1. The asset management

game: a primer

Chapter 1-4

McGraw-Hill/Irwin

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Major Types of Securities

Debt

Money market instruments

Bonds

Common stock

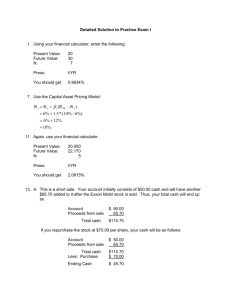

Preferred stock

Derivative securities

2-2

Markets and Instruments

Money Market

Debt Instruments

Derivatives

Capital Market

Bonds

Equity

Derivatives

2-3

Money Market Instruments

Treasury bills

Certificates of deposit

Commercial Paper

Bankers Acceptances

Eurodollars

Repurchase Agreements (RPs) and

Reverse RPs

Domestic interbank market

LIBOR Market

2-4

Bond Markets

Treasury Bonds and Notes

Agency Issues

International Bonds

Municipal Bonds

Corporate Bonds

Mortgage-Backed Securities

2-5

Derivatives Securities

Options

Basic Positions

Call (Buy)

Put (Sell)

Terms

Exercise Price

Expiration Date

Assets

Futures

Basic Positions

Long (Buy)

Short (Sell)

Terms

Delivery Date

Assets

2-6

Capital Market - Equity

Common stock

Residual claim

Limited liability

Preferred stock

Fixed dividends - limited

Priority over common

Tax treatment

2-7

Stock Market Indexes

Uses

Track average returns

Comparing performance of managers

Base of derivatives

Factors in constructing or using an Index

Representative?

Broad or narrow?

How is it constructed?

2-8

Examples of Indexes - Domestic

Dow Jones Industrial Average (30 Stocks)

Standard & Poor’s 500 Composite

NASDAQ Composite / NYSE Composite

Wilshire 5000

Nikkei 225 & Nikkei 300

FTSE (Financial Times of London)

Dax / CAC / MIB /

Region and Country Indexes

Stoxx

2-9

Bond Indexes

Lehman Brothers

Merrill Lynch

Salomon Brothers

Specialized Indexes

Merrill Lynch Mortgage

2-10

Construction of Indexes – I

How are stocks weighted?

Price weighted (DJIA)

Market-value weighted (S&P500, NASDAQ)

Equally weighted (Value Line Index)

How returns are averaged?

Arithmetic (DJIA and S&P500)

Geometric (Value Line Index)

2-11

Averaging Methods

Component Return

A=10%

B= (-5%)

C = 20%

Arithmetic Average

[.10 + (-.05) + .2] / 3 = 8.33%

Geometric Average

[(1.1) (.95) (1.2)]1/3 - 1 = 7.84%

2-12

Construction of Indexes - II

How are they updated?

intraday (MIB30, S&P/MIB)

daily (MIB)

How are the constituents chosen?

entire security universe (global index)

main securities (headline index)

securities sharing a common feature

sector, size, value source

2-13

Primary vs. Secondary Security Sales

Primary

New issue

Key factor: issuer receives the proceeds

from the sale

Secondary

Existing owner sells to another party.

Issuing firm doesn’t receive proceeds and

is not directly involved.

2-14

Investment Banking Arrangements

Underwritten vs. Best Efforts

Underwritten: firm commitment on

proceeds to the issuing firm.

Best Efforts: no firm commitment.

Negotiated vs. Competitive Bid

Negotiated: issuing firm negotiates terms

with investment banker.

Competitive bid: issuer structures the

offering and secures bids.

2-15

Public Offerings

Public offerings

registered with the authority (SEC, CONSOB)

sale is made to the investing public.

shelf registration (Rule 415, delega amm/tori)

Initial Public Offerings (IPOs)

Evidence of underpricing

Short and long term performance

Private placement:

sale to a limited number of sophisticated investors not

requiring the protection of registration.

Dominated by institutions.

Very active market for debt securities.

Not active for stock offerings.

2-16

Organization of Secondary Markets

Organized exchanges

Regulated markets

ATS / MTF / ECN

OTC market

Third market

Fourth market

2-17

Organized Exchanges

Auction (order driven) markets

centralized order flow on an electronic (limit)

order book

Dealer (quote driven) markets

competitive dealership function;

specialist role based either on issuer’s

mandate or exchange designation

Stock, futures & options, and to a lesser

extent, bonds.

2-18

Other Market

OTC

Dealer market without centralized order flow.

information system for individuals, brokers, dealers

Used for bonds, derivatives, stocks.

Third Market

Trading of listed securities away from the exchange, usually

involving services of dealers and brokers.

Institutional market: to facilitate trades of larger blocks of

securities.

Fourth Market

Institutions trading directly with institutions (no middleman)

Organized information and trading systems

ECN Development

2-19

Trading Services & Costs

Services

Order collection

Order routing

Execution

Confirmation and clearing

Central counterparty service

Settlement

Costs

Commission (brokers, exchanges, clearinghouse, CSD)

Bid/ask spread

Time to execution

2-20

Types of Orders

Instructions on how to complete the order

Market vs. Limit

Stop loss

Fill or kill vs. Good till …

Market opening / close

Margin trading

Asset purchase partly based on borrowed money.

Margin arrangements differ for stocks and futures.

In USA, maximum initial margin 50% set by the Fed

Maintenance margin is the minimum level the equity margin can be

Margin call: Call for more equity funds

2-21

Margin Trading - Initial Conditions

X Corp

Margin:

Initial Position

Stock $70,000

1000 shares purchased @ $70

50% Initial; 40% Maintenance

Borrowed $35,000

Equity

$35,000

New Position if price drops to $60 per share

Stock $60,000

Borrowed $35,000

Equity

$25,000

Margin% = $25,000/$60,000 = 41.67%

2-22

Margin Trading - Margin Call

How far can the stock price fall before a

margin call?

(1000P - $35,000)* / 1000P = 40%

P = $58.33

* 1000P - Amount Borrowed = Equity

2-23

Short Sales

Purpose: to profit from a decline in the price

of a stock or security.

Mechanics

Borrow stock through a dealer.

Sell it and deposit proceeds and margin in an

account.

Closing out the position: buy the stock and

return to the party from which it was

borrowed.

2-24

Short Sale - Initial Conditions

Z Corp

Margin:

100 Shares

@ $100

50% Initial;

30% Maintenance

Sale Proceeds $10,000

Stock Owed $10,000

I. Margin 5,000

Equity 5,000

Stock Price Rises to $110

Sale Proceeds

$10,000

Margin

$ 5,000

Stock Owed $11,000

Net Equity $ 4,000

Margin % (4000/11000) = 36% > 30% (maintenance m.)

How much can the price rise before a margin call?

(15,000* - 100P) / (100P) = 30% P = $115.38

* Initial margin plus sale proceeds

2-25

Regulation of Securities Markets

Fair and orderly trading

Insider trading and market abuse

Pre and post trade transparency

Order routing (concentration vs. fragmentation)

Trading rules (tick size, priority, circuit breakers,…)

Conduct of business

conflict of interests (prevent, manage, disclose)

retail investor protection

Regulation

Law, Authority

Exchange

Self-Regulation

2-26

Investment Companies

Services

Administration & record keeping

Diversification & divisibility

Professional management

Reduced transaction costs

Types

Unit Trusts

Managed Investment Companies

Open-End

vs.

Closed-End

Other investment organizations

Commingled funds

REITs

Hedge funds

2-27

Net Asset Value

Used as a basis for valuation of

investment company shares.

Selling new shares

Redeeming existing shares

Calculation

Market Value of Assets - Liabilities

Shares Outstanding

2-28

Open-End vs. Closed-End Funds

Shares Outstanding

Closed-end:

no change unless new stock is offered.

Open-end:

changes when new shares are sold or old shares

are redeemed.

Pricing

Open-end:

Net Asset Value(NAV)

Closed-end:

Premium or discount to NAV

2-29

Investment Policies

Money Market

Fixed Income

Equity

Balance & Income

Asset Allocation

Indexed

Specialized Sector

2-30

Costs of Investing in Mutual Funds

Fee Structure

Front-end load

No load

vs.

Back-end load

Operating expenses

12 b-1 charges

distribution costs paid by the fund

Alternative to a load

Fees

Management fees

Performance fees (symmetric vs. fulcrum)

Bounds, high watermark, frequency

2-31

Exchange Traded Funds

Allow investors to trade funds based on

indexes like stock.

Examples

SPDRS

WEBS

HOLDERS

Allow sector specialization

2-32

A First Look at Fund Performance

Most funds underperform their benchmark

Not fair comparison because of costs

Result holds even if passive management costs

considered.

Do some mf consistently outperform?

Some evidence suggests so

Depends on measurement interval and on time period

Evidence shows consistency of poor performance

Correlation with high fees

2-33

Sources of Information on Mutual Funds

Morningstar

Press

Assogestioni

Wiesenberger’s Investment Companies

Investment Company Institute

Information providers

Advisors

2-34