Chapter 13A

Budgeting

Budgeting

A budget is a financial plan for a

business.

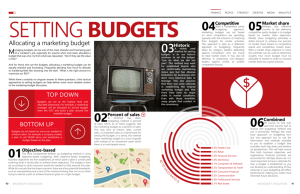

Objectives of budgeting:

• Establishing specific goals (Planning)

• Executing plans to achieve the goals

(Directing)

• Periodically comparing actual results with

the goals (Controlling)

Human Behavior

and Budgeting

Importance of setting a reasonable budget:

• Budgets set too tightly discourage employees

when expectations are too high.

• Budgets set too loosely lead to budgetary

slack – called “padding” the budget.

• Goal conflict occurs when the employees’ or

managers’ self-interest differs from the

company’s goals or objectives.

Choosing the Budget Period

Operating Budget

2011

2012

The annual operating budget

may be divided into quarterly

or monthly budgets.

2013

2014

A continuous budget is a 12month budget that rolls forward

one month as the current month

is completed.

Developing Budget Estimates

Zero-based budgeting requires

managers to estimate sales, production,

and other data as though operations are

being started for the first time.

More common methods involve revising

last year’s budget.

Master Budget

A master budget is a series of budgets

that are linked together.

Major parts of a master budget include:

Relationship of the Various Income Statement Budgets

Sales Budget

Production Budget

Total units

to be

sold

+

Desired

ending =

inventory

Total

units

needed

Total

units

needed

Expected

- beginning

inventory

=

Units

to be

produced

Production Budget

Calculation of the Purchases Budget

Raw material

needed

+

for

production

Desired

ending =

raw

material

inventory

Units to be

Produced

(Production

Budget) * DM

needed for each

unit

Price of Raw

Materials *Units of

Raw Materials

Total

raw

material

needs

Total

raw

material

needs

-

Expected

raw

material

beginning

inventory

=

Raw

material

to be

purchased

Raw Material Requirements

Wallet:

Leather: 0.30 square yard per unit

Lining: 0.10 square yard per unit

Handbag:

Leather: 1.25 square yards per unit

Lining: 0.50 square yard per unit

Direct Materials Purchases Budget

Direct Labor Requirements

Wallet:

Cutting Dept: 0.10 hour per unit

Sewing Dept: 0.25 hour per unit

Handbag:

Cutting Dept: 0.15 hour per unit

Sewing Dept: 0.40 hour per unit

Direct Labor Cost Budget

Factory Overhead

Cost Budget

Estimated Inventories

January 1, 2009:

Finished Goods: $1,095,600

Work in Process: $214,400

December 31, 2009:

Finished Goods: $1,565,000

Work in Process: $220,000

Selling and Administrative

Expenses Budget

0

0