Electronic Payment Systems

advertisement

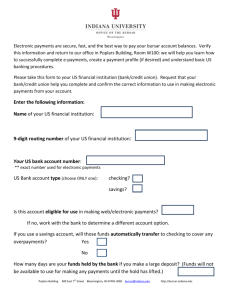

Chapter 3 E-Payment Systems eb-course.weebly.com Agenda • Definition of electronic payment • Security for e-payments • Types of electronic payment methods • Which electronic payments to accept? Payment Methods Payment: The transfer of money from one individual or legal entity to another – – – – – Cash Personal Cheques Money orders (Bank note) Credit cards Debit cards 3 What is electronic payment • Electronic payment methods are the payments made electronically rather than by paper (cash, checks, vouchers, etc) • Allows global reach, high speed, low transaction cost and high automatibility Security for E-payments If you are running an e-commerce site, you need to worry about • Authentication – Authenticity of business • Confidentiality – Information privacy • Data Integrity – Data must not be altered • Audit Trail – Data should be trailed Security for E-payments • Standards for E-payments – It is a must to have a generally accepted protocol for securing e-payments such as SSL / SET • Implemented protocols – SSL (Secure Sockets Layer) • Security protocol used by web browser and web server to transmit sensitive information over the internet • Uses private key to encrypt data – SET (Secure Electronic Transaction) • Built with SSL • Uses digital wallet that holds customers certificates Secure Sockets Layer (SSL) • Created by Netscape for secure message transmission. • Uses public-key encryption • Browser is the client • Netscape servers can be enabled for SSL • Other servers can be enabled by installing the Netscape SSLRef program library Secure Socket Layers (SSL) protocol • Certificate Authority – Ex) Verisign • Secures credit card payments • Provides 40 bit and 128 bit SSL Encryption • Authenticates the business for customer confidence Secure Electronic Transaction (SET) • Visa and MasterCard developed SET specifically to handle electronic payments • Based on cryptography and digital certificates • Digital certificates uniquely identify the parties to a transaction – An electronic credit card – Registries for authentication • A digital signature is used to guarantee a sender’s identity Secure Electronic Transmission (SET) SET involves interaction among credit card holders, merchants, issuing banks, payment processing organizations, and public key certificate authorities so it’s much more secure than SSL Purchase is Requested Transaction is Approved SET Encryption Request is Sent to E-commerce Server Merchant Sends Record to Bank Bank Credits Merchant’s Account E-Commerce Server Verifies Transaction The SET protocol The SET protocol coordinates the activities of the customer, merchant, merchant’s bank, and card issuer. [Source: Stein] Secure Electronic Transaction (SET) Protocol • SET is much more complex – Success of SSL – Expensive overhead Types of Electronic Payment • B2B – Small to large payments • B2C – Small to medium payments – Credit card transactions • Micropayments – Very small payments Types of Electronic payments (B2B) • • • • Electronic checks Purchasing cards Electronic letters of credit Electronic Funds Transfer – Transfer of funds • Ex) ATM, Internet banking • Electronic Benefits Transfer – Transfer of benefits • Ex) Debit card for food stamps Types of Electronic Payments (B2C) • Electronic Payment Cards – (credit, debit, charge) • Smart Cards – (phone cards, bank cards) • P2P payments – (paypal, c2it) • Other payment methods Electronic payment cards (1) • Credit cards – – – – Most popular online payment Convenient for both merchant and customer Quicker payments 24/7 Safest recommended method • Liability is limited by federal law to $50 for unauthorized charge on credit card Electronic payment cards (2) • How credit card works Smart Card (1) • A type of computer embedded chip card that stores and transacts encrypted data between users. • Smart card are used in healthcare, banking, entertainment and transportation industries. • Offers enhanced security, convenience and economic benefits • Rechargeable stored value card – Examples • Mondex in UK • VisaCash in US Smart Card (2) • Smart Card for E-Commerce – Advantages • Carry personal Accounts • Credit and buying preferences • Manage and control expenditures with automatic limits and reporting – Disadvantages • Costs 2 to 7 times more than magnetic stripe cards • Need a smart card reader Smart Card (3) • NTT-DoCoMo, Japan’s leading communications company have tied up with coca-cola company and developed a mobile commerce platform (cmode) that allow purchasing soft drinks using cell phones. http://www.nttdocomo.com/corebiz /imode/alliances/cmode.html P2P Payments • Person to person payments are newest and fastest growing e-payment schemes. • Able to transmit funds to anyone with an email address – ex) Paypal • • • • Free to send money to anyone Over 50 million account holders in 45 countries State of the art security technology Buyer protection up to $1,000 with no extra charge Types of Electronic Payments (Micropayments) • Allows very small charges for goods and services • Very small payments usually below $10 – Ex) Digital music • Credit cards or EFT are too expensive – Credit card charges 25 cents to 35 cents and 2 to 3 percent of purchase price • Difficult to allocate payment – Hard to split between issuing bank, paying bank, card processor, and etc) • New business model made possible by innovation of IT Other E-payment methods • Wireless payments – “M-pay bill” from Vodafone • E-check – Electronic version of paper check • www.electracash.com • E-charge – Charge purchases to local phone bill • www.echarge.com Accepting Electronic Payments (B2C) • Merchant Account – Payment processing opened through a bank • Ex) www.1stamericancardservice.com • Third Party Processor – Payment processor that accepts credit cards on behalf of your company • Ex) www.2checkout.com, www.paypal.com Merchant Account • Advantages – Increase credibility – Flexibility • Able to sell any kind of products and services • Own shopping cart – Low discount rate • Average 2-3% • Disadvantages – Difficult to obtain – Expensive • Large set up fee, application fee, gateway fee, monthly statement fee and monthly minimum fee – Ex) 1stAmericanCardService: $185 start up fee, $9 statement fee and etc Third Party Processor • Advantages – – – – Easy to obtain Small set up fee, no monthly fees, no gateway fees Accepts most credit card, debit card, checks Less administrative work • Disadvantages – Don’t have public acceptance • Must use their shopping cart system – Gives less confidence to purchaser – Limited items • Paypal restricted item’s list – Higher transaction fees • 2checkout: 5.5% of sale amount plus 45 cents per sale • Digibuy: 13.9% of sales amount Things to consider • Monthly sales volume – Low volume: Third party processor – High volume: Merchant account • Types of products or services • International support – Multi-currency – Multi-language • Marketing assistance or reseller affiliates – 2checkout shopping mall – Yahoo! Shopping