Chapter 1

advertisement

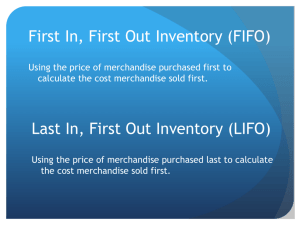

Financial Merchandise Management Financial Merchandise Management Financial Merchandise Management A retailer specifies which products are purchased, when products are purchased, and how many products are purchased encompasses merchandising budgets and forecasts, accounting systems and integrated dollar and unit controls. Dollar control - planning and monitoring the financial investment in merchandise Unit control – planning and monitoring the quantities of merchandise handled Two ways to account for merchandise: Cost accounting system - values merchandise at cost plus inbound transportation charges Retail accounting system - values merchandise at current retail prices Disadvantages of Cost-Based Inventory Systems Requires that a cost be assigned to each item in stock Problematic because UPC labels and price tags record retail dollar value Requires a complex coding process to match cost with items during physical inventory counts FIFO v. LIFO Does not adjust inventory values to reflect style changes, end-of-season markdowns, or sudden surges of demand The Retail Method Closing inventory is determined by calculating the average relationship between the cost and retail values of merchandise available for sale during a period To do this, you must: 1. 2. 3. Calculate the cost complement Calculate deductions from retail value Convert retail inventory value to cost Advantages of the Retail Method Valuation errors are reduced when conducting a physical inventory since merchandise value is recorded at retail and costs do not have to be decoded Because the process is simpler, a physical inventory can be completed more often Profit-and-loss statement can be based on book inventory Method gives an estimate of inventory throughout the year and is accepted in insurance claims Limitations of the Retail Method Bookkeeping burden of recording data Ending book inventory figures correctly computed only if the following are accurate: Value of beginning inventory Purchases Shipping charges Markups Markdowns Employee discounts Transfers Returns Sales Cost complement is an average based on the total cost of merchandise available for sale and total retail value Chapter 16 Discussion Questions Small Group exercise Take a few minutes to compare your answers to discussion questions 8, 9, 12, 14 Takeaways Careful merchandise analysis, planning and forecasting can reduce some of the problems commonly associated with inventory (being out-of-stock, being stuck with excess merchandise, linking shelf space with revenues, fad merchandise, predicting customer demand) Financial merchandise management lets you know what you have on hand and how much you can purchase in a time period helps determine shelf space requirements by knowing Beg. and End. inventory levels Can be used as a control mechanism (for both inventory effectiveness but also buyer performance)