Ch 7 Notes

advertisement

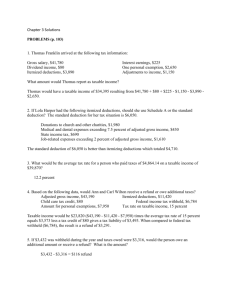

Chapter 7 Federal Income Tax Lesson 7.1 Our Tax System I. Types of Taxes A. Revenue—money collected by the government from citizens and businesses the form of taxes 1. Income taxes is the largest source of government revenue 2. Other taxes—social security, unemployment, insurance, inheritance and estate, excise, import duties, personal property B. Progressive taxes—taxes that take a larger share of income as the amount of income grows 1. Federal income taxes 2. Tax Rates (single) Tax Rate Taxable Income 10% >0 15% >$9,075 25% >$36,900 28% >$89,350 33% >$186,350 35% >$405,100 39.6% >406,750 C. Regressive Taxes—taxes that take a smaller share of income as the amount of income grows 1. Consumption taxes are regressive—Sales tax 2. Excise tax—sales taxes imposed on specific goods and services (gasoline, cigarettes, alcohol, air travel, TELEPHONE SERVICE) D. Proportional taxes—(flat taxes) taxes for which the rate stays the same, regardless of income—property taxes E. Taxes provide services 1. Local level--taxes provide education, parks and playgrounds, roads, police, fire 2. National level—salaries for Congress, funds for National Defense, highways, welfare, foreign aid, wildlife refuges II.Components of the Tax System A. The IRS—Internal Revenue Service 1. Agency of the Department of the Treasury 2. Main function is to collect income taxes and enforce tax laws 3. Also provides services to taxpayers a. Assist taxpayers in finding information and forms b. Furnishes tax information and instruction booklets free to schools c. Maintains a web site www.irs.gov, where you can get tax info, download tax forms, file taxes electronically d. Also get tax forms from the public library B. The Power to Tax 1. The power to levy taxes rests with Congress 2. Revenue bills must pass a vote in both the House and the Senate and then be signed by the president before they become law C. Paying Your Fair Share 1. Our income tax is graduated—tax rates increase as taxable income increases 2. Tax rates apply to income ranges, or tax brackets 3. Congress increases the tax rates when needed to bring in more $ to balance the budget 4. Deficit—when government spends more than it receives in revenue 5. Voluntary compliance—all citizens are expected to prepare and file income tax returns by April 15 of each year 6. Responsibility to file and pay taxes rests with each individual 7. Failure to do so can result in a penalty: interest charges on tax owed plus a fine and/or imprisonment 8. Tax evasion—willful failure to pay taxes, punishable by a fine, imprisonment, or both C. An IRS Audit 1. Audit—examination of tax return 2. Taxpayers may represent themselves, give some the power to take their place (lawyer, CPA, family member, or licensed tax agent) or can bring anyone for support. 3. Audits usually involve confirming supporting documentation 4. Correspondence audit—much more common, IRS sends a letter asking taxpayer to answer ?s or produce evidence of deductions 5. May also have office audit or field audit (agent visits the taxpayer) Lesson 7.2 Filing Tax Returns I. Definitions of Terms A. 1. 2. 3. 4. Filing Status Single—not married Married filing a joint return Married filing a separate return Head of Household—meet certain conditions and provide a home for dependents 5. Qualifying widow(er) with a dependent child B. Exemption—an amount you may subtract from your income per dependent 1. Dependent—person who lives with you and receives more than half his/her living expenses from you 2. Dependents may include children, spouse, elderly parents, disabled relatives C. Gross Income—all the taxable income you receive, including wages, tips, salaries, interest, dividends, unemployment compensation, alimony, workers’ comp 1. Not taxable—child support, gifts, inheritances, life insurance benefits, veterans’ benefits 2. Other taxable income—gambling winnings, bartering, pensions, annuities, social security benefits, self-employment income, rental income, royalties, estate and trust income, income on sale of property 3. Wages Salaries, and Tips—W-2 includes all employment income 4. Interest Income—taxable interest from banks, savings and loan associations, credit unions, series HH savings bonds— should receive a Form 1099-INT for each investment earning interest 5. Dividend Income—money, stock, or other property that corporations pay to stockholders in return for their investments—will receive a Form 1099DIV for each stock investment. 6. Unemployment Compensation—Form 1099-G shows the total received 7. Social Security Benefits—85% is taxable if total income > $25,000 single or $32,000 married filing jointly. Form SSA-1099 8. Child support—money paid for support of dependent children, not taxable for person receiving it nor deductible for person paying it 9. Alimony—money paid to support a former spouse. Taxable for the person receiving it and deductible for the person paying it. D. Adjusted Gross Income 1. “Adjust” your income by subtracting certain things (IRA, student loan interest, tuition, educator expenses) 2. Adjustments reduce your income subject to tax E.Taxable Income 1. Deductions—expense the law allows you to subtract from your adjusted gross income to determine your taxable income 2. Itemize—list the allowable expenses on your tax return using Schedule A and Form 1040 (Medical, dental; state, local, property taxes; mortgage interest; gifts to charity; moving expenses; work expenses) 3. Standard deduction—stated amount that you may deduct from AGI instead of itemizing; based on filing status 4. Your choice to itemize or take standard deduction (take the higher) 5. Taxable income—income on which you pay tax 6. Gross Income—Adjustments=Adjusted Gross Income (AGI) AGI—Deduction (Std or Item)— Exemptions=Taxable Income Look up taxable income in tax table Tax—Credits—Withholding=Tax owed or Refund due F.Tax Credits—an amount subtracted directly from the tax owed 1. Every dollar off a credit comes off the tax owed 2. College tuition, childcare, children, earned income II. Preparing to File A. Who Must File? 1. 2. Single, under age 65, earning >$10,150 If <$10,150, file to claim refund of taxes withheld B. When to File April 15 C. Which Form to Use? 1. Three basic forms—1040EZ, 1040A-- (short forms) 2. 1040—(long form), itemize, >$100,000 taxable income D. Where to Begin? 1. Save all receipts and proofs of payment for itemized deductions 2. Compare paycheck stubs to W-2 (receive by Jan 31) 3. Use last year’s return as a guide 4. File ASAP to get refund ASAP 5. Check amount of itemized deductions (over $6,200, single) 6. Sign form to verify accuracy 7. Amended return (1040X) to make corrections 8. Save copies of tax returns, receipts, Forms W-2, Forms 1099, for six years E. Filing Electronically www.irs.gov/efile Free if your AGI < $60,000 III. Preparing Your Income Tax Return A. Complete in ink or typed with no errors or omissions B. Tax Preparation Software (TurboTax) C. Form 1040EZ 1. Single or Married and claim no dependents, taxable income <$100,000 a. Name, address, social security number b. Report income, indicate if you are a dependent on someone else’s tax return c. Compute tax—use tax table, subtract amount withheld d. Refund or Amount Owed, can have refund deposited electronically into bank account—takes only 2—3 weeks e. Sign and date the return, attach W-2, mail to regional IRS office—Fresno, CA— refund, Cincinnati, OH--Pay D. Form 1040A—can take deductions for IRA (Individual Retirement Accounts) contributions, tax credit for child-care expenses a. b. c. d. Name, address, social security number Filing status Exemptions Total income Adjusted gross income f. Subtract standard deduction and exemptions to calculate taxable income g. Compute tax—use tax table, subtract credit for childcare expenses, child tax credit, subtract amount withheld h. Refund or Amount Owed i. Sign and date return e. Aren’t Taxes FUN??!!??