BREMEN UNIVERSITY

SUMMER SCHOOL

Entrepreneurship and

Business Planning

Course Handout

Assist. Prof. Dr. Saban Celik

Department of International Trade and Finance

Yaşar University, IZMIR, TURKEY

Email:saban.celik@yasar.edu.tr

Web: http://scelik.yasar.edu.tr

3/16/2014

This course handout is prepared for the course entitled “Entrepreneurship and Business Planning” given

in Bremen University Summer School. All Rights Reserved. No part of this handout or any of its contents

may be reproduced, copied, modified or adapted, without the prior written consent of the Bremen

University, unless otherwise indicated for stand-alone materials.

[Intentionally left blank]

2

BREMEN UNIVERSITY

THE INTERNATIONAL SUMMER SCHOOL

COURSE HANDOUT

BREMEN –2015

SHORT CONTENT

SESSION I

The Foundations of Entrepreneurship

Entrepreneurial Mind

SESSION II

Strategic Management and the Entrepreneur

Forms of Business Ownership and Franchising

SESSION III

Creating a Powerful Business Plan

SESSION IV

E-Commerce and the Entrepreneur

SESSION V

Integrated Marketing Communications and Pricing Strategies

SESSION VI

Creating a Successful Financial Plan

SESSION VII

Managing Cash Flow

SESSION VIII

Staffing and Leading a Growing Company

SESSION IX

Sources of Funds: Equity and Debt

SESSION X

Case Studies: Global Aspects of Entrepreneurship

3

COURSE DESCRIPTION

This course addresses the unique entrepreneurial experience of conceiving, evaluating, creating,

managing, and potentially selling a business. The goal is to provide a comprehensive background

with practical application of important concepts applicable to entrepreneurial environment. In

addition to creative aspects, key business areas of finance, accounting, marketing and

management will be addressed from an entrepreneurial perspective. The course relies on

classroom discussion, participation, case analysis, the creation of a feasibility plan, and building

a business plan to develop a strategy for launching and managing a business. Students will need

to draw upon their business education and experience, and apply it to the task of launching a new

venture. Students are expected to interact with advisors, be able to work effectively in teams, and

be active participants in classroom discussions and exercises.

COURSE OBJECTIVES

To possess a well grounded understanding of essential entrepreneurial business principals.

To develop an understanding of important business issues as they relate to new ventures.

To identify, appreciate, and assess the knowledge, attitudes, and skills of an entrepreneur.

To study and observe entrepreneurial settings and entrepreneurial role models through

exposure to actual business settings and experiences.

To have an expanded awareness of the resources available for creating a business plan.

To establish a level of confidence in creating a business plan as a tool to assess, create and

communicate a business concept.

RESOURCES

Main Textbook

Entrepreneurship and Effective Small Business Management, 11th

Edition, Scarborough, Norman M. Upper Saddle River, NJ: Pearson Prentice Hall

Publishing Co., 2015.

Supplementary Textbook

Exploring Business;Karen Collins,Prentice Hall, Upper Saddle River, 2008

New Venture Creation: Entrepreneurship For The 21st Century, 9/E; Stephen Spinelli And Robert J.

Adams, Jr. The Mcgraw-Hill Companies, Inc., 2012

Enterprise in the Global Firm, Julian Birkinshaw, SAGE Publications, SAGE Publications Ltd 6 Bonhill

Street London EC2A 4PU.

Entrepreneurship The Seeds of Success, John Forbat, HARRIMAN HOUSE LTD 3A Penns Road

Petersfield Hampshire GU32 3EW,

Perspectives on Innovation, Editors Franco Malerba and Stefano Brusoni,

Cambridge University Press, The Edinburgh Building, Cambridge CB2 8RU, UK,

The Entrepreneurial Personality A Social Construction, Second edition, Elizabeth Chell, First published

2008 by Routledge 27 Church Road, Hove, East Sussex BN3 2FA.

Doing Business Report, 2013, 2013 The International Bank for Reconstruction and Development / The

World Bank

4

SESSION I

The Foundations of Entrepreneurship

Entrepreneurial Mind

Chapter Review

1. Define the role of the entrepreneur in business

Record numbers of people have launched companies over the past decade. The boom

in entrepreneurship is not limited solely to developed countries; many nations across

the globe are seeing similar growth in the small business sector. A variety of

competitive, economic, and demographic shifts have created a world in which "small

is beautiful."

Society depends on entrepreneurs to provide the drive and risk-taking necessary for

the business system to supply people with the goods and services they need.

2. Describe the entrepreneurial profile.

Entrepreneurs have some common characteristics, including a desire for

responsibility, a preference for moderate risk, confidence in their ability to succeed,

desire for immediate feedback, a high energy level, a future orientation, skill at

organizing, and a value of achievement over money. In a phrase, they are high

achievers.

3. Describe the benefits of owning a small business.

Driven by these personal characteristics, entrepreneurs establish and manage small

businesses to gain control over their lives, become self-fulfilled, reap unlimited

profits, contribute to society, and do what they enjoy doing.

4. Describe the potential drawbacks of owning a small business.

Small business ownership has some potential drawbacks. There are no guarantees

that the business will make a profit or even survive. The time and energy required to

manage a new business may have dire effects on the owner and family members.

5. Explain the forces that are driving the growth in entrepreneurship.

Several factors are driving the boom in entrepreneurship, including entrepreneurs

portrayed as heroes, better entrepreneurial education, economic and demographic

factors, a shift to a service economy, technological advancements, more independent

lifestyles, and increased international opportunities.

6. Discuss the role of diversity in small business and entrepreneurship.

Several groups are leading the nation's drive toward entrepreneurship--women,

minorities, immigrants, "part-timers," home-based business owners, family business

owners, copreneurs, corporate castoffs, and corporate dropouts.

7. Explain the reasons small businesses fail.

The failure rate for small businesses is higher than for big businesses, and profits

fluctuate with general economic conditions. SBA statistics show that 60 percent of

new businesses will have failed within six years. The primary cause of business

failure is incompetent management. Other reasons include poor financial control,

failure to plan, inappropriate location, lack of inventory control, improper managerial

attitudes, and inability to make the "entrepreneurial transition."

5

9. Put business failure into the proper perspective.

Because they are building businesses in an environment filled with uncertainty and

shaped by rapid change, entrepreneurs recognize that failure is likely to be a part of

their lives; yet, they are not paralyzed by that fear. Successful entrepreneurs have the

attitude that failures are simply stepping stones along the path to success.

10. Explain how small business owners can avoid the major pitfalls of running a business.

There are several general tactics the small business owner can employ to avoid

failure. The entrepreneur should know the business in depth, develop a solid business

plan, manage financial resources effectively, understand financial statements, learn to

manage people effectively, set the business apart from the competition, and keep in

tune with yourself.

Discussion Questions

S1Q1: What is an entrepreneur? Give a brief description of the entrepreneurial profile.

S1Q2: Inc. magazine claims, "Entrepreneurship is more mundane than it's sometimes portrayed ... you don't need to

be a person of mythical proportions to be very, very successful in building

a company." Do you agree?

Explain.

S1Q3: What are the major benefits of business ownership?

S1Q4: Which of the potential drawbacks to business ownership are most critical?

S1Q5: Describe the small business failure.

6

SESSION II

Strategic Management and the Entrepreneur

Forms of Business Ownership and Franchising

Chapter Summary

1. Understand the importance of strategic management to a small business.

Strategic planning, often ignored by small companies, is a crucial ingredient in

business success. The planning process forces potential entrepreneurs to subject their

ideas to an objective evaluation in the competitive market.

2. Explain why and how a small business must create a competitive advantage in the market.

The goal of developing a strategic plan is to create for the small company a

competitive advantage--the aggregation of factors that sets the small business apart

from its competitors and gives it a unique position in the market. Every small firm

must establish a plan for creating a unique image in the minds of its potential

customers.

3. Develop a strategic plan for a business using the nine steps in the strategic planning process.

Small businesses need a strategic planning process designed to suit their particular

needs. It should be relatively short, be informal and not structured, encourage the

participation of employees, and not begin with extensive objective setting. Linking

the purposeful action of strategic planning to an entrepreneur's little ideas can

produce results that shape the future.

Step 1. Develop a clear vision and translate it into a meaningful mission statement.

Highly successful entrepreneurs are able to communicate their vision to those around

them. The firm's mission statement answers the first question of any venture: What

business am I in? The mission statement sets the tone for the entire company.

Step 2: Assess the company's strengths and weaknesses. Strengths are positive

internal factors; weaknesses are negative internal factors.

Step 3: Scan the environment for significant opportunities and threats facing the

business. Opportunities are positive external options; threats are negative external

forces.

Step 4: Identify the key factors for success in the business. In every business, key

factors that determine the success of the firms in it, and so they must be an integral

part of a company' strategy. Key success factors are relationships between a

controllable variable (e.g., plant size, size of sales force, advertising expenditures,

product packaging) and a critical factor influencing the firm's ability to compete in

the market.

Step 5: Analyze the competition. Business owners should know their competitors

almost as well as they know their own. A competitive profile matrix is a helpful tool

for analyzing competitors’ strengths and weaknesses.

Step 6: Create company goals and objectives. Goals are the broad, long-range

attributes that

the firm seeks to accomplish. Objectives are quantifiable and more

precise; they should be specific, measurable, assignable, realistic, timely, and written

down. The process works best when subordinate managers and employees are

actively involved.

Step 7: Formulate strategic options and select the appropriate strategies. A strategy is

the game plan the firm plans to use to achieve its objectives and mission. It must

center on establishing for the firm the key success factors identified earlier.

7

Step 8: Translate strategic plans into action plans. No strategic plan is complete until

the owner puts it into action.

Step 9: Establish accurate controls. Actual performance rarely, if ever, matches plans

exactly. Operating data from the business serve as guideposts for detecting deviations

from plans. Such information is helpful when plotting future strategies.

The strategic planning process does not end with these ten steps; rather, it is an ongoing

process that the owner will repeat

4. Discuss the characteristics of three basic strategies: low-cost, differentiation, and focus.

Three basic strategic options are cost leadership, differentiation, and focus. A

company pursuing a cost leadership strategy strives to be the lowest-cost producer

relative to its competitors in the industry.

A company following a differentiation strategy seeks to build customer loyalty by

positioning its goods or services in a unique or different fashion. In other words, the

firm strives to be better than its competitors at something that customers value.

A focus strategy recognizes that not all markets are homogeneous. The principal idea

of this strategy is to select one (or more) segment(s), identify customers special

needs, wants, and interests, and approach them with a good or service designed to

excel in meeting these needs, wants, and interests. Focus strategies build on

differences among market segments.

5. Understand the importance of controls such as the balanced scorecard in the planning

process.

Just as a pilot in command of a jet cannot fly safely by focusing on a single

instrument, an

entrepreneur cannot manage a company by concentrating on a

single measurement. The balanced scorecard is a set of measurements unique to a

company that includes both financial and operational measures and gives managers a

quick yet comprehensive picture of the company's total performance.

6. Discuss the issue entrepreneurs should consider when evaluating different forms of ownership:

The key to choosing the “right” form of ownership is understanding the characteristics of

each form and knowing how they affect an entrepreneur’s personal and business

circumstances.

Factors to consider include: tax implications, liability expense, start-up and future capital

requirements, control, managerial ability, business goals, management succession plane,

and cost of formation.

7. Describe the advantages and disadvantages of the sole proprietorship.

A sole proprietorship is a business owned and managed by one individual and is the most

popular form of ownership.

Sole proprietorships offer these advantages:

Simple to create

Least costly form to begin

Owner has total decision making authority

No special legal restrictions

Easy to discontinue

Sole proprietorships suffer from these disadvantages:

Unlimited personal liability of owner

Limited managerial skills and capabilities

8

Limited access to capital

Lack of continuity

8. Describe the advantages and disadvantages of the partnership.

A partnership is an association of two or more people who co-own a business for the

purpose of making a profit.

Partnerships offer these advantages

Easy to establish

Complimentary skills of partners

Division of profits

Larger pool of capital available

Ability to attract limited partners

Little government regulation

Flexibility

Tax advantages

Partnerships suffer from these disadvantages.

Unlimited liability of at least one partner

Difficulty in disposing of partnership interest

Lack of continuity

Potential for personality and authority conflicts

Partners are bound by the law of agency

9. A limited partnership operates like any other partnership except that it allows limited partners

(primary investors that cannot take an active role in managing the business) to become owners

without subjecting themselves to unlimited personal liability for the company’s debts.

10. Describe the advantages and disadvantages of the corporation.

A corporation, the most complex of the three basic forms of ownership, is a separate

legal entity. To form a corporation, an entrepreneur must file the articles of

incorporation with the state in which the company will incorporate.

Corporations offer these advantages.

Limited liability of stockholders

Ability to attract capital

Ability to continue indefinitely

Transferable ownership

Corporations suffer from these disadvantages.

Cost and time in incorporating

Double taxation

Potential for diminished managerial incentives

Legal requirements and regulatory red tape

Potential loss of control by the founders

11. Describe the advantages and disadvantages of the alternative forms of ownership such as the

S corporation, the limited liability company, and the joint venture.

An S corporation offers its owners limited liability protection, but avoids the double

taxation of C corporations.

A limited liability company, like an S corporation, is a cross between a partnership and a

corporation. However, it operates without the restrictions imposed on an S corporation.

9

To create a LLC, an entrepreneur must file the articles of organization and the operating

agreement with the secretary of state.

A joint venture is like a partnership, except that it is formed for a specific purpose.

12. Define the concept of franchising and describe the different types of franchises.

Franchising is a method of doing business involving a continuous relationship between a

franchiser and a franchisee. The franchiser retains control of the distribution system,

while the franchisee assumes all of the normal daily operating functions of the business.

There are three types of franchising: trade name franchising, where the franchisee

purchases only the right to use a brand name; product distribution franchising, which

involves a license to sell specific products under a brand name; and pure franchising,

which provides a franchisee with a complete business system.

13. Describe the benefits and limitations of buying a franchise.

The franchiser has the benefits of expanding his business on limited capital and growing

without developing key managers internally. The franchisee also receives many key

benefits: management training and counseling, customer appeal of a brand name;

standardized quality of goods and services, national advertising programs, financial

assistance, proven products and business formats, centralized buying power, territorial

protection, and greater chances for success.

Potential franchisees should be aware of the disadvantages involved in buying a

franchise: franchise fees and profit sharing, strict adherence to standardized operations,

restrictions on purchasing, limited product lines, possible ineffective training programs,

and less freedom.

Discussion Questions

S2Q1: Why is strategic planning important to a small company?

S2Q2: What is a competitive advantage? Why is it important for a small business to establish one?

S2Q3: What are strengths, weaknesses, opportunities, and threats? Give an example of each.

S2Q4: Explain the characteristics of effective objectives. Why is setting objectives important?

S2Q5: What are business strategies?

S2Q6: Describe the three basic strategies available to small companies. Under what conditions is each most

successful?

S2Q7: What is a balanced scorecard? What value does it offer entrepreneurs who are evaluating the success of their

current strategies?

S2Q8: What factors should an entrepreneur consider before choosing a form of ownership?

S2Q9: Why are sole proprietorships so popular as a form of ownership?

S2Q10: Explain the differences between a domestic corporation, a foreign corporation, and an alien corporation.

S2Q11: Explain the differences between a domestic corporation, a foreign corporation, and an alien corporation.

S2Q12: Describe the three types of franchising and give an example of each.

10

SESSION III

Creating a Powerful Business Plan

Chapter Review

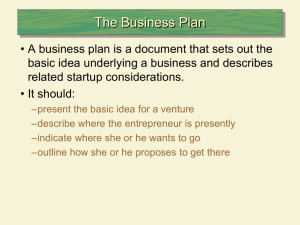

1. Explain why every entrepreneur should create a business plan.

A business plan serves two essential functions. First and more important, it guides the

company’s operations by charting its future course and devising a strategy for following

it. The second function of the business plan is to attract lenders and investors.

Applying for loans or attempting to attract investors without a solid business plan rarely

attracts needed capital. Rather, the best way to secure the necessary capital is to prepare a

sound business plan.

2. Describe the elements of a solid business plan.

Although a business plan should be unique and tailor-made to suit the particular needs of

a small company, it should cover these basic elements: an executive summary, a mission

statement, a company history, a business and industry profile, a description of the

company’s business strategy, a profile of its products or services, a statement explaining

its marketing strategy, a competitor analysis, owners’ and officers’ résumés, a plan of

operation, financial data, and the loan or investment proposal.

3. Explain the three tests every business plan should pass.

Reality test. The external component of the reality test revolves around proving that a

market for the product or service really does exist. The internal component of the reality

test focuses on the product or service itself.

Competitive test. The external part of the competitive test evaluates the company’s

relative position to its key competitors. The internal competitive test focuses on the

management team’s ability to create a company that will gain an edge over existing

rivals.

Value test. To convince lenders and investors to put their money into the venture, a

business plan must prove to them that it offers a high probability of repayment or an

attractive rate of return.

4. Understand the keys to making an effective business plan presentation.

Lenders and investors are favorably impressed by entrepreneurs who are informed and

prepared when requesting a loan or investment.

Tips include demonstrating enthusiasm about the venture but not overemotional;

“hooking” investors quickly with an up-front explanation of the new venture, its

opportunities, and the anticipated benefits to them; using visual aids; hitting the

highlights of your venture; not getting caught up in too much detail in early meetings

with lenders and investors; avoiding the use of technological terms that will likely be

above most of the audience; rehearsing the presentation before giving it; closing by

reinforcing the nature of the opportunity; and being prepared for questions.

5. Explain the “five Cs of credit” and why they are important to potential lenders and investors

reading business plans.

Small business owners need to be aware of the criteria bankers use in evaluating the

creditworthiness of loan applicants—the five Cs of credit: capital, capacity, collateral,

character, and conditions.

11

Capital. Lenders expect small businesses to have an equity base of investment by the

owner(s) that will help support the venture during times of financial strain.

Capacity. A synonym for capacity is cash flow. The bank must be convinced of the

firm’s ability to meet its regular financial obligations and to repay the bank loan, and that

takes cash.

Collateral. Collateral includes any assets the owner pledges to the bank as security for

repayment of the loan.

Character. Before approving a loan to a small business, the banker must be satisfied with

the owner’s character.

Conditions. Conditions such as interest rates, the health of the nation’s economy, and

industry growth rates surrounding a loan request also affect the owner’s chance of

receiving funds.

Discussion Questions

S3Q1: Why should an entrepreneur develop a business plan?

S3Q2: Why do entrepreneurs who are not seeking external financing need to prepare business plans?

S3Q3: Describe the major components of a business plan.

S3Q4: How can an entrepreneur seeking funds to launch a business convince potential lenders and investors that a

market for the product or service really does exist?

S3Q5: How would you prepare to make a formal presentation of your business plan to a venture capital forum?

S3Q6: What are the 5 C’s of credit? How do lenders and investors use them when evaluating a request for

financing?

12

SESSION IV

E-Commerce and the Entrepreneur

Chapter Summary

1. Describe the benefits of selling on the World Wide Web.

Although a Web-based sales strategy does not guarantee success, the companies that have

pioneered Web-based selling have realized many benefits, including the following:

The opportunity to increase revenues.

The ability to expand their reach into global markets.

The ability to remain open 24 hours a day, seven days a week

The capacity to use the Web’s interactive nature to enhance customer service.

The power to educate and to inform

The ability to lower the cost of doing business.

The ability to spot new business opportunities and to capitalize on them.

The power to track sales results.

2. Understand the factors an entrepreneur should consider before launching into e-commerce.

Before launching an e-commerce effort, business owners should consider the following

important issues:

How a company exploits the Web’s interconnectivity and the opportunities it creates to

transform relationships with its suppliers and vendors, its customers, and other external

stakeholders is crucial to its success.

Web success requires a company to develop a plan for integrating the Web into its overall

strategy. The plan should address issues such as site design and maintenance, creating

and managing a brand name, marketing and promotional strategies, sales, and customer

service.

Developing deep, lasting relationships with customers takes on even greater importance

on the Web. Attracting customers on the Web costs money, and companies must be able

to retain their online customers to make their Web sites profitable.

Creating a meaningful presence on the Web requires an ongoing investment of

resources—time, money, energy, and talent. Establishing an attractive Web site

brimming with catchy photographs of products is only the beginning.

Measuring the success of its Web-based sales effort is essential to remaining relevant to

customers whose tastes, needs, and preferences are always changing.

3. Explain the twelve myths of e-commerce and how to avoid falling victim to them.

The twelve myths of e-commerce are:

Myth 1. Setting up a business on the Web is easy and inexpensive.

Myth 2. If I launch a site, customers will flock to it.

Myth 3. Making money on the Web is easy.

Myth 4. Privacy is not an important issue on the Web.

Myth 5. The most important part of any e-commerce effort is technology.

Myth 6. “Strategy? I don’t need a strategy to sell on the Web! Just give me a Web site,

and the rest will take care of itself.”

Myth 7. On the Web, customer service is not as important as it is in a traditional retail

store.

Myth 8. Flash makes a Web site better.

Myth 9. It’s what’s up front that counts.

Myth 10. E-commerce will cause brick-and-mortar retail stores to disappear.

13

Myth 11. The greatest opportunities for e-commerce lie in the retail sector.

Myth 12. It’s too late to get on the Web.

4. Explain the basic strategies entrepreneurs should follow to achieve success in their ecommerce efforts.

Following are some guidelines for building a successful Web strategy for a small e-company:

Consider focusing on a niche in the market.

Develop a community of on-line customers.

Attract visitors by giving away “freebies.”

Make creative use of e-mail, but avoid becoming a “spammer.”

Make sure your Web site says “credibility.”

Consider forming strategic alliances with larger, more established companies.

Make the most of the Web’s global reach.

Promote your Web site on-line and off-line.

5. Learn the techniques of designing a killer Web site.

There is no sure-fire formula for stopping surfers in their tracks, but the following suggestions

will help:

Select a domain name that is consistent with the image you want to create for your

company and register it.

Be easy to find.

Give customers want they want.

Establish hyperlinks with other businesses, preferably those selling products or services

that complement yours.

Include an e-mail option and a telephone number in your site.

Give shoppers the ability to track their orders on-line.

Offer Web shoppers a special all their own.

Follow a simple design for your Web page.

Assure customers that their on-line transactions are secure.

Keep your site updated.

Consider hiring a professional to design your site.

6. Explain how companies track the results from their Web sites.

The simplest technique for tracking the results of a Web site is a counter, which records the

number of “hits” a Web site receives. Another option for tracking Web activity is through loganalysis software. Server logs record every page, graphic, audio clip, or photograph that visitors

to a site access, and log-analysis software analyzes these logs and generates reports describing

how visitors behave when they get to a site.

7. Describe how e-businesses ensure the privacy and security of the information they collect

and store from the Web.

To make sure they are using the information they collect from visitors to their Web sites legally

and ethically, companies should take the following steps:

Take an inventory of the customer data collected.

Develop a company privacy policy for the information you collect.

Post your company’s privacy policy prominently on your Web site and follow it.

To ensure the security of the information they collect and store from Web transactions,

companies should rely on virus and intrusion detection software and firewalls to ward off attacks

from hackers.

14

Discussion Questions

S4Q1: In what ways have the Internet and e-commerce changed the ways companies do business?

S4Q2: Explain the benefits a company earns by selling on the Web.

S4Q3: Discuss the factors entrepreneurs should consider before launching an e-commerce site.

S4Q4: What are the 12 myths of e-commerce? What can an entrepreneur do to avoid them?

S4Q5: What strategic advice would you offer an entrepreneur about to start an e-company?

S4Q6: What design characteristics make for a successful Web page?

15

SESSION V

Integrated Marketing Communications and Pricing Strategies

Chapter Review

1. Explain the value of integrated marketing communications.

All marketing communications messages from any medium are clear, consistent, and

compelling.

Each communication conveys the same positive message.

Branding of the firm’s products or services is supported by communicating the correct

unique selling proposition (USP).

2. Describe the basis of an integrated marketing communications plan.

Focus on your target audience.

Know exactly what you want your message to achieve.

3. Describe the elements of a marketing communications plan

Advertising

Publicity and public relations

Personal selling

4. Describe the advantages and disadvantages of the various advertising media.

The medium used to transmit an advertising message influences the consumer’s

perception—and reception—of it.

Media options include newspapers, radio, television, magazines, direct mail, the World

Wide Web, outdoor advertising, transit advertising, directories, trade shows, special

events and promotions, and point-of-purchase ads.

5. Discuss the four basic methods for preparing a marketing communications budget.

Four basic methods are what is affordable; matching competitors; percentage of sales;

objective and task.

6. Explain practical methods for stretching a small business’s advertising budget.

Despite their limited advertising budgets, small businesses do not have to take a secondclass approach to advertising. Three techniques that can stretch a small company’s

advertising dollars are cooperative advertising, shared advertising, and publicity.

Discussion Questions

S5Q1: What are the three elements of promotion? How do they support one another?

S5Q2: What factors should a small business manager consider when selecting advertising media?

S5Q3: What is a unique selling proposition? What role should it play in a company's advertising strategy?

S5Q4: Briefly outline the steps in creating an advertising plan. What principles should the small business owner

fol¬low when creating an effective advertisement?

S5Q5: Describe the common methods of establishing an ad¬vertising budget. Which method is most often used?

Which technique is most often recommended? Why?

S5Q6: What techniques can small businesses use to stretch their advertising budgets?

16

SESSION VI

Creating a Successful Financial Plan

Chapter Summary

1. Understand the importance of preparing a financial plan.

Launching a successful business requires an entrepreneur to create a solid financial plan. Not

only is such a plan an important tool in raising the capital needed to get a company off the

ground, but it also is an essential ingredient in managing a growing business.

Earning a profit does not occur by accident; it takes planning.

2. Describe how to prepare the basic financial statements and use them to manage the small

business.

Entrepreneurs rely on three basic financial statements to understand the financial

conditions of their companies:

o The balance sheet. Built on the accounting equation: Assets = Liabilities + Owner's

Equity (Capital), it provides an estimate of the company's value on a particular date.

o The income statement. This statement compares the firm's revenues against its

expenses to determine its net income (or loss). It provides information about the

company's bottom line.

o The statement of cash flows. This statement shows the change in the company's

working capital over the accounting period by listing the sources and the uses of

funds.

3. Create projected financial statements.

Projected (pro forma) financial statements are a basic component of a sound financial plan.

They help the manager plot the company's financial future by setting operating objectives

and by analyzing the reasons for variations from targeted results. Also, the small business in

search of start-up funds will need these pro forma statements to present to prospective

lenders and investors. They also assist in determining the amount of cash, inventory, fixtures,

and other assets the business will need to begin operation.

4. Understand the basic financial statements through ratio analysis.

The 12 key ratios described in this chapter are divided into four major categories:

o liquidity ratios, which show the small firm's ability to meet its current obligations,

o leverage ratios, which tell how much of the company's financing is provided by

owners and how much by creditors

o operating ratios, which show how effectively the firm uses its resources

o profitability ratios, which disclose the company's profitability

Many agencies and organizations regularly publish such statistics. If there is a discrepancy

between the small firm's ratios and those of the typical business, the owner should investigate

the reason for the difference. A below-average ratio does not necessarily mean that the

business is in trouble.

5. Explain how to interpret financial ratios.

To benefit from ratio analysis, the small company should compare its ratios with those of

other companies in the same line of business and look for trends over time.

When business owners detect deviations in their companies' ratios from industry standards,

they should determine the cause of the deviations. In some cases, such deviations are the

result of sound business decisions; in other instances, however, ratios that are out of the

17

normal range for a particular type of business are indicators of what could become serious

problems for a company.

6. Conduct a break-even analysis for a small company.

Business owners should know their firm's break-even point, the level of operations at which

total revenues equal total costs; it is the point at which companies neither earn a profit nor

incur a loss. Although just a simple screening device, break-even analysis is a useful

planning and decision-making tool.

Discussion Questions

S6Q1: Why is it important for entrepreneurs to develop financial plans for their companies?

S6Q2: How should a small business manager use the ratios discussed in this chapter?

S6Q3: Outline the key points of the 12 ratios discussed in this chapter. What signals does each give a business

owner?

S6Q4: Describe the method for building a projected income statement and a projected balance sheet for a beginning

business.

S6Q5: How can break-even analysis help an entrepreneur planning to launch a business? What information does it

give an entrepreneur?

18

SESSION VII

Managing Cash Flow

Chapter Summary

1. Explain the importance of cash management to the success of the small business.

Cash is the most important but least productive asset the small business has. The manager

must maintain enough cash to meet the firm's normal requirements (plus a reserve for

emergencies) without retaining excessively large, unproductive cash balances.

Without adequate cash, a small business will fail.

2. Differentiate between cash and profits.

Cash and profits are not the same. More businesses fail for lack of cash than for lack of

profits.

Profits, the difference between total revenue and total expenses, are an accounting concept.

Cash flow represents the flow of actual cash (the only thing businesses can use to pay bills)

through a business in a continuous cycle. A business can be earning a profit and be forced out

of business because it runs out of cash.

3. Understand the five steps in creating a cash budget and use them to create a cash budget.

The cash budgeting procedure tracks the flow of cash through the business and enables the

owner to project cash surpluses and cash deficits at specific intervals.

The five steps in creating a cash budget are determining an adequate minimum cash balance,

forecasting sales, and forecasting cash receipts, forecasting cash disbursements, and

determining the end-of-month cash balance.

4. Describe fundamental principles involved in managing the "Big Three" of cash management:

accounts receivable, accounts payable, and inventory.

Controlling accounts receivable requires business owners to establish clear, firm credit and

collection policies and to screen customers before granting them credit. Sending invoices

promptly and acting on past-due accounts quickly also improve cash flow. The goal is to

collect cash from receivables as quickly as possible.

When managing accounts payable, a manager's goal is to stretch out payables as long as

possible without damaging the company's credit rating. Other techniques include verifying

invoices before paying them, taking advantage of cash discounts, and negotiating the best

possible credit terms.

Inventory frequently causes cash headaches for small business managers. Excess inventory

earns a zero rate of return and ties up a company's cash unnecessarily. Owners must watch

for stale merchandise.

5. Explain the techniques for avoiding a cash crunch in a small company.

Trimming overhead costs by bartering, leasing assets, avoiding nonessential outlays, using

zero-based budgeting, and implementing an internal control system boost a firm's cash flow

position.

Investing surplus cash maximizes the firm's earning power. The primary criteria for investing

surplus cash are security and liquidity.

19

Discussion Questions

S7Q1:Why must small business owners concentrate on effective cash flow management?

S7Q2:Explain the difference between cash and profit.

S7Q3:Outline the steps involved in developing a cash budget.

S7Q4:How can an entrepreneur launching a new business forecast sales?

S7Q5:Outline the basic principles of managing a small firm's receivables, payables, and inventory.

S7Q6:What steps should business owners take to conserve cash in their companies?

S7Q7:What should be a small business owner's primary concerns when investing surplus cash?

20

SESSION VIII

Staffing and Leading a Growing Company

Chapter Review

1. Explain the challenges involved in the entrepreneur's role as leader and what it takes to be a

successful leader.

Leadership is the process of influencing and inspiring others to work to achieve a

common goal and then giving them the power and the freedom to achieve it.

Management and leadership are not the same; yet both are essential to a small company's

success. Leadership without management is unbridled; management without leadership is

uninspired. Leadership gets a small business going; management keeps it going.

2. Describe the importance of hiring the right employees and how to avoid making hiring

mistakes.

The decision to hire a new employee is an important one for every business, but its impact

is magnified many times in a small company. Every “new hire” a business owner makes

determines the heights to which the company can climb or the depths to which it will

plunge.

To avoid making hiring mistakes, entrepreneurs should: develop meaningful job

descriptions and job specifications; plan and conduct an effective interview; and check

references before hiring any employee.

3. Explain how to build the kind of company culture and structure to support the entrepreneur’s

mission and goals and to motivate employees to achieve them.

Company culture is the distinctive, unwritten code of conduct that governs the behavior,

attitudes, relationships, and style of an organization. Culture arises from an

entrepreneur’s consistent and relentless pursuit of a set of core values that everyone in the

company can believe in. Small companies’ flexible structures can be a major competitive

weapon.

Entrepreneurs rely on six different management styles to guide their companies as they

grow. The first three (craftsman, classic, and coordinator) involve running a company

without any management assistance and are best suited for small companies in the early

stages of growth; the last three (entrepreneur-plus-employee team, small partnership, bigteam venture) rely on a team approach to run the company as its growth speeds up.

4. Understand the potential barriers to effective communication and describe how to overcome

them.

Research shows that managers spend about 80 percent of their time in some form of

communication; yet their attempts at communicating sometimes go wrong. Several

barriers to effective communication include: Managers and employees don't always feel

free to say what they really mean; ambiguity blocks real communication; information

overload causes the message to get lost; selective listening interferes with the

communication process; defense mechanisms block a message; and conflicting verbal

and nonverbal messages confuse listeners.

To become more effective communicators, business owners should: Clarify their

messages before attempting to communicate them; use face-to-face communication

whenever possible; be empathetic; match their messages to their audiences; be organized;

encourage feedback; tell the truth; not be afraid to tell employees about the business, its

performance, and the forces that affect it.

21

5. Discuss the ways in which entrepreneurs can motivate their workers to higher levels of

performance.

Motivation is the degree of effort an employee exerts to accomplish a task; it shows up as

excitement about work. Four important tools of motivation are empowerment, job design,

rewards and compensation, and feedback.

Empowerment involves giving workers at every level of the organization the power, the

freedom, and the responsibility to control their own work, to make decisions, and to take

action to meet the company’s objectives.

Job design techniques for enhancing employee motivation include job enlargement, job

rotation, job enrichment, flextime, job sharing, and flex-place (which includes

telecommuting and hoteling).

Money is an important motivator for many workers, but not the only one. The key to

using rewards such as recognition and praise to motivate involves tailoring them to the

needs and characteristics of the workers.

Giving employees timely, relevant feedback about their job performance through a

performance appraisal system can also be a powerful motivator.

Discussion Questions

S8Q1:What is leadership? What is the difference between leadership and management?

S8Q2:What behaviors do effective leaders exhibit?

S8Q3:Why is it so important for small companies to hire the right employees? What can small business owners do to

avoid making hiring mistakes?

S8Q4:What is a job description? A job specification? What functions do they serve in the hiring process?

S8Q5:Outline the procedure for conducting an effective interview.

S8Q6:What is company culture? What role does it play in a small company's success? What threats does rapid

growth pose for a company's culture?

S8Q7:What is empowerment? What benefits does it offer workers? The company? What must a small business

manager do to make empowerment work in a company?

S8Q8:Is money the "best" motivator? How do pay-for-performance compensation systems work? What other

rewards are available to small business managers to use as motivators? How effective are they?

22

SESSION IX

Sources of Funds: Equity and Debt

Chapter Summary

1. Explain the differences in the three types of capital small businesses require: fixed, working,

and growth.

Capital is any form of wealth employed to produce more wealth. Three forms of capital

are commonly identified: fixed capital, working capital, and growth capital.

Fixed capital is used to purchase a company's permanent or fixed assets; working capital

represents the business's temporary funds, and is used to support the business's normal

short-term operations; growth capital requirements surface when an existing business is

expanding or changing its primary direction.

2. Describe the various sources of equity capital available to entrepreneurs, including personal

savings, friends and relatives, angels, partners, corporations, venture capital, and public stock

offerings.

The most common source of financing a business is the owner's personal savings. After

emptying their own pockets, the next place entrepreneurs turn for capital is family

members and friends. Angels are private investors who not only invest their money in

small companies, but they also offer valuable advice and counsel to them. Some

business owners have success financing their companies by taking on limited partners as

investors or by forming an alliance with a corporation, often a customer or a supplier.

Venture capital companies are for-profit, professional investors looking for fast-growing

companies in "hot" industries. When screening prospects, venture capital firms look for

competent management, a competitive edge, a growth industry, and important

intangibles that will make a business successful. Some owners choose to attract capital

by taking their companies public, which requires registering the public offering with the

SEC.

3. Describe the process of "going public," as well as its advantages and disadvantages

Going public involves: 1. choosing the underwriter, 2. negotiating a letter of intent, 3.

preparing the registration statement, 4. file with the SEC, and 5. meet state requirements.

Going public offers the advantages of raising large amounts of capital, improved access

to future financing, improved corporate image, and gaining listing on a stock exchange.

The disadvantages include dilution of the founder's ownership, loss of privacy, reporting

to the SEC, filing expenses, and accountability to shareholders.

4. Explain the various simplified registrations and exemptions from registration available to

small businesses wanting to sell securities to investors.

Rather than go through the complete registration process, some companies use one of the

simplified registration options and exemptions available to small companies: Regulation

S-B, Regulation D (Rule 504) Small Company Offering Registration (SCOR), Regulation

D (Rule 505, and Rule 506) Private Placements, Section 4(6), Rule 147, Regulation A,

direct stock offerings, and foreign stock markets.

23

5. Describe the various sources of debt capital and the advantages and disadvantages of each.

Commercial banks offer the greatest variety of loans, although they are conservative

lenders. Typical short-term bank loans include commercial loans, lines of credit,

discounting accounts receivable, inventory financing, floor planning, and character loans.

6. Explain the types of financing available from nonblank sources of credit.

Asset-based lenders allow small businesses to borrow money by pledging otherwise idle

assets such as accounts receivable, inventory, or purchase orders as collateral.

Trade credit is used extensively by small businesses as a source of financing. Vendors

and suppliers commonly finance sales to businesses for 30, 60, or even 90 days.

Equipment suppliers offer small businesses financing similar to trade credit but with

slightly different terms.

Commercial finance companies offer many of the same types of loans that banks do, but

they are more risk oriented in their lending practices. They emphasize accounts

receivable financing and inventory loans.

Savings and loan associations specialize in loans to purchase real property—commercial

and industrial mortgages—for up to 30 years.

Stockbrokerage houses offer loans to prospective entrepreneurs at lower interest rates

than banks because they have high-quality, liquid collateral— stocks and bonds in the

borrower’s portfolio.

Insurance companies provide financing through policy loans and mortgage loans. Policy

loans are extended to the owner against the cash surrender value of insurance policies.

Mortgage loans are made for large amounts and are based on the value of the land being

purchased.

Small Business Investment Companies are privately owned companies licensed and

regulated by the SBA that qualify for SBA loans to be invested in or loaned to small

businesses.

Small Business Lending Companies make only intermediate and long-term loans that are

guaranteed by the SBA.

7. Identify the sources of government financial assistance and the loan programs these agencies

offer.

The Economic Development Administration, a branch of the Commerce Department,

makes loan guarantees to create and expand small businesses in economically depressed

areas.

The Department of Housing and Urban Development extends grants (such as Community

Development Block Grants) to cities that, in turn, lend and grant money to small

businesses in an attempt to strengthen the local economy.

The Department of Agriculture’s Rural Business-Cooperative Service loan program is

designed to create nonfarm employment opportunities in rural areas through loans and

loan guarantees.

The Small Business Innovation Research Program involves 10 federal agencies that

award cash grants or long-term contracts to small companies wanting to initiate or to

expand their research and development (R&D) efforts.

The Small Business Technology Transfer Program allows researchers at universities,

federally funded R&D centers, and nonprofit research institutions to join forces with

small businesses and develop commercially promising ideas.

8. Describe the various loan programs available from the Small Business Administration.

Almost all SBA loan activity is in the form of loan guarantees rather than direct loans.

Popular SBA programs include Low Doc Program, the SBA Express Program, the 7(A)

loan guaranty program, the CAPLine Program, the Export Working Capital Program, the

24

Section 504 Certified Development Company program, the microloan program, the

Prequalification Loan Program, the disaster loan program, and the 8(a) program.

Many state and local loan and development programs, such as Capital Access Programs

and Revolving Loan Funds, complement those sponsored by federal agencies.

9. Discuss state and local economic development programs.

In an attempt to develop businesses that create jobs and economic growth, most states

offer small business financing programs, usually in the form of loans, loan guarantees,

and venture capital pools.

10. Discuss valuable methods of financing growth and expansion internally with bootstrap

financing.

Small business owners may also look inside their firms for capital. By factoring accounts

receivable, leasing equipment instead of buying it, and by minimizing costs, owners can

stretch their supplies of capital.

11. Explain how to avoid becoming a victim of a loan scam.

Entrepreneurs hungry for capital for their growing businesses can be easy targets for con

artists running loan scams. Entrepreneurs should watch out for promises of “guaranteed”

loans, up-front fees, pitches over the World Wide Web, and Nigerian letter scams.

Discussion Questions

S9Q1:Why is it so difficult for most small business owners to raise the capital needed to start, operate, or expand

their ventures?

S9Q2:What is capital? List and describe the three types of capital a small business needs for its operations.

S9Q3:Define equity financing. What advantage does it offer over debt financing?

S9Q4:What is the most common source of equity funds in a typical small business? If an owner lacks sufficient

equity capital to invest in the firm, what options are available for raising it?

S9Q5:What is an "angel?" Assemble a brief profile of the typical private investor. How can entrepreneurs locate

potential angels to invest in their businesses?

S9Q6:What types of businesses are most likely to attract venture capital? What investment criteria do venture

capitalists use when screening potential businesses? How do these compare to the typical angel's criteria?

S9Q7:How do venture capital firms operate? Describe their procedure for screening investment proposals?

S9Q8:What role do commercial banks play in providing debt financing to small businesses? Outline and briefly

describe the major types of short-term, intermediate, and long-term loans commercial banks offer.

S9Q9:What is trade credit? How important is it as a source of debt financing to small firms?

S9Q10:Explain how asset-based financing works. What is the most common method of asset-based financing?

What are the advantages and disadvantages of using this method of financing?

S9Q11:How can a firm employ bootstrap financing to stretch its current capital supply?

S9Q12:What is a factor? How does the typical factor operate? Explain the advantages and the disadvantages of

factoring. What kinds of businesses typically use factors?

25

SESSION X

Case Studies: Businesss in a Global Environment

Chapter Summary

Introduction

In the context of the course, opportunities in international Business will be examined in terms

of doing business data.

The business environment

For policy makers trying to improve their economy’s regulatory environment for business, a

good place to start is to find out how it compares with the regulatory environment in other

economies. Doing Business provides an aggregate ranking on the ease of doing business based

on indicator sets that measure and benchmark regulations applying to domestic small to mediumsize businesses through their life cycle. Economies are ranked from 1 to 189 by the ease of doing

business index. For each economy the index is calculated as the ranking on the simple average of

its percentile rankings on each of the 10 topics included in the index in Doing Business 2014:

starting a business, dealing with construction permits, getting electricity, registering property,

getting credit, protecting investors, paying taxes, trading across borders, enforcing contracts and

resolving insolvency. The ranking on each topic is the simple average of the percentile rankings

on its component indicators (see the data notes for more details). The employing workers

indicators are not included in this year’s aggregate ease of doing business ranking, but the data

are presented in this year’s economy profile.

Starting a business

Formal registration of companies has many immediate benefits for the companies and for

business owners and employees. Legal entities can outlive their founders. Resources are pooled

as several shareholders join forces to start a company. Formally registered companies have

access to services and institutions from courts to banks as well as to new markets. And their

employees can benefit from protections provided by the law. An additional benefit comes with

limited liability companies. These limit the financial liability of company owners to their

investments, so personal assets of the owners are not put at risk. Where governments make

registration easy, more entrepreneurs start businesses in the formal sector, creating more good

jobs and generating more revenue for the government.

Dealing with construction permits

Regulation of construction is critical to protect the public. But it needs to be efficient, to avoid

excessive constraints on a sector that plays an important part in every economy. Where

complying with building regulations is excessively costly in time and money, many builders opt

out. They may pay bribes to pass inspections or simply build illegally, leading to hazardous

construction that puts public safety at risk. Where compliance is simple, straightforward and

inexpensive, everyone is better off.

26

Getting electricity

Access to reliable and affordable electricity is vital for businesses. To counter weak electricity

supply, many firms in developing economies have to rely on self-supply, often at a prohibitively

high cost. Whether electricity is reliably available or not, the first step for a customer is always to

gain access by obtaining a connection.

Registering property

Ensuring formal property rights is fundamental. Effective administration of land is part of that. If

formal property transfer is too costly or complicated, formal titles might go informal again. And

where property is informal or poorly administered, it has little chance of being accepted as

collateral for loans—limiting access to finance.

Getting credit

Two types of frameworks can facilitate access to credit and improve its allocation: credit

information systems and borrowers and lenders in collateral and bankruptcy laws. Credit

information systems enable lenders’ rights to view a potential borrower’s financial history

(positive or negative)—valuable information to consider when assessing risk. And they permit

borrowers to establish a good credit history that will allow easier access to credit. Sound

collateral laws enable businesses to use their assets, especially movable property, as security to

generate capital—while strong creditors’ rights have been associated with higher ratios of private

sector credit to GDP.

Protecting investors

Protecting investors matters for the ability of companies to raise the capital they need to grow,

innovate, diversify and compete. If the laws do not protect minority shareholders, investors may

be reluctant to provide funding to companies through the purchase of shares unless they become

the controlling shareholders. Effective regulations define related-party transactions precisely,

promote clear and efficient disclosure requirements, require shareholder participation in major

decisions of the company and set detailed standards of accountability for company insiders.

Paying taxes

Taxes are essential. They fund the public amenities, infrastructure and services that are crucial

for a properly functioning economy. But the level of tax rates needs to be carefully chosen—and

needless complexity in tax rules avoided. According to Doing Business data, in economies where

it is more difficult and costly to pay taxes, larger shares of economic activity end up in the

informal sector—where businesses pay no taxes at all.

27

Trading across borders

In today’s globalized world, making trade between economies easier is increasingly important

for business. Excessive document requirements, burdensome customs procedures, inefficient port

operations and inadequate infrastructure all lead to extra costs and delays for exporters and

importers, stifling trade potential. Research shows that exporters in developing countries gain

more from a 10% drop in their trading costs than from a similar reduction in the tariffs applied to

their products in global markets.

Enforcing contracts

Effective commercial dispute resolution has many benefits. Courts are essential for entrepreneurs

because they interpret the rules of the market and protect economic rights. Efficient and

transparent courts encourage new business relationships because businesses know they can rely

on the courts if a new customer fails to pay. Speedy trials are essential for small enterprises,

which may lack the resources to stay in business while awaiting the outcome of a long court

dispute.

Resolving insolvency

A robust bankruptcy system functions as a filter, ensuring the survival of economically efficient

companies and reallocating the resources of inefficient ones. Fast and cheap insolvency

proceedings result in the speedy return of businesses to normal operation and increase returns to

creditors. By improving the expectations of creditors and debtors about the outcome of

insolvency proceedings, well-functioning insolvency systems can facilitate access to finance,

save more viable businesses and thereby improve growth and sustainability in the economy

overall.

Employing workers

Employing workers measures flexibility in the regulation of employment, specifically as it

affects the hiring and redundancy of workers and the rigidity of working hours.

Discussion Questions

S10Q1: Compare and contrast the business environment in your country and

Germany

S10Q2: Compare and contrast starting a business in your country and Germany

S10Q3: Compare and contrast dealing with construction permits in your country and Germany

S10Q4: Compare and contrast getting credit in your country and Germany

S10Q5: Compare and contrast protecting investors in your country and Germany

S10Q6: Compare and contrast paying taxes in your country and Germany

S10Q7: Compare and contrast trading across borders in your country and

Germany

S10Q8: Compare and contrast enforcing contracts in your country and Germany

S10Q9: Compare and contrast resolving insolvency in your country and

Germany

S10Q10: Compare and contrast employing workers in your country and Germany

28