accounting for non profit organization

advertisement

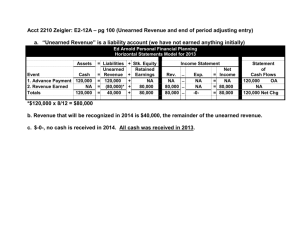

By : Wan Maimunah Wan Ishak Commerce Dept Tel : 09-5655300 ext 436 1. 2. 3. 4. At the end of this chapter, students should be able to : Understand the non profit organization Identify receipts and expenditure of NPO Understand special activities run by NPO Produce accounting records for NPO Club & Society Main purpose : to provide facilities to the members ( not profit making) Example : ?? Recommendation : Refer to some website of any club & society in Malaysia to have some overview of activities of any club & society Financial statement need to be presented in AGM Items of Financial Statement : 1. Revenue & Payment Account 2. Income & Expenditure Account 3. Balance Sheet Capital Revenue Income Revenue Membership Fee Contribution for special purposes Entrance Fee Small amount of donation Capital Expenses Fund of certain project Buying of Non Current Asset Income Expenses All expenses spent for that NPO Example : Transaction Revenue Capital Laundry Honorarium Interest on fixed deposit Gift Competition Fee Entrance Fee Utilities Maintenance Fee Purchase of furniture Premises Rent Donation for club fund Donation to build swimming pool Expenses Income Capital Income Example : Transaction Revenue Capital Donation Annual Fee Purchase of sport equipment Sales of old furniture Insurance Donation to grannies house Stamp Repair club premises Donation to build parking lot Salary of club’s clerk Lawyer fee to buy premise Dividend from investment Expenses Income Capital Income Receipts & Payment Account Particulars RM Particulars RM Bal b/f XX XX All receipts will be recorded here XX All payments will be recorded here Bal c/f XX Income & Expenditure Account Particulars RM Particulars RM All expenses will be recorded here XX All income will be recorded here XX Fee Account Jan 1 Unearned b/f xx Dec 31 Income & Expenditure xx Advanced c/f I&E – revenue item xx BS – current liability Jan 1 Advanced b/f Xx Dec 31 Receipts & Payment xx Unearned c/f xx BS – current asset 1. A club golf with 100 members charge the annual fee for RM50/member. The club received RM 4,200 as fees for the financial year ended 31 Dec 2009. That amount inclusive of RM 300 for 2010. Prepare Fees A/c 2. Balance as at 1 Jan 2009 : Unearned fees for 2008 RM 160 Advanced fees for 2009 RM 80 Extract from Cash Book as at 31 Dec 2009 : Cash Book Fees for 2008 RM 140 Fees for 2009 RM 4,400 Fees for 2010 RM 110 Additional info: Unearned fees for 2009 as at 31 Dec 2009 is RM 65 Balance for Unearned Fees for 2008 are write off . Prepare : Fees A/c, extract of P&L and extract of Balance Sheet 3. Extract from Cash Book as at 31 Dec 2009 : Cash Book Fees for 2008 Fees for 2009 Fees for 2010 RM 80 RM 4,850 RM 145 Additional info. : On 1 Jan 2009, unearned fees is RM 98. Unearned fees for 2008 are write off. There are Unearned Fees for 2009 for RM 68 as at 31 Dec 2009. Prepare : Fees A/c, extract of P&L and extract of Balance Sheet Enhance your understanding : Income & Expenditure A/c fye 31/3/ Rent 240 Profit from sales Printing & Stationery 150 Ticket sales Organizer’s expenses 160 Fee Maintenance 60 Whole life fee Salaries Misc Depre-equipment Surplus 520 55 180 3370 4735 315 2650 1600 170 4735 How did this figure derived ?? Balance Sheet as at ……….. Non Current Asset : Equipment 1100 -Accu. Depre (180) 920 Current Asset : Unearned fee Prepaid rent Cash Current Liab : Printing 400 60 3380 3840 (30) 3810 4730