Ch. 5 * Supply

Ch. 5 – Supply

Essential Question

How do the laws of supply interact to establish prices in the economy?

Review

Elastic= Adaptable- it changes/ have more choices= higher than 1.0

Example- Soda, Restaurants, etc

Inelastic= Not adaptable- it does not change/have less choices= under 1.0

Example- Insulin, gas, etc.

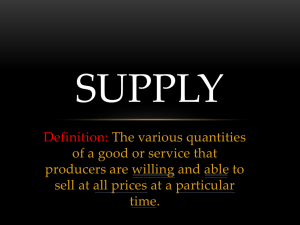

The Supply Curve

Supply= Suppliers=Producers= Sellers=Owner of a Company

Supply- a relation showing the quantities of a good producers are willing and able to sell at various prices during a given period, other things constant

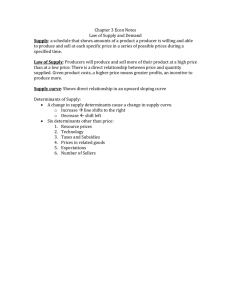

A. Law of Supply – As price increases, quantity supplied increases and vice-versa. There is a direct correlation (direct relationship)

B. Role of profit

1. profit = total revenue – total cost (every aspect)

2. entrepreneur takes risks because of profit incentive

The Supply Curve

Supply curve – a curve or line showing the quantities of a particular good supplied at various prices during a given period of time, other things constant

E. More willing and able to supply a good if price increases

F. Supply is the entire relationship between price and quantity supplied

G. Quantity supplied refers to a particular amount offered at a particular price

H. The market supply curve is simply the horizontal sum of the individual supply curves for all the suppliers in the market

Elasticity of Supply

Elasticity of supply – indicates how responsive producers are to a change in price. A measure of the responsiveness of quantity supplied to a price change/ or the % change in quantity supplied divided by the % change in price

1. This depends on how costly it is to alter output when the price changes a. If higher prices generates little increase in quantity supplied then quantity supplied tends to be inelastic b. Supply will be more elastic if a marginal price increase results in a large boost in output.

2. Elasticity of supply is typically greater in the longer the period of adjustment

Shifts of the Supply Curve

A. Five determinants of supply (other than the price of the good)reasons the curve may shift

1. Cost of resources used to make the good

*Costs of Production/Input prices

2. Price of other goods these resources could make

*Taxes (discourage production)

*Subsidies/Tax breaks- encourage production

3. The technology used to make the good

*If technology increases= supply curve shifts outward/right

4. Producer expectations of future prices

5. Number of sellers in the market

Shifts in the Supply Curve

B. Movement along a supply curve is caused by a change in price

Change in quantity supplied resulting from a change in price of the good

C. A change in one of the determinants of supply causes a shift

Increase or decrease in supply resulting from a change in 1 of the determinants of supply

Production and Costs

A. Production in the short run (Period during which at least 1 of a firm’s resources is fixed)

1. At least one resource is a fixed cost (cannot be easily altered) ex: size of the warehouse, mortgage, rent- stays the same every month

2. Labor is an example of a variable resource/cost- can change

3. Law of diminishing returns – is the most important feature of production in the short run – marginal product eventually declines as more units of one resource are added to all other resources (As you get more of it, you want it less)

Costs in the Short run

1. fixed cost – any production cost that is independent of the firm’s output

*Sometimes called overhead – must pay for building, taxes, insurance, etc.

2. variable cost – any production cost that changes as output changes

*Labor is a variable cost.

* Add fixed cost and variable cost = total cost

3. total cost- the sum of fixed cost and variable cost

4. marginal cost = change in total cost divided by change in quantity

*What it costs for each unit?

5. Short run losses and shutting down

Production and Costs in the Short Run

Short run: Period during which ALL resources can be varied/changed.

1. Economies of scale – Buying in bulk/large quantities

The larger the company, the cheaper the cost

Ex: Costco, BJ’s, Sam’s Club

2. Diseconomies of scale –Spending more $ than you are making

Ex: Gov’t

Essential Question

How do the laws of supply interact to establish prices in the economy?