Marta Borda

advertisement

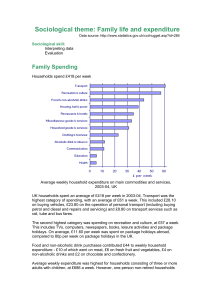

4TH INTERNATIONAL CONFERENCE - SOCIAL SECURITY SYSTEMS IN THE LIGHT OF DEMOGRAPHIC, ECONOMIC AND TECHNOLOGICAL CHALLENGES FINANCIAL SITUATION OF HOUSEHOLDS IN POLAND IN THE CONTEXT OF DEVELOPMENT OF PRIVATE HEALTH CARE FINANCING MECHANISMS Marta Borda Department of Insurance Wroclaw University of Economics Poland Poznań, September 24-25, 2015 PLAN OF PRESENTATION • Introduction • General analysis of households’ financial situation in 2000-2013 • Selected measures of households’ financial condition according to basic socio-economic groups and quintile groups by available income per capita • Conclusions HEALTH CARE FINANCING IN POLAND – MAIN CHARACTERISTICS HEALTH CARE FINANCING IN POLAND – MAIN CHARACTERISTICS TABLE 1. HEALTH CARE FINANCING IN POLAND – SELECTED RATIOS Characteristic Total health care expenditure as % of GDP Total health care expenditure per capita (USD PPP) Years 1995 2000 2005 2010 2013 5.5 5.5 6.2 7.0 6,4* 409.0 583.5 856.6 1394.9 1550.7 72.9 70.0 69.3 71.2 69.6 27.1 29.98 30.64 28.42 30.3 27.12 29.98 26.16 22.24 22.81 100 100 85.36 78.26 75.0 Public expenses as % of total health care expenses Private expenses as % of total health care expenses Household out-of-pocket expenses as % of total health care expenses Household out-of-pocket expenses as % of private health care expenses Source: WHO Health for All Database, *OECD Health Data. Figure 3. The dynamics of real available income and expenditure per capita in households in Poland, 2000‐2013 Source: author’s own calculations based on data from Central Statistical Office of Poland. Statistical interdependences between average monthly health expenditure and average monthly available income per capita in households in Poland, 2000‐2013 Figure 4. The relationship between average monthly health expenditure and average monthly available income per capita in households in Poland, 2000‐2013 Source: author’s own calculations based on data from Central Statistical Office of Poland. Figure 5. The share of total expenditure, health expenditure and current savings in available income in households, 2000‐2013 (in %) Source: author’s own calculations based on data from Central Statistical Office of Poland. Figure 6. Health expenditure incurred by the Polish households, 2000‐2013 Source: author’s own calculations based on data from Central Statistical Office of Poland. Figure 7. Average monthly household health expenditure per capita by socio-eonomic groups, 2006‐2013 Source: author’s own calculations based on data from Central Statistical Office of Poland. Figure 9. Average monthly household health expenditure per capita by quintile groups, 2006‐2013 Source: author’s own calculations based on data from Central Statistical Office of Poland. CONCLUSIONS • In the analyzed period, with the increase in income the households increased their health expenditure. The rise of health expenditure resulted mainly from increasing purchase of medicines and other pharmaceutical products and the use of outpatient care services. • The lowest level of spending on health was observed in the case of farmers, and households with the lowest incomes. The most burdened with health expenditure in relation to their financial possibilities were retirees and pensioners. The development of private health insurance would result in limiting the further growth of direct health expenditure of households, which in contrast to the regular insurance premium are often a burden on a household budget. CONCLUSIONS • The interest in private health insurance depends on the financial situation of households. The most favorable financial situation, allowing to increase health spending and savings accumulation was observed in the case of self-employed workers, as well as the reachest households. With regard to households of farmers, retirees, pensioners and the poorest 20% of households seems rather unlikely that these households, due to the relatively unfavorable and often precarious financial situation, were interested in new solutions in private health care financing. • The results of the correlation analysis confirms that with the increase (decrease) in income households increase (decrease) value of health spending and have a larger (smaller) amount of surplus funds that can be spent on savings. It is not possible to distinguished types of households for which the analyzed relationship was the strongest or the weakest. Thank you for your attention Contact: marta.borda@ue.wroc.pl