Powerpoint

advertisement

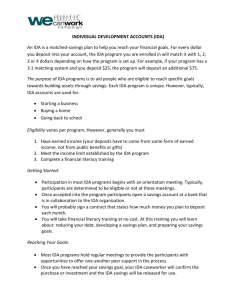

Establishing practical sovereignty through asset-based development in Native communities Peter L. Morris First Nations Development Institute Presentation to the North Australian Research Unit Darwin, NT, Australia June 28, 2005 The Problem: Control The Solution: Asset-based development The Result: Practical Sovereignty The Problem Observations from Indian Country and of the broader Indigenous experience. Adamson, ‘Land Rich, Dirt Poor’ Salway Black, ‘Redefining Success in Community Development’ The Solution Asset-based development Welfare reform in the US Asset accumulation policies to assist the middleclass The Theory Introduced by Professor Michael Sherraden: Assets and the Poor: A new American welfare strategy “Income may feed people’s stomachs but assets change their heads.” Further theoretical development Tom Shapiro and Melvin Oliver Black Wealth, White Wealth Tom Shapiro The Hidden Cost of Being African American Relevance to Indigenous policy “If assets represent potential for social and economic development, asset inequality may be the most fundamental racial issue in the United States” Sherraden, ‘Inclusion in Asset Building’ Relevance to Indigenous governance “When we think of the exercising of sovereignty, we tend to focus exclusively on the role of tribal government. But being a nation, in the fullest sense, is much more encompassing. It is about members who are engaged, productive and responsible citizens; it is about strong and vital government and other institutions; it is about a healthy and vibrant economy; it is about supportive and loving families and kinship networks; — all grounded in the values provided by a strong cultural foundation.” Salway-Black, ‘Assets: Our once and future wealth’ The Result Ability to make and enforce their own decisions as individuals, families and communities. The Australian experience – thinking outside the box when you don’t have one! Center piece – IDAs/MSAs What are Individual Development Accounts (IDAs)? Matched savings accounts Individual contributions to the account are matched by private or public funds An individual must be savings toward an asset building goal (like owning a home or starting a business) What they do Establish a banking relationship. Provide a teachable moment for financial literacy training. Affirm positive behavior. Enable accomplishment of goals. Provide an empowering pathway out of poverty. The State of the General IDA Field Widespread popularity across the United States and in a number of other countries. Investment in IDAs by more than 500 communities, 300 banks and financial institutions, 47 states, and the federal government. At least 20,000 saving in IDA accounts. Bush administration – funding for 600,000 – 900,000 additional accounts. Cultural foundations of asset-building Pre-contact “In traditional American Indian cultures, assets are given away. Think about ceremonies, like potlatches or give-aways at Pow Wows. Sharing and reciprocity are important. The whole point of possessing assets is that one can use and share them. Status and power are derived from the ability to share and to provide others in the community with the resources that they need. The pride of acquiring something is being able to give it away.” -Dr. Eddie Brown, former Assistant Secretary of Indian Affairs, Director of American Indian Studies at Arizona State University Post-contact Indigenous rights movements, cultural preservation, intellectual property. First Nations and the Native IDA Field Active involvement in Native IDAs from 1998 18-20 Native programs now in existence First Nations has awarded almost $1 million in grants to 9 existing IDA programs to date. More than 200 participants have reached their savings goal. At least 250 active participants. Well over 1000 individuals positively impacted, along with their families and communities. Early Native IDA Programs 1999 - present Cherokee Nation IDA program ALU LIKE IDA program Oklahomans for Indian Opportunity IDA program Tahlequah, OK HI – Entire state Norman, OK 2001 - present Umatilla Saves IDA program Leech Lake IDA program White Earth IDA program Pendleton, OR Cass Lake, MN Mahnomen, MN 2002 - present The Lakota Fund IDA program Kyle, SD Finished or holding Fort Hall IDA program Fort Hall, ID Redwood Valley Youth IDA program Redwood Valley, CA Warm Springs IDA program Warm Springs, OR Rapid growth 2003 (or later) - present ICE IDA program Cook Inlet Tribal Council IDA program Wind River Development Fund IDA program Salt River Pima Maricopa Indian Community IDA program Navajo Partnership for Housing Yurok Indian Housing Authority IDA program Hoopa Valley Tribe IDA program Native American Connections White Mountain Apache Housing Authority IDA Program Many in development – from Alaska to Wisconsin! Flagstaff, AZ Anchorage, AK Ft. Washakie, WY Scottsdale, AZ St Michaels, AZ Northern CA Hoopa Valley, CA Phoenix, AZ Whiteriver, AZ Integrating asset-building strategies The delivery mechanism Community Development Financial Institutions (CDFIs) The products IDAs The teachable moments Earned New Income Tax Credit (EITC) wealth Confederated Tribes of the Umatilla Indian Reservation in Pendleton, Oregon • Home Ownership Program, Match Rate 3:1 • Savings Goal =$1,500; and Match = $4,500 • Save a minimum of $60 per month for a period of 6 months or longer Confederated Tribes of the Umatilla Indian Reservation in Pendleton, Oregon • Currently: 18 participants • Two graduates on allotted land, one one fee simple, one fee simple HUD repossession The Cherokee Nation in Oklahoma: • Savings goal: $720 (2 years) – save $30 per month. • Participants must attend an orientation class, and at least 12 hours of economic literacy in the first 12 months of saving. • Individual strategies for savings and personalized budgets are developed. • Participants are required to attend asset maintenance workshops in the second 12 months of the savings period. Cherokee Nation IDA program • In the first three years, 40 participants graduated from the Cherokee Nation program. • Participants saved a total of $18,757, earned match dollars of $75,120, and leveraged approximately $298,500 of private money. Cherokee Nation IDA program – use of savings • Many new homes purchased and homes improved • George (pictured at left, with Gina Martinez, IDA Coordinator) built equity in his home and then used his home as a means to start his own business – a convenience store and gas station. • One program graduate used his funds to buy land to start a mobile home park. • Another bought a sewing machine to start a fabric crafts business. Professor Michael Sherraden “Income may feed people’s stomachs… but assets change their heads.” And their families for generations! Indigenous Community Enterprises, Arizona • Youth IDA program • Youth build Hogan homes for elders in the community • Receive financial literacy training • Receive vocational training • Save toward an asset building goal Grandma Eula Tsinnie in front of her burned Hogan-fall 2002. Construction of Grandma Tsinnie's Hogan-winter 2002 The first graduate – a transformed woman! The Result: People equipped to govern, exercising practical sovereignty. Ongoing research opportunities Developing a Native technical assistance and peer-mentoring network in the Southwest and Oklahoma Developing a Native training institute Increasing the profile of this work in the academy Possible work in Canada and Alaska Let’s keep the discussion going FIRST NATIONS DEVELOPMENT INSTITUTE Peter L. Morris 2300 Fall Hill Ave., Suite 412 Fredericksburg, VA 22401 (540) 371-5615 Fax (540) 371-3505 pmorris@firstnations.org www.firstnations.org