Potential Predictors of Small Cap Stocks: Sharpe Ratio, Sortino

advertisement

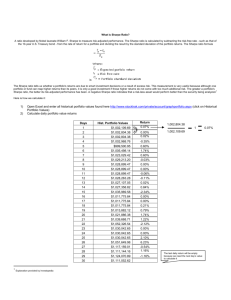

Potential Predictors of Small Cap Stocks: Sharpe Ratio, Sortino Ratio, Alpha Bethanie Royality-Lindman; Felicia Lin; Laura Meadows Abstract: One major debate surrounding the stock market is whether to follow active or passive trading. Passive investors believe that, according to the Law of One Price and the Efficient Market Hypothesis, there is no opportunity for making arbitrage profit and the best course of action is to create a portfolio that reflects the overall market to balance gains and losses and to have a chance at every successful stock. Active trading involves speculating stocks to see which will have the best performance as well as finding differences in prices of the same stock to make an arbitrage profit. Active investors have for many years been trying to find risk adjusted predictors of the stock market in order to gain the most profit. We choose Sharpe Ratio, Sortino Ratio, and Alpha after researching the most frequently used risk-adjusted measurements on various hedge-fund websites. Via linear regression, those three measurements are tested for their significance in determining and predicting the outcome of future full market cycles as risk-adjusted measurements. Introduction: In 1959 Harry Markowitz created a model to explore if mean and variance of return are good measures of an investor’s utility. Markowitz’s Mean-Variance Model suggests investors look to minimize variance of return and maximize return. Given this assumption, many mathematicians and money managers have tried to either predict the stock market as a whole (active managing) or explain why this is not possible (passive investing). William F. Sharpe argues for passive investing. Sharpe suggests that at any one point in time, the market return is the weighted average of returns on all the possible investments within the market. A passive investor by definition will have the same return as the market return, since a passive portfolio reflects the same securities in the certain market with the same proportions of investments that the whole market contains. Sharpe explains that an active investor must also have the same return as the market return, given that the entire market’s return is a weighted average of all securities, including those actively managed. Although individual active investors may do better than or worse than the market, on average active investors do as well as the market. Passive investing merely involves mimicking the market, but to invest actively one must put in time and effort to speculate on the market and choose the best investments, or pay someone to do this work. Since the return on active and passive investments must be exactly the same, and the cost of active management is higher than that of passive, an actively managed dollar is worth less than a passively managed dollar. With this, Sharpe concludes that passive investing provides greater profit than active investing. Sharpe created a ratio in order to try to predict the future of a stock’s success. This ratio is widely used and involves subtracting the risk-free rate of return over a certain period of time from the return on the investment being investigated, divided by the standard deviation of the stock’s return over time. The standard deviation is an attempt at measuring the volatility of the stock. upside volatility, or deviating from the mean return in a positive direction, is desired but is accounted for in Sharpe’s ratio. In an attempt to improve upon the Sharpe ratio, Dr. Frank Sortino created a ratio of his own, accounting only for the downside, and unwanted, volatility. Sortino works closely with retirement funds in most of his work. He argues that not every person has the same needs but that every investor obviously wants positive returns. Since it is not necessary to beat the market to gain, passive investing is a viable option for earning a profit while minimizing risk. Sortino believes in the looking carefully at downside capture, as shown in his ratio, when predicting the outcome of stocks. Sortino notes that CAPM and passive investing are limited but also explains that with current knowledge, they are the best options for minimizing risk and maximizing return. Two professors, mathematicians, and money managers that build off Sharpe’s work and argue for CAPM are Eugene F. Fama and Kenneth R. French. In their paper “The Capital ASset Pricing Model: Theory and Evidence” Fama and French explain the shortcomings of the version of CAPM that was created by Lintner and Sharpe. The two think that there is more that must be explored than just return, risk free return, and volatility to predict an investment’s outcome. Fama and French mention the need to look at groups of stock that are similar and size and type, or if the investment is a growth investment. Fama and French believe in the Law of One Price and in passive investing, but struggle, as do many others, to find the perfect predictor of an investment’s return. In our investigation we looked at 296 small cap funds over a full market cycle (about 7.5 years) to identify possible predictors of small cap investments’ future outcomes. Specifically, our research looked into the functionality of the Sharpe Ratio, Sortino Ratio, and alpha to predict the market. Sharpe Ratio Analysis: Sharpe Ratio is developed to measure risk-adjusted performance in any asset or portfolio. It is calculated by determining the return of a risk-free asset normally using United States Treasury Bills and subtracting that from the expected return of the asset or portfolio. That difference is then divided by the standard deviations of the asset’s or portfolio’s return. The Sharpe Ratio describes how much in “excess” return an investor is receiving for the extra risk/volatility that an investor beholds when investing in riskier assets or portfolio. Investors look to be compensated for investing in additional risk assets rather than for holding risk-free asset or portfolio like US Treasury Bills or Bonds. The Formula for Sharpe Ratio: Sharpe Ratio = 𝑅𝑅 −𝑅𝑅𝑅 𝑅𝑅 𝑅𝑅 = Expected asset return 𝑅𝑅𝑅 = Risk-free rate of return 𝜎𝑅 = Asset standard deviation The returns measured by this ratio have no defined time length as long as the assets or portfolio are normally distributed. Any abnormalities like skewed data or multi-modal on the distribution curve can be a problem. Asset standard deviation would potentially represent a weakness depending on the distribution. The risk-free rate of return is usually based on United States Treasury Bill. Investing with additional risk is usually compensated, so a risk-free rate of return is used to see if the investor is properly rewarded for taking that risk. While the risk-free asset and the investor’s target asset/portfolio should be equal in duration, it doesn’t necessarily have to be as long as both of the assets or portfolio can be annualized. Since the full market cycle is 7.5 years, a long-dated IPS (inflation protected security) would provide the best comparison for the investment, however that would result in different values for the ratio due to the length of the duration of the investment; IPS would have a higher return than United States Treasury Bills. Since the ratio is calculated with the intention of finding the “excess” return or rather compensation based on risk, the higher the ratio the better the investment for the investor is from a risk to reward perspective. The Sharpe Ratio is a risk adjusted measure of return that is used to evaluate the performance of an asset or of a portfolio. The ratio can be used to compare one portfolio with another portfolio by making a change to incorporate the risk difference. In the future, we will refer to First Market Cycle as FMC and Second Market Cycle as SMC. Descriptive Statistics: Standard Deviation FMC Variable Standard Deviation FMC N 295 N* 0 Variable Standard Deviation FMC Median 27.460 Mean 27.708 Maximum 55.910 SE Mean 0.180 StDev 3.095 Variance 9.579 Minimum 18.515 Regression Analysis: Cycle Growth% versus Full Market Cycle Sharpe The regression equation is Cycle Growth% = 19.2 - 21.4 Full Market Cycle Sharpe 246 cases used, 49 cases contain missing values Predictor Constant Full Market Cycle Alpha S = 41.9102 R-Sq = 0.6% Coef 19.15 -21.39 SE Coef 14.51 17.06 T 1.32 -1.25 P 0.188 0.211 VIF 1.000 R-Sq(adj) = 0.2% 𝑅0 :𝛽1 = 0 𝑅1 :𝛽1 ≠0 To analyze the relationship, we regress the Cycle Growth % between the first full market cycle and the second full market cycle against the calculated Sharpe Ratio of a full market cycle. We first check the standard deviation of the assets to ensure that the Sharpe Ratio is applicable; the histogram of the standard deviation shows normal curve. We determine a fitted line equation of Cycle Growth% = 19.2 - 21.4 Full Market Cycle Sharpe. From the R-Sq value of 0.6%, we can see that practically none of the variability in Cycle Growth% was associated with Full Market Cycle Sharpe. Also, given the resulting p-value of 0.211, we fail to reject the null hypothesis that the slope is equal to zero at the 0.05 level of significance. We conclude that there is insufficient evidence to conclude that there is a significant relationship between Full Market Cycle Sharpe and Cycle Growth%, and thus the full market Sharpe Ratio is not a significant variable in determining or predicting the outcome of full market cycles. Sortino Ratio Analysis: Investors’ usual approach to building a portfolio is by determining the amount of risk they are willing to take on then selecting the appropriate investment that is in their range of risk tolerance; in other words, the allocation of investment is driven by the amount of risk or “return” of investment they desire. The Sortino Ratio is the exact opposite of such an approach. This ratio focuses on the investors’ need for the amount of return on their investment not the amount of risk they wish to take on. Sortino Ratio unlike the Sharpe Ratio measures only the downside volatility. The calculation is similar to Sharpe except it uses the negative asset standard deviation for the denominator instead of the standard deviation of the desired assets or portfolio. The risk-free return of the asset is determined by the investor, for our situation it will be United States Treasury Bill to achieve conformity throughout the rest of the calculations. The Formula for Sortino Ratio: Sortino Ratio = 𝑅𝑅 −𝑅𝑅𝑅 𝑅𝑅 𝑅𝑅 = Expected asset return 𝑅𝑅𝑅 = Risk-free rate of return 𝜎𝑅 = Negative asset standard deviation This focus on the negative asset standard deviation makes the Sortino Ratio very relevant to investors because it looks at potential losses instead of simply the risk or volatility of an investment. The 𝑅𝑅𝑅 is also attractive due to the lack of limits on the parameter of what the benchmark can be. The benchmark usually is used to compare volatility against risk-free however it may not be every investor’s main objective. In regards to the Sortino Ratio, the investor has the freedom of choice in determining which benchmark aligns with the focus of making a bigger return on investment; thus the investor may choose a higher risk benchmark versus the regular United States Treasury Bill. Descriptive Statistics: Downside Standard Deviation FMC Variable Downside Standard Deviat N 295 N* 0 Variable Downside Standard Deviat Median 11.760 Mean 11.895 Maximum 24.770 SE Mean 0.0823 StDev 1.414 Variance 2.000 Minimum 8.370 Regression Analysis: Cycle Growth% versus Full Market Cycle Sortino The regression equation is Cycle Growth% = 22.7 - 14.4 Full Market Cycle Sortino 246 cases used, 49 cases contain missing values Predictor Constant Full Market Cycle Alpha S = 41.8564 R-Sq = 0.9% Coef 22.67 314.45 SE Coef 14.66 9.733 T 1.55 -1.48 P 0.123 0.139 VIF 1.000 R-Sq(adj) = 0.5% 𝑅0 :𝛽1 = 0 𝑅1 :𝛽1 ≠0 To analyze the relationship, we regress the Cycle Growth % between the first full market cycle and the second full market cycle against the calculated Sortino Ratio of a full market cycle. We first check the standard deviation of the negative assets to ensure that the Sortino Ratio is applicable; the histogram of the standard deviation shows normal curve. We determine a fitted line equation of Cycle Growth% = 22.7 - 14.4 Full Market Cycle Sortino. From the R-Sq value of 0.9%, we can see that practically none of the variability in Cycle Growth% was associated with Full Market Cycle Sortino. Also, given the resulting p-value of 0.139, we fail to reject the null hypothesis that the slope is equal to zero at the 0.05 level of significance. We conclude that there is insufficient evidence to conclude that there is a significant relationship between Full Market Cycle Sortino and Cycle Growth%, and thus the full market Sortino Ratio is not a significant variable in determining or predicting the outcome of full market cycles. Alpha Analysis: Alpha or the Jensen Index shares some resemblance to the CAPM (Capital Asset Pricing Model). While CAPM equation is used to calculate the required ROI (return of investment), CAPM is also used to evaluate the performance of various assets and portfolio. Alpha is used to figure out how much the realized return of the assets and portfolio from the expected market return as referenced in CAPM. The formula for Alpha is as follows: 𝛼 = 𝑅𝑅 − [(𝑅𝑅 − 𝑅𝑅𝑅 )𝑅] 𝑅𝑅 = Expected asset return 𝑅𝑅 = Expected market return 𝑅𝑅𝑅 = Risk-free rate of return Alpha is measures the premiums of risk in terms of β (beta); for our data we average out the 5 year β and 10 year β for the approximate of a full market cycle. It is assumed that the asset or portfolio being measured is varied. Alpha also requires different risk-free rate of return for each time interval to be measured. In this case the risk-free rate of return will be using T-Bill (United States Treasury Bill); since our full market cycle is calculated to be 7.5 years, we will be using an equivalent time duration for the T-Bill. We will examine the asset’s or portfolio’s returns minus the risk-free asset’s return and relate that to the return of the market portfolio minus the same risk-free asset’s return. Regression Analysis: Cycle Growth% versus Full Market Cycle Alpha The regression equation is Cycle Growth% = 0.76 - 44.6 Full Market Cycle Alpha 246 cases used, 49 cases contain missing values Predictor Constant Full Market Cycle Alpha S = 41.5219 R-Sq = 2.5% Coef 0.761 -44.62 SE Coef 2.655 17.94 T 0.29 -2.49 P 0.775 0.074 VIF 1.000 R-Sq(adj) = 2.1% 𝑅0 :𝛽1 = 0 𝑅1 :𝛽1 ≠0 To analyze the relationship, we regress the Cycle Growth % between the first full market cycle and the second full market cycle against the calculated Alpha of a full market cycle. We determine a fitted line equation of Cycle Growth% = 0.76 - 44.6 Full Market Cycle Alpha. From the R-Sq value of 2.5%, we can see that practically none of the variability in Cycle Growth% was associated with Full Market Cycle Alpha. Also, given the resulting p-value of 0.074, we fail to reject the null hypothesis that the slope is equal to zero at the 0.05 level of significance. We conclude that there is insufficient evidence to conclude that there is a significant relationship between Full Market Cycle Alpha and Cycle Growth%, and thus the full market Alpha is not a significant variable in determining or predicting the outcome of full market cycles. While alpha is a good measure of performance that uses realized return and risk-free return to calculate the risk on the investor, however calculation without further diversifying the asset and portfolio weakens the correlation that can be provided by alpha. Comparison of the Three Methods: The classic model for determining risk of a portfolio is the Sharpe ratio. Since the Sharpe ratio is often considered a base for comparison, I will begin by describing the Sharpe ratio, and then compare the Sortino and Alpha to the Sharpe ratio. The Sharpe ratio essentially tells us the origins of an investment's returns--either from excess risk, or carefully thought-out investment decisions. As mentioned earlier, the Sharpe ratio is calculated by subtracting the risk free rate from the average rate of return of the portfolio, and dividing it by the standard deviations of the return of the investment. Essentially, the Sharpe ratio is a measurement of how much return an investor is receiving, in exchange for the amount of risk that they are taking for a particular investment. A limitation of the Sharpe ratio is that it is expressed as a raw number. This means that having one fund’s Sharpe ratio is not meaningful, unless compared to another fund’s ratio. The Sharpe ratio will give an idea of the risk adjusted return in comparison to other funds, but will not be helpful on its own. The Sortino ratio can be described as a modification of the Sharpe ratio. The difference between the Sharpe and Sortino ratio is that Sortino takes into account “bad volatility” by separating the positive and negative returns. Negative returns on an investment is described as bad volatility, while good volatility is caused by positive returns and are desirable by investors. Mathematically, the Sortino ratio takes the portfolio’s return and subtracts the risk-free rate, and divides it by the downside deviation. The downside deviation is similar to standard deviation, except that instead of using the mean, it only considers returns that fell below a minimum acceptable return value. Therefore the difference between the Sharpe and Sortino ratios is that the Sortino ratio does not discriminate based on all volatility, only the “bad”, or what falls below a certain threshold. This threshold, or the minimum acceptable return value, is set by the investor based on his or her comfort level. Therefore the Sortino ratio gives a more personalized rating of an investment, based upon each individual investor. The Sortino ratio is most commonly used for those investors who are risk-averse. It allows investors to set their minimum acceptable return value and assess negative risk, as opposed to taking into account all volatility. Depending on whether the investor wants to concentrate on downside deviation or standard deviation, it can be difficult to say which ratio is more useful. Sortino ratio is often better for analyzing highly volatile portfolios because it takes into account downside deviation, and therefore does not need as many data points as standard deviation offers. On the other hand, the Sharpe ratio is best for analyzing portfolios with low volatility because it requires more data points, that standard deviation will give, while the downside deviation will not offer enough. The alpha value takes into account a portfolio’s beta. It is the the measurement of the actual return and expected return, taking its beta into consideration. In other words, it is the excess risk, taking into account the risk that the investor took. Beta measures volatility that cannot be eliminated through diversification. If an investment yields a higher return than what was expected given its beta, the value will be positive. One of the drawbacks of alpha in comparison to the Sortino and Sharpe ratio is that the value of beta must be meaningful. For instance, since the alpha ratio depends on beta, if the beta of a particular investment has an R-squared value that is too low, then alpha will not be meaningful. The Sharpe ratio does not have this limiting factor, and therefore will always be meaningful. The Sharpe ratio, which uses standard deviation, can be used to compare funds of varying types, since standard deviation is calculated using the same methods. However, since alpha uses beta, and can be calculated based on different benchmarks for stocks or bonds, it is not always useful when comparing the two. Sharpe does not have this problem and therefore can be used when comparing both stock and bond investments. Why is Sharpe Ratio the Standard?: The Sharpe ratio is one of the most commonly used ratios to measure risk of a portfolio. One reason is that it can be used to measure both stock and bond funds because it uses standard deviation. Since standard deviation is calculated using the same methods, it allows the measurements to be comparable. The Sharpe ratio is a simplified version of the Sortino ratio and does not distinguish between “good” and “bad” volatility. Whereas this creates obvious limitations, it keeps the ratio uniform and simple. It does not depend on the investor’s level of comfort or a particular minimum acceptable return value. The Sharpe ratio is intended to be used to measure diversified, liquid investments, and will give the most accurate measurement for investments that fall into this category. However hedge funds are not normally distributed, and is an example of why other ratios are more useful for determining risk. Although the Sharpe ratio has its drawbacks, perhaps the reason why it is the most widely used is due to its simplicity. It was developed in 1966 and won a nobel prize, which enhanced investor’s beliefs in its ability to assess risk. Many other ratios are based upon the Sharpe ratio, or are variations of the Sharpe ratio. This makes the Sharpe ratio an easy, common measurement from which to compare and base other determinants of risk. Although it is understood that it may not be the most useful in method of determining risk universally, it will always remain the simplest. Conclusion: Sharpe, Sortino, Fama, French and many other credible professionals have attempted to find the perfect formula for predicting return on a stock. Sharpe insisted that it is best to minimize cost when investing, which is most easily done through passive investing. Sortino brings to the table the idea that it is only necessary to look at downside volatility when looking at an investment’s future return, because upside capture is desirable so should not be considered when looking at a stock’s volatility. Fama and French explore the many ratios and possible predictors of securities. In our research, we explored small cap stocks and their performances in a complete market cycle of about seven years. In an attempt to find the most accurate predictor of return, we looked at the Sharpe Ratio, the Sortino Ratio, and alpha and compared their predictions to the actual return on these investments. Below is the two-sample T-Test for the Sharpe ratio of the FMC against the SMC and the Sortino ratio of the FMC against the SMC. The resulting p-value of 0 for both tests shows that we must reject the null hypothesis that states that the difference between the average of the Sharpe ratio of the FMC and the SMC is 0. Therefore, the difference is significant. The FMC is different from the SMC in both cases, indicating that both the Sharpe ratio and Sortino ratio are incapable of predicting such large differences and therefore would not be good predictors of any market cycle. Two-Sample T-Test and CI: Sharpe FMC, Sharpe SMC Two-sample T for Sharpe FMC vs Sharpe SMC N Mean StDev SE Mean Sharpe FMC 295 1.564 0.966 0.056 Sharpe SMC 295 0.931 0.240 0.014 Difference = mu (Sharpe FMC) - mu (Sharpe SMC) Estimate for difference: 0.6333 95% CI for difference: (0.5194, 0.7471) T-Test of difference = 0 (vs not =): T-Value = 10.93 Both use Pooled StDev = 0.7039 P-Value = 0.000 DF = 588 Two-Sample T-Test and CI: Sortino FMC, Sortino SMC Two-sample T for Sortino FMC vs Sortino SMC N Mean StDev SE Mean Sortino FMC 295 1.061 0.616 0.036 Sortino SMC 295 0.3503 0.0935 0.0054 Difference = mu (Sortino FMC) - mu (Sortino SMC) Estimate for difference: 0.7104 95% CI for difference: (0.6391, 0.7816) T-Test of difference = 0 (vs not =): T-Value = 19.59 Both use Pooled StDev = 0.4404 P-Value = 0.000 DF = 588 Regression Analysis: Sharpe FMC versus Sharpe SMC Analysis of Variance Source DF Regression 1 Sharpe SMC 1 Error 293 Total 294 Adj SS Adj MS 6.666 6.6655 6.666 6.6655 267.698 0.9136 274.363 F-Value P-Value 7.30 0.007 7.30 0.007 Model Summary S 0.955848 R-sq 2.43% R-sq(adj) 2.10% R-sq(pred) 0.51% Coefficients Term Constant Sharpe SMC Coef 0.981 0.626 Regression Equation SE Coef T-Value P-Value VIF 0.223 4.40 0.000 0.232 2.70 0.007 1.00 Sharpe FMC = 0.981 + 0.626 Sharpe SMC The graph above shows the regression of the Sortino FMC versus the Sortino SMC. After running the regression of the Sortino FMC to the SMC, we found a non-existent, or weak correlation. The r^2 was only .0216, meaning that only 2.16% of the variation in the Sortino FMC can be explained by the Sortino SMC. Therefore, the correlation is not significant to conclude a linear relationship between the two. Regression Analysis: Sortino FMC versus Sortino SMC Analysis of Variance Source DF Adj SS Adj MS F-Value P-Value Regression 1 2.407 2.4074 6.47 0.012 Sortino SMC 1 2.407 2.4074 6.47 0.012 Error 293 109.091 0.3723 Total 294 111.499 Model Summary S 0.610185 R-sq 2.16% R-sq(adj) 1.83% R-sq(pred) 0.00% Coefficients Term Constant Sortino SMC Coef 0.722 0.968 SE Coef T-Value P-Value 0.138 5.23 0.000 0.381 2.54 0.012 1.00 VIF Regression Equation Sortino FMC = 0.722 + 0.968 Sortino SMC Looking at the scatterplots of “Cycle Growth% Versus Full Market Cycle Sharpe” and “Cycle Growth% Versus Full Market Cycle Sortino”, we investigated both ratios’ effectiveness on predicting the full market cycle. We calculated the growth % between full market cycles and regressed it as a response to the factor of Sharpe Ratio and Sortino Ratio. The resulting coefficient of determination, R-sq, is 0.6% and 0.9% respectively. A mere 0.6% and 0.9% of the variability in stock returns can be associated with a change in Sharpe Ratio and Sortino Ratio. The resulting p-value is 0.211 and 0.139 which leads us to fail to reject the null hypothesis of 𝑅0 :𝛽1 = 0. This suggests that Sharpe Ratio and Sortino Ratio plays no part in predicting the return of the full portfolio over the duration of a full market cycle. Therefore, if given any Sharpe or Sortino ratio for a small cap stock, it would not be possible to predict the future value after a full market cycle of the asset or portfolio. Additionally, the graph below shows the regression line of the Sharpe ratio versus the Sortino ratio. We regressed the Sharpe ratios against the Sortino ratios and found a strong, positive, linear relationship between the two with an r^2 of 96.3. This means that 96.3% of the variability in Sharpe can be described by the Sortino ratio. Therefore, both ratios are equally poor predictors of the performance of small cap stocks. Lastly, we investigated alpha’s effectiveness on predicting the full market cycle. We were able to plot individual alphas for each stock we investigated against the return of each investment over a duration of 7.5 years, the length of a full market cycle. The resulting coefficient of determination, R^2, is 2.5%. A mere 2.5% of the variability in stock returns can be associated with a change in alpha. The resulting p-value is 0.074 which leads us to fail to reject the null hypothesis of 𝑅0 :𝛽1 = 0. This suggests that alpha plays no part in predicting the return of the full portfolio over the duration of a full market cycle. In the future, our investigation could be improved upon by adding a variable that includes a measure of value and/or growth of each stock. Past research has shown that it may be important to divide the stocks into sections, grouped by similarities of the style of the stocks, in terms of their ability to add value or growth to a portfolio. Based on the definitions of growth and value stocks, these types of investments perform differently. Therefore, separating these types of stocks and then testing our methods on the new groupings may provide evidence that alpha, the Sharpe ratio, or the Sortino ratio are capable of predicting future performance of certain types of securities. Works Cited "EVestment Guide To Investment Statistics." Investing Classroom. Evestment, 1 Jan. 2014. Web. 1 Nov. 2014. <https://www.evestment.com/resources/investment-statistics-guide/downsidedeviation>. Fama, Eugene F., and Kenneth R. French. "The Capital Asset Pricing Model: Theory and Evidence." Journal of Economic Perspectives 18.3 (2004): 25-46. Web. 16 Nov. 2014. Koba, Mark. "Alpha and Beta." CNBC Explains. NBC Universal, 19 Jan. 2012. Web. 1 Nov. 2014. <http://www.cnbc.com/id/45777498#.>. Sharpe, William F. "The Arithmetic of Active Management." Financial Analysts Journal 47.1 (1991): 7-9. Web. 16 Nov. 2014. Sortino, Frank, Mark Kordonsky, and Hal Forsey. "Managing by Facts." Pensions & Investments. Pensions and Investments, 19 Feb. 2007. Web. 16 Nov. 2014. "Sortino Ratio." Investopedia Inc. Tradimo Ltd., 1 Jan. 2014. Web. 1 Nov. 2014. <https://www.evestment.com/resources/investment-statisticsguide/downside-deviation>. Wiley, John. "Gauging Risk and Return Together,." Investing Classroom. Morningstar, 1 Jan. 2010. Web. 1 Nov. 2014. <http://news.morningstar.com/classroom2/course.asp?docId=2932&page=2&CN=com>.