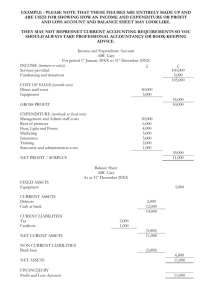

Movement in Reserves Statement

advertisement