Chapter 2 Notes

advertisement

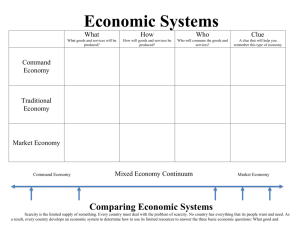

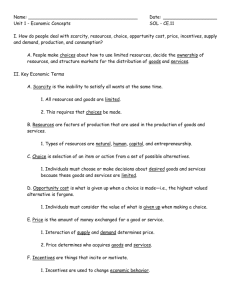

Chapter 2 Economic Resources and Systems Section 2.1 Economic Resources Making Economic Decisions Because of scarcity (i.e. the lack of something, not enough) all businesses must make decisions. Scarcity is the result of limited resources vs. unlimited wants and needs. Reading Check p.23 Factors of Production: all the economic resources needed to produce a good or service. There are four factors of production: Natural Resources Labor/Human Resources Capital Resources Entrepreneurial Resources Natural Resources: are raw materials that come from nature such as crops, ores, animals, fish, water, etc. Some natural resources are renewable such as crops and animals while others are non-renewable such as oil, coal, etc. Use the one hundred year rule: If something can be replenished within one hundred years it should be considered renewable. If it takes more than one hundred years than it should be considered non-renewable The amount of natural resources a country has directly affects a nations economy. Reading Check p.24 Labor/Human Resources: people used to make goods or services. Labor can be skilled or unskilled, physical or intellectual. Capital Resources: the things used to produce goods or services such as buildings, materials and equipment and can also be referred to as capital goods. Reading Check p.25 Entrepreneurial Resources: the ideas that business people come up with to provide goods or services (i.e. the assembly line, the light-bulb, computers, etc.) After You Read p.26 Section 2.2 Economic Systems Basic Economic Questions: What to produce? How should it be produced? (i.e. what resources will be used?) Who should share in what is produced? (i.e. who gets it?) Answering these questions results in opportunity costs. Opportunity Costs are what you give up in order to make the choices you make. (i.e. using $10 to go to the movies results in various opportunity costs that you could have done with that money such as save it.) Different Types of Economies: An Economic System is the method a society uses to distribute resources. The type of economic system will determine how the above questions are answered. Market Economies: economic system in which economic decisions are made in the marketplace and may also be called a private enterprise system (resources are owned privately) or free enterprise system, or capitalism. In a market economy, individuals are responsible for being informed and making careful decisions. Reading Check p.29 Price: the amount of money given or asked for when goods or services are bought or sold. Supply: the amount of goods and services that producers will provide at various prices. Once again profit is the goal. The higher the price the producer can get will make them willing to provide more of the good or service and the lower the price the less they will produce. This is the “LAW OF SUPPLY” Demand: the amount of goods and services people are willing and able to buy. The higher the price the less consumers will buy. The lower the price the more they will buy. This is the “LAW OF DEMAND” Equilibrium is the place where supply and demand are equal (see fig 2.1 p.30) Demand and Supply are both affected by price. Command Economies: economic system in which a central authority (i.e. the government) makes the key economic decisions. The gov’t also owns and controls most of the resources. In this type of economy businesses and consumers have little to no choice in what to produce or buy. Communism and Socialism are two forms of Command Economies. Mixed Economies: In reality, few nations have a pure market economy or pure command economy. Most countries have a mixture of the two where private ownership of property and individual decision making are combined with government intervention and regulations. What type of Economy does the United States of America have? After You Read p.31