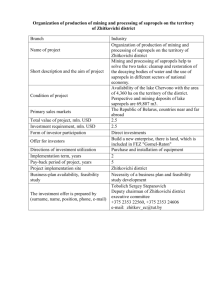

Economic/Operating Exposure

Outline

• Lufthansa case

• Operating Exposure

– Example

– Measuring operating exposure

– Managing operating exposure

• financial hedges

• business strategies

Lufthansa

• Jan. ‘85: purchased 20 Boeing 737’s for

$500 mln, payable Jan. 1986.

• What to do with the DM/$ exchange risk?

–

–

–

–

–

Remain uncovered?

Hedge 100% forward?

Hedge some forward?

Put options?

Money market hedge/prepay?

Exhibit 1 (Lufthansa) Lufthansa’s

Net Cost by Hedging Alternative

Lufthansa

• Herr Rutnau felt the dollar was overvalued, and

was likely to depreciate, reducing DM cost of

aircraft.

• But he wasn’t sure. It could appreciate (had

done so for 5 years).

• Sold 50% forward.

Exhibit 2 (Lufthansa) What Herr

Ruhnau Could See: The Rise

Lufthansa

• Herr Rutnau felt the dollar was overvalued, and

was likely to depreciate, reducing DM cost of

aircraft.

• But he wasn’t sure. It could appreciate (had

done so for 5 years).

• Sold 50% forward.

• Outcome:

– Dollar did depreciate: down 28%!!

• Rutnau heavily criticized for selling forward.

Exhibit 3 (Lufthansa) What Herr

Ruhnau Couldn’t See: The Fall

Exhibit 1 (Lufthansa) Lufthansa’s

Net Cost by Hedging Alternative

Accusations against Ruhnau

• Chose wrong time to buy Boeing. Dollar at

1980’s high in Jan. 85.

• Hedging 50% when he expected the dollar to

fall. Should have left the whole exposure

unhedged.

• Using forwards instead of options.

• Buying Boeing at all. Should have bought

Airbus.

Should Ruhnau be fired?

Operating exposure

(a.k.a. economic, competitive or strategic exposure)

• The impact of unexpected exchange rate changes upon

known and unknown but expected future cash flows of

the firm, for indefinite future.

• Firm value = discounted expected future cash flows

• Operating exposure therefore measures how firm value

changes with unexpected changes in exchange rates

Simple example

• U.S. firm expects 10 mln SF/year from

exports to Switzerland, indefinitely.

• Long-term exchange rate forecast =

current spot exchange rate

• Current rate: 2 SF/$ (.50 $/SF)

• Required rate of return: 10%/year

• What if the SF depreciates?

Year

1

2

3

SF

SF10 mln

SF10 mln

SF10 mln

forecast:

.50 $/SF

.50 $/SF

.50 $/SF ...

E[$ CF]

$5 mln

$5 mln

$5 mln

V

10%

Perpetuity formula: V = C / r

So V = $5 mln / .10 = $50 mln

...

...

...

Year

1

2

3

SF

SF10 mln

SF10 mln

SF10 mln

forecast:

.50 $/SF

.50 $/SF

.50 $/SF ...

E[$ CF]

$5 mln

$5 mln

$5 mln

$50 mln

10%

What if SF depreciates 2%, to .49 $/DM?

...

...

...

Year

1

2

3

...

SF

SF10 mln

SF10 mln

SF10 mln

forecast:

.49 $/SF

.49 $/SF

.49 $/SF ...

...

E[$ CF]

V

10%

New exchange rate implies new X-rate forecasts

Year

1

2

3

SF

SF10 mln

SF10 mln

SF10 mln

forecast:

.49 $/SF

.49 $/SF

.49 $/SF ...

E[$ CF]

$4.9 mln

$4.9 mln

$4.9 mln ...

V

10%

and new projected dollar cash flows

...

...

Year

1

2

3

SF

SF10 mln

SF10 mln

SF10 mln

forecast:

.49 $/SF

.49 $/SF

.49 $/SF ...

E[$ CF]

$4.9 mln

$4.9 mln

$4.9 mln ...

$49 mln

10%

and reduces the value of the firm by $1 mln.

...

...

Year

SF

1

2

3

SF10 mln

SF10 mln

SF10 mln

Operating exposure:

$1 mln change in firm value for

every 2% change in the current

$/SF rate

...

...

Measuring operating exposure

• Requires a longer-term perspective:

viewing the firm as an ongoing concern

with price and cost competitiveness affected

by exchange rate changes

• Requires an overall assessment of the

industry:

– Nationality of competitors & suppliers

– firm’s degree of market power

Example: Volvo

• Structure:

• Imports supplies from Germany

• produces in Sweden

• Sells in U.S.

• Major competition:

• German cars (BMW, Mercedes, Audi)

• Most important risks

• Swedish krona vs. DM (not especially vs. $)

• Swedish interest rates

• German producer prices

Measuring operating exposure

• Types of firms:

• Price-taking firms

• Price-setting firms with market power

Price-taking firms

1. Analyze impact of unexpected, persistent

exchange rate changes upon local-currency

foreign market prices, for indefinite future

– Who’s the competition?

2. Analyze impact on home-currency cash

flows

3. Decide what to do about the exchange raterelated operating exposure.

Simple example, revisited

• U.S. firm expects 10 mln SF/year from exports

to Switzerland, indefinitely.

• Assumptions:

– Competing with Swiss firms.

– SF price unaffected by $/SF fluctuations

• Consequently, $ revenues heavily affected by

$/SF changes:

10% SF depreciation lowers

discounted expected revenues 10%.

• SF appreciation has the opposite effect.

Example #2:

U.S. chemical firm exporting to Canada

• Major competition: other U.S. firms.

• Chemical industry sets C$ prices based on

U.S. $ costs.

• IF the Canadian dollar depreciates 10%:

– C$ prices rise overall by 10%.

– Reduction in total Canadian sales by 2%.

– Local currency result: C$ revenues up 8%.

– U.S. $ revenues for this firm fall 2%.

• Operating exposure not severe.

Price-setting firms with (some)

market power

• Some ability to raise local-currency prices in

foreign markets to offset FX depreciation.

• How much ability?

Depends on the price elasticity of demand for

that firm’s products.

Example: 1985-87 dollar

depreciation of 50% against DM

DM/DOLLAR EXCHANGE RATE, 1974-97

3.5

3

Plaza

DM/$

2.5

2

Louvre

1.5

1

74

76

78

80

82

84

86

88

90

92

94

96

Example: 1985-87 dollar

depreciation of 50% against DM

• Mercedes, BMW:

– Raise $ prices to (partly) maintain DM revenues?

– Leave $ prices unchanged to maintain market

share/sales volume?

• Policy:

– Raised $ prices 30-40%

– Intense advertising campaign to differentiate

German cars.

Managing Operating Exposure

• Financial management

– contractual hedges

• Strategic management

– marketing initiatives

– production initiatives

Financial Management of Operating Exposure

If have stable, predictable FC earnings,

various contractual/financial hedges are

feasible for the medium term (1-5 years)

• long-term forward contracts

• local-currency debt (matching)

• currency swaps

• long-term put options

Examples

• Merck (pharmaceuticals)

– R&D, production in U.S.

– Sales in U.S., abroad

• Sales predictable (niche-market)

• Local-currency prices often regulated abroad

• Kodak (film)

– Concerned w/ maintaining foreign market share

(against Fuji)

• Pioneer Hi-Bred

– Has foreign subsidiaries

Financial Management of Operating Exposure

Long-term forward contracts

• Waterford Crystal

– Costs in Irish punt

– Revenues in U.S. dollars

– Sold anticipated $ revenues forward out 2 years

• Difficult to hedge forward beyond 5 years

Financial Management of Operating Exposure

If have stable SF revenues

want to finance them with stable SF debt

so that only net SF revenues at risk.

Year

1

2

3

SF revenues

SF10 mln

SF10 mln

SF10 mln

...

SF interest

liabilities

-SF9 mln

-SF9 mln

-SF9 mln

...

SF1 mln

SF1 mln

SF1 mln

...

Net SF revenues

...

Example: Swiss subsidiary of U.S. firm

• If well-established, can directly issue SF debt

• If new, use a currency swap

– U.S. firm issues dollar debt

– U.S. firm swaps that debt for SF debt with a swap

dealer

Currency swap

1. U.S. firm issues $ debt

U.S. firm

$ liabilities

Currency swap

2. U.S. firm enters into a currency swap

U.S. firm

Pays SF

Receives $

$ liabilities

swap

dealer

Currency swap

$ revenues cover $ liabilities

U.S. firm

Pays SF

Receives $

$ liabilities

swap

dealer

Currency swap

Net effect: U.S. firm has effectively issued SF

debt to finance its foreign subsidiary

U.S. firm

Pays SF

Receives $

$ liabilities

swap

dealer

Strategic Management of

Operating Exposure

• In medium- to long-run, all firms have

exchange rate-related operating exposure.

Example:

“domestic” U.S. car company (Chrysler?)

– Costs in U.S. dollars

– Sales, revenues in U.S. dollars

• Yen depreciation makes Japanese cars more

competitive, reducing Chrysler’s revenues

• Real exchange rate movements affect the

overall competitive environment

– monitoring/measuring such effects important

– hedging can be difficult (and questionable)

• Firms respond strategically to exchange

rate-related problems and opportunities

– marketing initiatives

– production initiatives

Examples

• Goodyear-Mexico

– 37% Mexico peso devaluation 12/94

– Previously sold tires in Mexico

– Became major exporter to U.S., Europe, South

America

Examples

• U.S. textile industry

– U.S. cannot compete in labor-intensive textiles

– Major investment in capital-intensive textiles

niches

• Industrial fabrics

• Sheets, towels

– Increased service component

• Quick Reponse computerized inventory

management and ordering program for coordinating

textile mills/apparel manufacturers/retailers

Strategic Management of

Operating Exposure

Marketing Initiatives Production Initiatives

–

–

–

–

Market selection

Product Strategy

Pricing Strategy

Promotional Strategy

–

–

–

–

Product sourcing

Input mix

Plant location

Raising productivity

Marketing Initiatives

• Market selection & diversification

– Move into/out of various foreign markets,

depending on competitiveness

Example: Waterford Crystal (Irish)

When $ weakened in late 1980’s, went

increasingly after Asian, European markets.

Marketing Initiatives

• Product Strategy

– Altering product niche depending on

competitiveness

• New-product introduction

• Product line decisions

• Product innovation

• Example: Volkswagen (1970’s)

– 1960’s: low-priced cars with few features

– DM appreciation in early 1970’s, rising German

labor costs

– VW revised product line towards higher-priced

cars for middle-income consumers

Marketing Initiatives

• Pricing Strategy

– For firms with some market power: decision

between

• market share

• profit margins

when setting local-currency prices following a

currency appreciation/depreciation.

• Promotional Strategy

Example: Early 1980’s: strong $.

European countries advertised Alpine skiing

heavily in U.S.

Production Initiatives

• Changing Input Mix

– foreign outsourcing of component inputs

Example: Caterpillar. 50% of pistons are

foreign (Brazil)

• Shifting production among multiple

international plants

– Westinghouse: Plants in Canada, Spain, Britain

& Brazil.

– Toyota in 1994-6

• Creating new plants abroad

Example: Japanese, German car plants in U.S.

Production Initiatives

• Raising productivity

•

•

•

•

closing inefficient plants

automation

negotiating wage & benefit cutbacks

alternate production processes

Example: U.S. paper & pulp industries

(Brazilian competition)

Production and marketing initiatives have substantially

internationalized U.S. business over the last 15 years.

3.0

2.5

2.0

1.5

U.S. Direct Investment Abroad

($ trillion)

1.0

0.5

0.0

Foreign Direct Investment in U.S.

Summary

• Unexpected exchange rate fluctuations generally

affect the short-term and longer-term prospects of

the firm -- operating exposure

• There exist some financial tools for managing

identifiable operating exposure

• currency swaps, ...

• Firms typically respond strategically to exchange

rate-related shifts or potential shifts in relative

competitiveness

• Marketing initiatives

• Production initiatives

0

0