Presentation - Federal Reserve Bank of Atlanta

advertisement

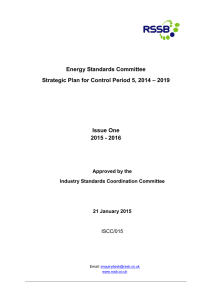

Dealing with the international financial crisis from a SOE: emerging issues. Gerardo Licandro Conference: “Quantitative Approaches to Monetary Policy in Open Economies.” Structure of the presentation • Financial Crisis: a view from the periphery – Some background facts on the uruguayan economy – Three stages in crisis administration • Until Lehman • From Lehman until early 2009 • Recent events – emerging issues for the international financial system • Some questions for the long run Background notes on Uruguay • SOE. Oil importing, agriculture accounts for more than 50% of gross production value • High exposure to the region on goods imports and service exports • Record liability dollarization (decreasing) • Financial crisis in 2002 legacy – More than 80% of deposits are short term – Low levels of banking credit • Recent macro performance – – – – Average growth 2003-2007 above 6% Inflation ranged between 3-10% Debt /GDP halved Structural fiscal result close to equilibrium. Steady reduction in spending/GDP – Unemployment in lowest recorded level (7%) The crisis until Lehman • Strong capital inflows from late 2007 til the first semester of 2008 • Soaring commodity prices • Domestic impact – – – – Booming investment Rising prices of food Strong pressures in the exchange market Rapidly growing fiscal revenue • Policy response – – – – Monetary policy: Reserve accumulation through sterilized intervention Spike in reserve requirements Asset management: flight from housing assets Response of prudential regulation: control on asset composition of banks – Debt. Allow change in portfolio of private sector through debt exchanges The answer to financial panic • Financial panic resulted in a change in the currency composition of the portfolio of the private sector. Two conflicting forces led to this result – World deleveraging led to the cancellation of positions on domestic currency – Deleveraging in Argentina brought dollar deposits to Uruguay. • Plummeting commodity prices reduced inflation • The priority in this environment turned to avoiding contagion. Policymakers decided to let interest rates go to minimize the use of reserves, while reducing excess volatility on the exchange rate. Uncertainty about the lenght, depht and severity of the crisis was key. • Debt policy: debt exchanges, for limited amounts to allow portfolio change and reduce pressure on the exchange rate market. Sign contingent lines with IIFs • Prudential response: preserve the assets of the banking sector. Run on banks in trouble. • Fiscal policy. Limited space due to prior spending commitments. Lessons? • Lack of international financial safety net might lead to coordination failures in the response to the panic. – Idiosincratic prudential response deepens financial panic. – International reserve allocation followed a similar pattern. • Renewed influence of commodity prices leave the question of its sustainability. Should we have stabilization funds? The long term questions • More regulation and less financial intermediation? • How do we solve the debt overhang in developed countries?.> – Are emerging markets going to pay through inflation? – Is there going to be an adjustment of consumption? • Effects of Contractionary environment – Competitive monetary policies? – Competitive trade policies? – Closing capital accounts? • Reduction in long run growth? • loss of confidence on the US currency?. Is US’s debt sustainable? Dealing with the international financial crisis from a SOE: emerging issues. Gerardo Licandro Conference: “Quantitative Approaches to Monetary Policy in Open Economies.” Bye bye fear of floating? Argentina 1981 Indice ene 80=100 350 Brasil 1999 Indice ene 98=100 180 170 160 300 150 Var mar/set 81 250 140 $ argentino: 139% $ uruguayo: 7% 200 Var ene/jun 99 real: 47% $ uruguayo: 5% 130 120 150 110 100 100 90 50 Argentina 2001 Indice ene 01=100 400 120 m ay -9 9 -9 9 m ar en e99 v98 no se p -9 8 8 ju l-9 m ay -9 8 -9 8 Subprime crisis2008 Indice ene 07=100 110 350 Var. ene/jun 02 300 $ argentino: 260% $ uruguayo: 26% 250 100 90 Var mar09/ago 08 Fuente. BCRA, IPEA, INE y Pacific Exchange Rate. ar -0 9 m no v08 en e09 se p08 8 ju l-0 ay -0 8 en e07 m ar -0 7 m ay -0 7 -0 2 M ay -0 2 M ar 2 e0 En 01 ov N Se p0 1 1 l-0 Ju -0 1 M ay -0 1 M ar e0 1 60 m 0 real: 44% €: 16% $ uruguayo: 24% ar -0 8 70 50 m 100 no v07 en e08 80 7 se p07 150 ju l-0 200 En m ar e98 en p81 1 se ju l-8 m ay -8 1 -8 1 m ar en e81 v80 no 0 p80 se ju l-8 m ay -8 0 -8 0 m ar en e80 80