Committee to Study

Washington State’s Tax Structure

(ESSB 6153, Section 138)

“... to determine how well the current tax

system functions and how it might be changed

to better serve the citizens of the state in the

21st Century.”

Due November 30, 2002

Committee Appointments

Governor appointment

• William Gates, Sr.

Caucus appointments

•

•

•

•

Sen. Lisa Brown

Gary Strannigan

Rep. Jim McIntire

Rep. Jack Cairnes

Academic appointments

;;

• John

Beck

Gonzaga University School of Business Administration

• Neil Bruce

University of Washington Economics Department

• Dick Conway

Consultant, Governor’s Council of Economic Advisors

• Lily Kahng

Seattle University School of Law

• Debra Sanders

Washington State University School of Accounting

• Hugh Spitzer

Attorney, University of Washington

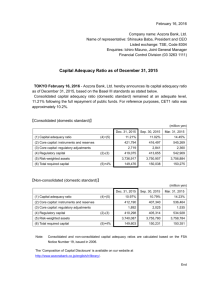

Problems with our current tax structure

Regressivity

Percent of Income Paid in Tax

Lower income households pay a higher percentage of their

income in state and local taxes than do higher income

households.

16%

14%

Total Excise and Property

12%

Property Tax

10%

Excise Tax

8%

6%

4%

2%

0%

Up to

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

Household Income

Source: Washington Excise and Property Tax Microsimulation Model

$100,000 $130,000

over

$130,000

Problems with our current tax structure

Exportability

State and local taxes are more burdensome because the retail

sales tax paid by households is not deductible from federal

income taxes.

Problems with our current tax structure

Adequacy

It is politically difficult to build and maintain adequate reserve

funds during good economic times.

Initiatives have impacted long run adequacy.

Initiatives and state-imposed reductions in tax bases have

impacted local adequacy.

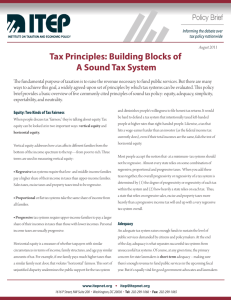

Problems with our current tax structure - Adequacy

Percent of

1971 value

1300

Excluding tax base and rate changes, over the past 30 years

General Fund revenues have grown more slowly than the

economy (personal income).

1100

900

700

The Economy

Revenues

(excluding tax base and rate

changes)

(Personal Income)

500

300

100

1971

1973

1975

1977

Source: Office of Financial Management

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

Problems with our current tax structure

Volatility

Washington’s mix of taxes causes revenues to increase more than

personal income during good economic times and less than

personal income in economic downturns.

Growth Rates

Sales Tax is more volatile than the

economy (personal income).

Personal Income

Retail Sales Tax

Inflation and other trends have been eliminated. Growth rates are due only to volatility .

Problems with our current tax structure

Erosion of the Tax Base

The increasing share of services in consumer spending, along

with increased opportunities for making purchases out of state,

result in taxable retail sales growing more slowly than the

economy as a whole over the long run.

Individuals can avoid sales tax by shopping in bordering states

with lower sales tax rates or by making remote purchases.

Problems with our current tax structure

B&O taxes are not neutral

Some Washington firms are able to avoid the B&O tax by shifting

their income generating activities (such as manufacturing) to

other states.

B&O tax pyramiding (at least 2:1) results in non-neutralities

between different industries and between vertically integrated

and non-integrated firms

Problems with our current tax structure

Business taxes are “hidden”

To the extent that business taxes are passed on to consumers,

business taxes are not transparent.

Menu of Major Alternatives

Problems Addressed

Neutrality

Business Value Added Tax (VAT)

Goods and Services Tax (GST)

Neutrality,

Transparency, Erosion

Neutrality, Transparency

“Progressive” VAT (low-income relief)

Regressivity

Flat Rate Personal Income Tax

Regressivity

Graduated Personal Income Tax

Regressivity

Flat Personal and Corporate Income Tax

Regressivity

Representative Packages

Value Added Tax Alternatives

Existing Taxes Reduced

or Replaced

#1

Business

VAT

Revenue Neutral

VAT Tax Rate

Replace B&O tax

2.2%

#2 Goods &

Services Tax

Replace sales/use and

B&O taxes

9.0%

#3

Reduce sales/use tax

from 6.5% to 3.5%

Replace B&O tax

3.9%

Progressive

VAT

#1 Subtraction Method VAT at 2.2%

Replaces B&O

NO CHANGE IN REGRESSIVITY

Percent of Income paid

in Tax

20%

Initial Tax Burden on Households

Major State and Local Taxes

15%

10%

Current Law

5%

Replace B&O

0%

Up to

$30,000

$40,000

$50,000

$60,000

$70,000 $80,000 $100,000 $130,000

$20,000

Household Income

Source: Washington Excise and Property Tax Microsimulation Model

Over

$130,000

#2 Goods and Services Tax

Percent of Income paid in Tax

20%

Initial Tax Burden on Households

Major State and Local Taxes

15%

10%

Current Tax System

5%

Replace RST and B&O

0%

Up to

$30,000

$40,000

$50,000

$60,000

$70,000 $80,000 $100,000 $130,000

$20,000

Household Income

Over

$130,000

#3 “Progressive” VAT

Percent of Income paid in Tax

20%

Initial Tax Burden on Households

Major State and Local Taxes

15%

Current Law

Replace B&O & Reduce RST

10%

5%

0%

Up to

$30,000

$40,000

$50,000

$60,000

$70,000 $80,000 $100,000 $130,000

$20,000

Household Income

Over

$130,000

Percent Reliance on Major State and Local Taxes

#2 Goods and Services Tax

0%

20%

40%

60%

80%

Current Tax

System

49%

13%

30%

Alternative Tax

System

49%

13%

30%

U.S. Average

25%

General Sales Taxes

11%

29%

Selective Sales Taxes

100%

27%

Property

Income

Percent Reliance on Major State and Local Taxes

#3 “Progressive” VAT

0%

20%

Current Tax

System

49%

Alternative Tax

System

U.S. Average

40%

43%

25%

11%

60%

80%

13%

13%

100%

30%

30%

29%

6%

27%

General Sales Taxes

Selective Sales Taxes

Property

Income

#4 Flat Rate Personal Income Taxes

Existing Taxes Reduced or Replaced

A Reduce state sales/use tax from

6.5% to 3.5%

Revenue Neutral

Income Tax Rate

2.6%

B

Reduce state/use sale tax to 3.5%

and replace state property tax

3.8%

C

Replace state sales/use tax

5.5%

D

Replace state sales/use tax and

state property tax

6.7%

#5 Graduated Personal Income Taxes

Revenue Neutral Rates for Joint Returns

Existing Taxes Reduced or

Replaced

$0 to

49,900

$49,900 to

120,650

$120,650

and over

A

Reduce state sales/use tax

from 6.5% to 3.5%

1.0%

2.7%

4.5%

B

Reduce state sales/use tax

from 6.5% to 3.5% and

replace state property tax

2.2%

3.5%

6.0%

C

Eliminate state sales/use tax

2.7%

5.7%

8.7%

Note: The income break points for single filers are $0 to 24,950, up to $60,325 and over $60,325.

#4 Flat Rate Personal Income Taxes

16%

Initial Tax Burden on Households

Percent of Income paid in Tax

14%

Major State and Local Taxes

12%

10%

8%

6%

Current Tax System

Sales Tax at 3.5% and Replace Property Tax

4%

Replace Sales Tax

2%

Replace Sales and Property Taxes

0%

Up to

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

Household Income

$80,000

$100,000 $130,000

Over

$130,000

#5 Graduated Rate Personal Income Taxes

16%

Initial Tax Burden on Households

Tax Paid as a Percent of Income

14%

Major State and Local Taxes

12%

10%

8%

6%

Current Law Tax System

4%

Sales Tax at 3.5%

Sales Tax Replaced by Personal Income Tax

2%

Sales and Property Tax Replaced by Personal Income Tax

0%

Up to

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

Household Income

$80,000

$100,000

$130,000

Over

$130,000

Percent Reliance on Major State and Local Taxes

#4 and #5 Flat and Graduated Income Taxes

53%

WA TAX SYSTEM

39%

Sales Tax at 3.5%

14%

27%

U.S. AVERAGE

Replace Sales

and Prop Tax

OREGON

14%

21%

21%

11%

0%

General Sales Taxes

12%

14%

33%

14%

32%

30%

25%

39%

34%

20%

33%

54%

40%

Selective Sales Taxes

60%

Property

80%

100%

Income Taxes

Long Term Adequacy

Personal Income Tax v. Sales Tax

450%

Flat Rate Personal Income Tax at 5.5%

400%

350%

Personal Income (Economy)

300%

250%

200%

150%

00

20

99

19

98

19

97

19

96

19

95

19

94

19

93

19

92

19

91

19

90

19

89

19

88

19

87

19

86

19

85

19

84

19

83

19

82

19

81

19

80

100%

19

Growth Percent

Sales Tax (Constant Base & Rate)

Improvements to the Current System

Continue to impose an estate tax.

• Tax in the amounts of the state credit allowed under

prior federal law.

• Adequacy - Prevents an increase in regressivity by

maintaining an existing tax on high-income

households.

• No change. Current yield estimated at:

FY 2005

$114.8 million

Extend the sales tax to consumer services.

Adds beauty shops, amusement, recreation and cable

TV to definition of retail sale.

Adequacy - extends the base to a growing area of

consumption not subject to tax.

• Equity - resolves inequities in our tax system, e.g.,

video rentals are taxed and movie tickets are not.

• Estimated revenue gain:

CY 2005

$229.6 million

Join other states in enacting streamlined sales

tax legislation.

• Multistate effort to create simpler, more uniform system for

collection of sales tax.

• Erosion of the base, equity - leads to collection of retail

sales tax on remote sales.

• Neutrality - consumers could no longer avoid tax by

shopping on the Internet.

• Economic vitality - would improve the competitive position

of WA retailers.

• Simplicity - uniformity would make sales tax simpler for

multi-state retailers.

Extend the watercraft tax to motor homes and

travel trailers.

• Consider raising existing rate from 0.5% rate to 1%.

• Equity - motor homes and travel trailers can be

substitutes for vacation homes which are taxed.

• Regressivity - upper income households spend more

on motors homes/travel trailers as a percent of

income.

• Estimated revenue gain:

1% Rate = $47.5 million in CY 2005

Create a constitutionally mandated “rainy day”

fund.

• Enact a constitutional amendment mandating a

“rainy day” fund.

• Volatility - sets aside revenues in years when they

exceed income growth.

• Adequacy - would help prevent permanent

decreases in the tax base during good economic

years.

Exempt construction labor from sales tax.

• Only a few states impose a sales tax on labor portion

of construction.

• Exempt labor portion of construction contract.

• Problems addressed:

Economic Vitality

Tax Harmony

Simplicity

Volatility

Regressivity

Homeownership

• Estimated revenue loss:

CY 2005

$400 million

Increase the B&O small business credit from

$35 to $70 a month.

• Increase the small business credit to $70/month.

• Raise the reporting threshold from $28,000 to $56,000

in gross.

• Economic vitality - new and expanding firms have

high tax burdens. This improvement would assist

new and expanding businesses that start out small.

• Estimated revenue loss:

CY 2005

$28 million

Other improvements to current system

Problem Addressed

Simplify local B&O tax

Avoid or reduce dedicated taxes

(except user fees)

Periodically review tax incentives to

determine if they’ve outlived their

purpose.

Neutrality, economic

vitality

Simplicity

Adequacy, economic

vitality

0

0