Analyzing Transactions Presentation

advertisement

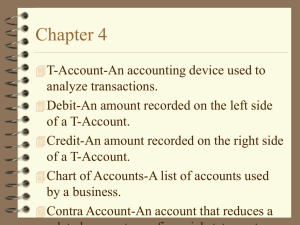

Analyzing Transactions into Debit and Credit Parts PRINCIPLES OF ACCOUNTING I Objectives • By the end of the lesson, I will be able to: • define accounting terms related to analyzing transactions into debit and credit parts. • identify accounting practices related to analyzing transactions into debit and credit parts. • use “T” accounts to analyze transactions showing which accounts are debited or credited for each transaction. • verify the equality of debits and credits for each transaction. What We Know • We have learned how business transactions affect accounts in an accounting equation. • Procedure is not practical in an actual accounting system. • the number of accounts most businesses have would make the accounting equation cumbersome to use • a separate record is commonly used for each account Accounting Terms • Accounting equation: shows relationship among assets, liabilities, and owner’s equity • Asset: anything of value that is owned or controlled • Capital: account used to summarize the owner’s equity • Chart of accounts: list of accounts used in a business • Credit: amount recorded on the right side of a T-account • Debit: amount recorded on the left side of a T-account • Liability: amount of money owed to the creditors of a business • Normal balance: side of the account that is increased • Owner’s equity: amount remaining after the value of all liabilities is subtracted from the value of all assets • T-account: accounting device used to analyze transactions • Transaction: business activity that changes assets, liabilities, or owner’s equity The Accounting Equation Assets = Liabilities + Owner’s Equity • The accounting equation can be represented as a “T”: • Always draw T accounts when analyzing transactions to see the debit and credit sides. What Does a T Account Look Like? Location, location, location • The normal balance side of an asset, liability, or capital account is based on the location of the account in the accounting equation All about the sides…. • The sides of the T account also show increases and decreases in account balances Rules • Two basic accounting rules regulate the increases and decreases of account balances: • Account balances increase on the normal side of an account • Account balances decrease on the opposite side of an account Remember This… • Asset accounts have normal debit balances • increase on the debit side • decrease on the credit side • Liability accounts have normal credit balances • increase on the credit side • decrease on the debit side • Owner’s equity account has a normal credit balance • increases on the credit side • decreases on the debit side Let’s Review • The normal balance side of an asset, liability, or capital account is based on what? • The sides of the T account show what? • Assets account have normal __________ balances. • Liability accounts have normal __________balances. • Owner’s Equity accounts have normal __________balances. Analyze This…. • Before a transaction is recorded in the records of a business, the information is analyzed to determine which accounts are changed and how. • Each transaction changes the balances of at least two accounts and debits equal credits for each transaction. • Four steps are used in analyzing a transaction: • Determine what accounts will be affected • Determine whether to increase or decrease the account • Determine whether the increase/decrease needs to be a debit or a credit • Make sure debits equal credits Let’s Do This Together • Using the Graphic Organizer, we will analyze the following transactions: • Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service. • Maria Sanchez transferred two telephones valued at $200 each from her home to the business. • Roadrunner bought a used truck on account from North Shore Auto for $12,000. • Roadrunner sold one telephone to Green Company for $200 on account. On Your Own…. • Using Microsoft Excel, you will create T accounts and basic formulas to analyze the transactions on your John Jones Computing handout. Ticket Out of the Door • List the normal balances Assets, Liabilities, and Owner’s Equity