Credit PP - Westmoreland Central School

advertisement

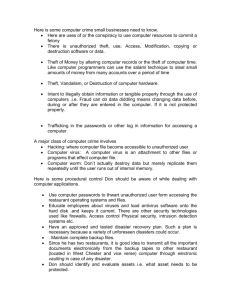

Lesson 6 Obtaining and Protecting Your Credit Learning Objectives • Explain the concept of consumer credit, including major types and its benefits and drawbacks • Describe the keys to building and maintaining healthy credit • Identify ways to protect your identity 2 The Basics of Credit for Consumers • You will almost certainly need or want to use credit at some point in your life • Used properly, credit can make it possible to purchase things that might be difficult to save the entire amount for • Used unwisely, credit can wreak havoc in your financial life!!!!!! 3 Types of Credit • It is essential to know about: – the major types of credit – the advantages and disadvantages of each – the laws that protect your right to get credit • Credit for consumers fall into one of three categories: – Noninstallment – Installment – Revolving open-end credit 4 Types of Credit • The consumer borrows the money at • NONINSTALLMENT the time of purchase is credit that is extended for a short term, such • Then the consumer pays off the entire amount within a short time as 30 days or less • Noninstallment credit is typically issued by: – department stores – furniture stores – other businesses selling items that cost several hundred dollars 5 Types of Credit • Noninstallment credit encourages immediate purchases of specific items • This type of credit may be useful to a person who is expecting to receive money soon enough to repay the amount borrowed 6 Types of Credit • Installment credit is also used for specific purchases but allows the borrower more time to repay the money • Principal is the total amount of money outstanding on the loan • Installment loans typically require the borrower to make monthly payments • Part of each payment goes to reduce the principal • Monthly payments also include interest charges 7 Types of Credit • Installment loans may span a few years • These type of loans are generally used for purchases such as furniture, boats, and other large items • Note that using installment credit does make the purchase of these items more costly • Take a look at Figure 9.1 to see how much interest you might pay over the life of a typical loan 8 Figure 9.1 9 Types of Credit • Revolving open-end credit allows consumers to borrow up to some preset maximum amount, such as $1,000 or $10,000 • Credit limit the preset maximum amount you can borrow • Consumers can use revolving credit to make one purchase or many • They can repay the entire amount borrowed at the end of the month • They can also spread payments over a longer time • They can continue to use the credit as long as they do not exceed their credit limit 10 Math for Personal Finance • Barbara borrowed $2,300 to buy some furniture and is paying 15 percent interest a year for the loan. The terms of the loan do not require her to pay off any of the loan balance during the first year. She only has to make interest payments. • How much interest will she pay the first year if she does no reduce the principal of the loan? 11 Math for Personal Finance • Solution: Barbara will pay $2300 x .15 = $345 in interest the first year 12 Advantages of Using Credit • Credit history is the record of how one has used credit in the past • Credit helps you make large purchases sooner • Using credit simplifies your finances by eliminating the need to carry cash or checks • Using credit wisely can help you establish a good credit history • A good credit history can make it less expensive for you to use credit in the future 13 Math for Personal Finance • Harlan used his credit card—a form of short-term credit—to charge three tanks of gas this month. • If his charges were $43.12, $51.87, and $38.35, how much should he pay at he end of the month? 14 Math for Personal Finance • Harlan should pay the bill in full: $43.12 + $51.87 + $38.35 = $133.34 15 Disadvantages of Using Credit • It is often easier to get credit than it is to pay it back • If you borrow too much money, you may have difficulty making the payments • A bad history can make borrowing more costly—or impossible • Failure to pay off loans can lead to bankruptcy 16 Disadvantages of Using Credit • Credit cards can tempt us to purchase things today when it would be wiser to save and pay for in full • Credit card interest rates are usually very high • It is wise to use credit cards for purchases you plan to pay off when the bill comes in • Check out www.chase.com for a payment calculator where you can plug in different balances and interest rates 17 Math for Personal Finance • Sabrina charges $800 at the local sporting goods store to buy some exercise equipment. The store offers no interest for 90 days if the balance is paid in full, or 24 percent annually if the balance is not paid in full prior to 90 days. • How much interest will she need to pay if she lets the account go for 91 days before paying the bill? 18 Math for Personal Finance • Solution: She will pay 2 percent--.02 a month, since the annual rate is 24 percent. At 91 days, she will owe for three months-3 x .02. Therefore, her interest will be $800 x .06 = $48 19 Credit Rights and Consumer Credit Laws • Equal Credit Opportunity Act prohibits creditors— people who provide credit—from denying credit based on gender, age, race, national origin, religion, and martial status • Federal law helps protect your access to credit • This legislation requires creditors to notify applicants within 30 days if they will receive credit • They explain the reason for denial if credit is denied • Refer to figure 9.2 for other consumer credit laws 20 Figure 9.2 21 Check Your Financial IQ • What are the risks and benefits of consumer credit? 22 Check Your Financial IQ • Credit is convenient and can make certain purchases possible. • But credit is costly and can lead to financial problems if used unwisely 23 Building Good Credit • We all want to establish good credit • Having no credit history at all may result in paying more for credit risk (how do they know if you have not history to compare) • Lenders often charge higher interest rates for people with less-than-good credit • Know the process by which you build good credit and how that information is collected and reported to creditors 24 Your Credit History • Each person’s credit history is collected in an individual credit report • How many times have you borrowed money? Did you pay it back on time? • Lenders use this information every time you apply for credit • Every time you make a credit purchase, it will further establish your credit history, good or bad. 25 Your Credit History • Paying for utilities, such as electricity and phone, also shows up on your credit history • Failing to pay your utility bills will negatively affect your credit history • It can also affect your ability to get credit in the future 26 Credit Bureaus and Credit Scoring • Credit bureaus collect credit information on individual consumers • There are three main credit three main credit bureaus: – Equifax – Experian – TransUnion 27 Credit Bureaus and Credit Scoring • Credit report shows every time you have applied for credit, whether or not you have paid your bills on time, if you have paid your credit cards in full every month or carried a balance, and if you have paid late fees • Credit bureaus provide credit reports to potential lenders, employers, and others upon request • Everyone can access his or her credit report once every 12 months free of charge • You will see the types of records being maintained by these credit bureaus regarding your personal credit history 28 Credit Reports • Fair Credit Reporting Act limits the sharing of your financial information only to firms that have a legal purpose to evaluate this information • When you apply for credit, the potential creditor will study your report and make decisions about extending additional credit • Review your credit report now and make sure it contains accurate information • Companies can make mistakes that can hurt your financial life 29 Credit Score • Credit score a number based on your credit history that assesses your creditworthiness • Credit bureaus use your credit history to create a credit score • Individuals with higher credit scores get better interest rates on loans • They are determined to have a lower risk of defaulting 30 Credit Score • Credit scores are calculated based on a model created by • Fair Isaac Corporation (FICO) • Credit scores are often called FICO scores • FICO scores will be between 300 and 850 • A higher score indicates better credit • Look at figure 9.4 to see where most people’s credit scores fall 31 Figure 9.4 32 Credit Score • FICO scores are broken down the following way: – 35 percent based on your credit history – 30 percent based on how much of your available credit you are using 33 Check Your Financial IQ • What are the elements of “good credit”? 34 Check Your Financial IQ • Good credit means having a credit history that is generally free of credit problems, such as unpaid or late bills 37 Threats to Your Credit: Identity Theft • Identity theft occurs when someone uses your personal information without your permission for personal gain • Identity theft can occur without you even knowing it • Someone may use your personal information to open a credit account and buy a large purchase • This account will be reported to the credit bureau under your name • When they don’t pay the bill your credit score will suffer 36 Threats to Your Credit: Identity Theft • Some criminals use your personal information to establish totally new identities and engage in criminal activity • People who have had their credit destroyed can no longer borrow money for anything • Identity theft is illegal but is difficult to detect 37 Identity Theft Tactics • Shoulder surfing occurs when someone in a public place skims personal information to use against you by overhearing your conversation or viewing your personal information • Identity thieves use a variety of tactics • Be cautious when someone seems to be standing too close to you when you’re using a computer, using a credit card, etc. 38 Identity Theft Tactics • Identity thieves have been known to go through a person’s trash to gather information • Credit card receipts, banking information, or unsolicited offers for credit cards can enable someone to profit from your identity • Shred documents such as these prior to disposing of them 39 Identity Theft Tactics • Other tactics include: – Skimming involves copying your credit card or debit card numbers from your cards – Pretexting occurs when someone improperly accesses your personal information by posing as someone who needs data for one reason or another – Phishing is when pretexting occurs online and can include emailing you and asking you to verify account information – Pharming uses email viruses to redirect you from a legitimate website to an official looking website designed to obtain your personal information 40 Protecting against and Reacting to Identity Theft • Preventing the theft of your identity is well worth the simple investment • The purchase of identity theft insurance may also be worth considering • Refer to figure 9.6 for some methods you should employ to prevent identity theft. 41 Figure 9.6 42 Protecting against and Reacting to Identity Theft • Act quickly if you detect a sign of identity theft • Monitor your credit report and protect yourself from identity theft • It is critical to your long-term financial health 43 Monitor Your Credit Report • Check your credit report periodically • Report inaccurate information to the three main credit reporting bureaus • File a dispute related to the inaccurate information • The credit bureaus will contact the creditor to verify the accuracy of information and change it if inaccurate 44 Check Your Financial IQ • What is identity theft? 45 Check Your Financial IQ • It is the improper use of personal information for gain 49 Summary • Credit is the ability to borrow funds that will be repaid in the future • It comes in a number of different forms such as: – Noninstallment – Installment – Revolving open-end credit 47 Summary • Credit has advantages and disadvantages • An advantage to credit is that it helps make large purchases easier • A disadvantage is that credit can be costly • Building good credit history is important to your financial future 48 Summary • Credit bureaus maintain a complete history of your credit transactions • They determine your credit score and report this information to interested parties • You can obtain a free credit report from any one of the three credit bureaus to ensure that the report is accurate 49 Summary • Identity theft is one of the fastest growing crimes in our country • It is important to protect yourself against identity theft • Act quickly if you suspect identity theft • Keep copies of all correspondence and credit transactions 50 Key Terms and Vocabulary • • • • • • • • • • • Credit Credit bureau Credit history Credit limit Credit report Credit score Creditor Equal Credit Opportunity Act Fair Credit Reporting Act Fair Isaac Corporation Identity theft • • • • • • • • • • Installment credit Interest Noninstallment credit Pharming Phishing Pretexting Principal Revolving open-end credit Shoulder surfing Skimming 51 Websites • www.chase.com • www.myfico.com • www.myfico.com/CreditEducation/Improve YourScore.aspx • www.annualcreditreport.com • www.ftc.gov • www.privacyrights.org 52