match Plans for Employees of Small Employers (SIMPLE) IRC 408(p) •Small Business Job Protection Act of 1996 •Must allow eligible employees to participate –Employer with no qualified retirement plan and less than 100 employees –Received at least $5,000 in compensation during any 2 prior years –And expect to receive $5,000 in current year –EGTRRA Limits •Fully vested at time of contribution •Non-Discrimination testing •EE’s must have 60 days before year begins to make changes to contribution •Not subject to Federal Income Tax Stock Ownership Plans (ESOP) •Must meet 401(a) requirements –Participation –Vesting –Non discrimination •ESOP buys stock with employer contributions or borrowed / leveraged funds –Stock bonus plan –Combined stock bonus and money purchase plan –Designed to invest primarily in employer’s stock •Value changes based on stock •Not considered wages Nonqualified Deferred Compensation Plans • Compensation will be deferred until a later date • Funded vs. Unfunded – Funded • Subject to taxation – Unfunded • Not subject to taxation • Cannot be any other type of deferral plan • American Jobs Creation Act of 2004 W -2 Reporting Requirements • • • • • • • • • • • • MSA – Box 12 – Code R HSA – Box 12 – Code W Non-taxable Sick Pay – Box 12 – Code J Dependent Child Care – $5000 - Box 10 Adoption Assist - $10,630 – Box 12 – Code T 401(k) – Box 12 – Code D 403(a) or 403(b) – Box 12 – Code E 457 – Box 11 or Box 12 – Code G 501(c) – Box 12 – Code H 408(k) – Box 12 – Code F 408(p) – Box 12 – 401(k) = Code D, IRA = Code S 409(a) – Box 12 – Code Y or Z Questions ? Discussion Time Any questions on: Prior Topics Topic this week Homework Problems Next Class Topics: Section 5 Paying the Employee and Section 6 Withholding Taxes