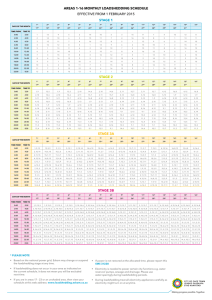

Cost of Loadshedding to Agriculture

advertisement