Chapter

12-1

Chapter 12:

Computer Controls for Organizations and

Accounting Information Systems

Introduction

General Controls for Organizations

General Controls for Information Technology

Application Controls for Transaction

Processing

Chapter

12-2

General Controls For

Organizations

Integrated Security for the Organization

Organization-Level Controls

Personnel Policies

File Security Controls

Business Continuity Planning

Computer Facility Controls

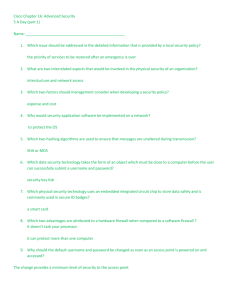

Computer Access Controls

Chapter

12-3

Developing a Security

Policy

Chapter

12-4

Integrated Security for

the Organization

Physical Security

Measures

used to protect its facilities, resources,

or proprietary data stored on physical media

Logical Security

Limit

access to system and information to

authorized individuals

Integrated Security

Combines

physical and logical elements

Supported by comprehensive security policy

Chapter

12-5

Physical and Logical Security

Chapter

12-6

Organization-Level Controls

Consistent policies and procedures

Management’s risk assessment process

Centralized processing and controls

Controls to monitor results of operations

Chapter

12-7

Organization-Level Controls

Controls to monitor the internal audit

function, the audit committee, and selfassessment programs

Period-end financial reporting process

Board-approved policies that address

significant business control and risk

management practices

Chapter

12-8

Personnel Policies

Separation of Duties

Separate

Accounting and Information Processing

from Other Subsystems

Separate Responsibilities within IT Environment

Use of Computer Accounts

Each

employee has password protected account

Biometrics

Chapter

12-9

Separation of Duties

Chapter

12-10

Division of Responsibility in

IT Environment

Chapter

12-11

Division of Responsibility in

IT Environment

Chapter

12-12

Personnel Policies

Informal Knowledge of Employees

Protect

against fraudulent employee actions

Observation of suspicious behavior

Highest percentage of fraud involved employees

in the accounting department

Must safeguard files from intentional and

unintentional errors

Chapter

12-13

Safeguarding Computer Files

Chapter

12-14

File Security Controls

Chapter

12-15

Business Continuity Planning

Definition

Comprehensive

approach to ensuring normal

operations despite interruptions

Components

Disaster

Recovery

Fault Tolerant Systems

Backup

Chapter

12-16

Disaster Recovery

Definition

Process

and procedures

Following disruptive event

Summary of Types of Sites

Hot

Site

Flying-Start Site

Cold Site

Chapter

12-17

Fault Tolerant Systems

Definition

Used

to deal with computer errors

Ensure functional system with accurate and

complete data (redundancy)

Major Approaches

Consensus-based

protocols

Watchdog processor

Utilize disk mirroring or rollback processing

Chapter

12-18

Backup

Batch processing

Risk

of losing data before, during, and after

processing

Grandfather-parent-child procedure

Types of Backups

Hot

backup

Cold Backup

Electronic Vaulting

Chapter

12-19

Batch Processing

Chapter

12-20

Computer Facility Controls

Locate Data Processing Centers in Safe Places

Protect from

the public

Protect from natural disasters (flood, earthquake)

Limit Employee Access

Security

Badges

Man Trap

Buy Insurance

Chapter

12-21

Study Break #1

A _______ is a comprehensive plan that helps protect the

enterprise from internal and external threats.

A.

B.

C.

D.

Firewall

Security policy

Risk assessment

VPN

Chapter

12-22

Study Break #1 - Answer

A _______ is a comprehensive plan that helps protect the

enterprise from internal and external threats.

A.

B.

C.

D.

Firewall

Security policy

Risk assessment

VPN

Chapter

12-23

Study Break #2

All of the following are considered organization-level controls

except:

A.

B.

C.

D.

Personnel controls

Business continuity planning controls

Processing controls

Access to computer files

Chapter

12-24

Study Break #2 - Answer

All of the following are considered organization-level controls

except:

A.

B.

C.

D.

Personnel controls

Business continuity planning controls

Processing controls

Access to computer files

Chapter

12-25

Study Break #3

Fault-tolerant systems are designed to tolerate computer errors

and are built on the concept of _________.

A.

B.

C.

D.

Redundancy

COBIT

COSO

Integrated security

Chapter

12-26

Study Break #3 - Answer

Fault-tolerant systems are designed to tolerate computer errors

and are built on the concept of _________.

A.

B.

C.

D.

Redundancy

COBIT

COSO

Integrated security

Chapter

12-27

General Controls for

Information Technology

Security for Wireless Technology

Controls for Networks

Controls for Personal Computers

IT Control Objectives for Sarbanes-Oxley

Chapter

12-28

General Controls for

Information Technology

IT general controls apply to all information

systems

Major Objectives

Computer

programs are authorized, tested, and

approved before usage

Access to programs and data is limited to

authorized users

Chapter

12-29

Control Concerns

Chapter

12-30

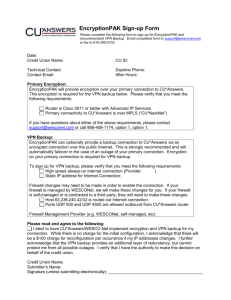

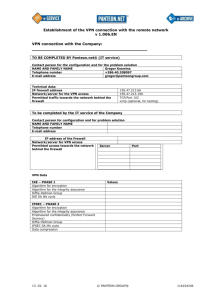

Security for Wireless Technology

Utilization of wireless local area networks

Virtual Private Network (VPN)

Allows

remote access to entity resources

Data Encryption

Data

converted into a scrambled format

Converted back to meaningful format following

transmission

Chapter

12-31

Controls for Networks

Control Problems

Electronic

eavesdropping

Hardware or software malfunctions

Errors in data transmission

Control Procedures

Checkpoint

control procedure

Routing verification procedures

Message acknowledgment procedures

Chapter

12-32

Controls for Personal Computers

Take an inventory of personal computers

Applications utilized by each personal

computer

Classify computers according to risks and

exposures

Physical security

Chapter

12-33

Additional Controls for Laptops

Chapter

12-34

IT Control Objectives for

Sarbanes-Oxley

“IT Control Objectives for Sarbanes-Oxley”

Issued

by IT Governance Institute (ITGI)

Provides guidance for compliance with SOX and

PCAOB requirements

Content

IT

controls from COBIT

Linked to PCAOB standards

Linked to COSO framework

Chapter

12-35

Application Controls

for Transaction Processing

Purpose

Embedded

in business process applications

Prevent, detect, and correct errors and

irregularities

Application Controls

Input

Controls

Processing Controls

Output Controls

Chapter

12-36

Application Controls

for Transaction Processing

Chapter

12-37

Input Controls

Purpose

Ensure

validity

Ensure accuracy

Ensure completeness

Categories

Observation,

recording, and transcription of data

Edit

tests

Additional input controls

Chapter

12-38

Observation, Recording,

and Transcription of Data

Confirmation mechanism

Dual observation

Point-of-sale devices (POS)

Preprinted recording forms

Chapter

12-39

Preprinted Recording Form

Chapter

12-40

Edit Tests

Input Validation Routines (Edit Programs)

Programs

or subroutines

Check validity and accuracy of input data

Edit Tests

Examine

selected fields of input data

Rejects data not meeting preestablished standards

of quality

Chapter

12-41

Edit Tests

Chapter

12-42

Edit Tests

Chapter

12-43

Additional Input Controls

Unfound-Record Test

Transactions

matched with master data files

Transactions lacking a match are rejected

Check-Digit Control Procedure

Modulus 11 Technique

Chapter

12-44

Processing Controls

Purpose

Focus

on manipulation of accounting data

Contribute

to a good audit trail

Two Types

Control totals

Data manipulation controls

Chapter

12-45

Audit Trail

Chapter

12-46

Control Totals

Common Processing Control Procedures

Batch

control total

Financial control total

Nonfinancial control total

Record count

Hash total

Chapter

12-47

Data Manipulation Controls

Data Processing

Following

validation of input data

Data manipulated to produce decision-useful

information

Processing Control Procedures

Software

Documentation

Error-Testing Compiler

Utilization of Test Data

Chapter

12-48

Output Controls

Purpose

Ensure

validity

Ensure accuracy

Ensure completeness

Major Types

Validating

Processing Results

Regulating Distribution and Use of Printed Output

Chapter

12-49

Output Controls

Validating Processing Results

Preparation

of activity listings

Provide detailed listings of changes to master files

Regulating Distribution and Use of Printed

Output

Forms

control

Pre-numbered forms

Authorized distribution list

Chapter

12-50

Study Break #4

A ______ is a security appliance that runs behind a firewall

and allows remote users to access entity resources by using

wireless, hand-held devices.

A.

B.

C.

D.

Data encryption

WAN

Checkpoint

VPN

Chapter

12-51

Study Break #4 - Answer

A ______ is a security appliance that runs behind a firewall

and allows remote users to access entity resources by using

wireless, hand-held devices.

A.

B.

C.

D.

Data encryption

WAN

Checkpoint

VPN

Chapter

12-52

Study Break #5

Organizations use ______ controls to prevent, detect, and

correct errors and irregularities in transactions that are

processed.

A.

B.

C.

D.

Specific

General

Application

Input

Chapter

12-53

Study Break #5 - Answer

Organizations use ______ controls to prevent, detect, and

correct errors and irregularities in transactions that are

processed.

A.

B.

C.

D.

Specific

General

Application

Input

Chapter

12-54

Copyright

Copyright 2010 John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that permitted in

Section 117 of the 1976 United States Copyright Act without the

express written permission of the copyright owner is unlawful.

Request for further information should be addressed to the

Permissions Department, John Wiley & Sons, Inc. The purchaser

may make backup copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions,

or damages, caused by the use of these programs or from the use of the

information contained herein.

Chapter

12-55

Chapter 12

Chapter

12-56