xin-paper_research_project

advertisement

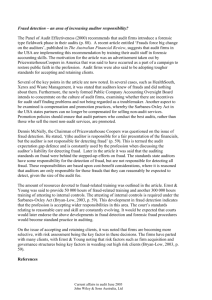

Running head: AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES An Empirical Study on Accounting and Auditing Enforcement Releases Cases Xin Tan Southeast Missouri State University Author Note This paper was submitted in partial fulfillment of the requirements of the degree of Masters in Business Administration AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Abstract The objective of the paper is to provide an empirical study about the characteristics of accounting fraud and fraudulent financial reporting occurrences, including violation length, industry, audit tenure and violation types. To do so, I collected Accounting and Auditing Enforcement Releases (AAERs) issued by the Securities and Exchange Commission (SEC) for accounting fraud committed by companies during 2009-2011, which provides a fraud sample consisting of 66 companies. I analyzed each incident and explore key company characteristics in instances of fraudulent reporting in AAERs. i AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES APPLIED RESEARCH ACCEPTANCE SHEET An Empirical Study on Accounting and Auditing Enforcement Releases Cases Submitted by Xin Tan in partial fulfillment of the requirements for the degree of Masters in Business Administration. Accepted on behalf of the Faculty of the School of Graduate Studies and Research by the Applied Research Project Committee. (Date) Advisor/Chair (Name,Ph.D.) ______________________________ (Date) MBA Coordinator (Name, Ph.D.) ii AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES CONTENTS ABSTRACT.............................................................. .............................. ……………. i AC CEP TANC E P AGE............................. ................. ………………… ii CONTENTS....................................... …………....................................... …………iii INTRODUCTION……………………………………………………. …...1 LITERATURE REVIEW……………………………………………… .....3 METHOD…………………………………………………….……………… 4 RESEARCH DESIGN AND RESULT ………………………………...… 5 CONCLUSION………………………………………… ……………….....15 LIMITATION…………………………………………………..... .... …...... 16 REFERENCES………………………………………………………… . …18 A P P E N D IX … … … … … … … … … … … … … … … … … … … … … … . … … . 2 0 iii I. Introduction While the United States experienced an unprecedented storm of accounting fraud, like Enron and WorldCom, around the beginning of twenty-first century, it is still unclear to what extent the typical fraud profile has changed in recent years. In the last decade, the accounting industry has made a variety of legislative and regulatory changes because of accounting fraud, such as the Sarbanes-Oxley Act of 2002. This act was enacted as a reaction to major accounting scandals and it enhanced standards for all U.S. public companies boards, management and public accounting firms. Fraudulent financial reporting can have significant consequences for companies, stockholders, investors, auditors and regulators. High profile fraud cases may decrease the credibility of the financial reporting system and erode the confidence of capital markets. Whether or not companies are likely to engage in accounting fraud is not easy to determine or obvious to track. That’s why this research analyzed the firms who were involved in fraudulent financial reporting and aimed to provide a useful understanding of fraud occurrences. The Committee of Sponsoring Organizations of the Treadway Commission (COSO) conducted studies (Beasley et al, 1997) about fraudulent financial reporting in order to provide a comprehensive analysis of fraud incidents investigated by the SEC. It offered a great method for researchers to analyze companies who committed fraud and fraud occurrences. This paper follows COSO’s method to collect sample firms and make an empirical study of those cases. Every sample firm in this paper was investigated by the SEC and presented in Accounting and Auditing Enforcement Releases (AAERs) during a three year period from 2009 to 2011. The AAERs summarizes the actions brought by the SEC against public companies, audit firms, mangers and auditors. Moreover, those releases contain the process of the fraud occurrences, such as name of firms or people, violation date, time period, 1 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES types of fraud and the main purpose of fraud. Some of those cases even indicate the dollar amount of money involved in the fraud and monetary penalties for the firms who committed fraud. This paper identifies 66 organizations involved in fraudulent financial reporting. There are two advantages to analyzing sample organizations. On one hand, it will help people to obtain a better understanding of organizations involved in fraudulent reporting and the fraud process. Most of the occurrences of accounting fraud behavior are the result of behavior tending towards the firms’ benefit. For example, Farber (2005) indicated that 60 percent of the fraud involved in fictitious transactions, such as creating phony invoices, which tend to overstate net income. Finding out the key features of recent fraudulent activity will help outsiders, such as auditors, regulators and potential investors to more accurately evaluate organizations. This research differs from previous studies in the following aspects: first, data from previous studies are outdated and may not represent the current relationships and facts. Second, the present research focuses on AAER cases against companies, not individual people. The remainder of this paper is organized as follows. In section II, a brief review of the relevant literature is provided. Section III presented the research method and a description of the sample. Section IV contained the research design and empirical results. A summarized conclusion is provided in Section V. 2 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES II. Literature review There is much research available on fraudulent financial reporting based on the empirical study. Previous researchers have tested and verified almost every aspect of firms identified by SEC as fraudulently reporting. One study supported by COSO in 1997 analyzed 347 accounting fraud cases, providing an extensive updated analysis of financial statement fraud occurrences. One of the finding was that “most fraud overlapped at least two fiscal periods, frequently involving both quarterly and annual financial statements.”(Beasley et al, 1997, P.7) Most of the literature clustered in governance mechanisms. Beasley (1996) found that larger proportions of outside members on the board of directors significantly reduced the likelihood of reporting fraud and that fraud does not have a connection with committees meets. Farber (2005) examined the association between the credibility of the financial reporting system and the quality of governance mechanisms. Sample firms tend to have poor governance relative to control sample firm. He found that firms who committed fraud have fewer audit committee meetings and a small percentage of Big Four1 audit firms. He also mentioned that improve governance would results in superior stock price performance. Coffee (2002) and Cox (2003) highlighted some cases of fraudulent financial reporting of public accounting firms to indicate the undeniable link between auditors and fraud companies. The sample firms showed an obvious preference for inflated profit rather than the inflated net assets in fraudulent financial reporting. With inflated profit, fictitious income is the most common technique and obtained by the inflated sales’ revenue. Lennox 1 The Big Four present the four largest professional services networks in accountancy and professional services, which handle the vast majority of audits for publicly traded companies. This group is known for the following companies: PricewaterhouseCoopers, Deloitte Touche Tohmatsu, Ernst & Young and KPMG. Others present other auditors except Big Four. 3 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES and Pittman (2010) conducted a research study about whether the Big Four public accounting firms are associated with higher quality financial statements. They suggested that the clients of the Big Four firms are less apt to engage in fraudulent financial reporting. Maksimovic and Titman (1991) found that companies are more likely to commit fraud when they have longer audit firm tenure because they suffered from financial distress. The General Accounting Office (GAO) indicated that “mandatory audit firm rotation may not be the most efficient way to strengthen audit independence” (2003, Highlights). Thus an increasing number of researches papers to address this point have emerged in recent years. Carcello (2004) examined the relation between audit firm tenure and fraudulent financial reporting and found that in the first three years of engagement relationship is more likely to detect fraudulent financial reporting. However, he failed to find evidence to prove longer client relationship would lead audit failure. O’Mally (2002) examined auditor tenure and auditor performance but failed to detect a relationship between tenure and fraudulent financial reporting. New York Stock Exchange (2003) advised that companies should periodically change their audit firms for high profile audit quality. III. Methods Sample collection In order to conduct this research, samples are quite essential in every aspect. The researcher use AAERs as a proxy for the occurrence of fraud. Consistent with Beasley (1996), this proxy is intended to capture extreme cases of fraud in the error-to-fraud continuum. The analysis period is restricted to three years to make data collection more accessible. The AAERs appear to be reasonable sources for identifying financial statement fraud occurrences because they depict the detail of each fraud and it is controlled by Securities and Exchange Commission (SEC). Another source of my research is the EDGAR 4 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES database. It provides access to corporate information, including a company’s financial information, registration statements, prospectuses and periodic reports. An illustrative example of SEC’s justification for issuing AAERs follows (per AAER No. 3093, in the case of UTstarcom, Inc.): The SEC's complaint charges UTStarcom with violations of the anti-bribery, books and records, and internal controls provisions of the FCPA (Sections 30A, 13(b) (2) (A) and 13(b) (2) (B) of the Securities Exchange Act of 1934, respectively). UTStarcom agreed, without admitting or denying the charges, to the entry of a permanent injunction against FCPA violations and to provide the SEC with annual FCPA compliance reports and certifications for four years, in addition to paying the $1.5 million penalty. According to Vinod (2002), “An industry is a collection of firms offering goods or services that are close substitutes of each other”. That’s why all fraud firms in this paper were reviewed to identify with the four-digit SIC code. The researcher obtained this data from SEC 10-K Form. The first two-digit as general SIC code is taken in order to facilitate the analysis of the sample firm’s industry distribution. IV. Research Design and Results Table 1 provides the information about the sample. The SEC issued 437 AAERs related to the violation of regulations from the year from 2009 to 2011. Three hundred and twenty two of them are firms not involved in financial statement fraud or are cases against individual CPA or auditors. I abandoned 21 firms because they did not file any financial statement to the SEC and 23 more firms because financial statement data was unavailable. Finally, 5 more samples were deducted from the final sample because the cases were 5 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES duplicative. Thus, there are 66 firms allegedly engaged in fraudulent financial reporting and investigated by SEC that were used as research. Table 1: Sample Selection of 66 Firms Subject to AAERs Number of AAERs issued between 2009 and 2011 Less: AAERs against individual CPA or auditors Firms without SEC files Firms without proxy or financial statement data Duplicate firms Final Sample 437 322 21 23 5 66 After making sure all the information is accurate, the researcher started to manage the data to generate results in an effective way. Inputting or uploading the data into a spreadsheet. Then, based on the shape of the charts and the data itself, the researcher was able to categorize each fraud firm by SIC Code. Table 2 indicates that sample firms were widely distributed among industries. Consistent with COSO’s 1999 and 2010 study, fraud occurred in a variety of industries but unlike their findings, manufacturing account for about 42% of the incidents, with 28 firms out of 66 in this research. According the 2010 COSO study, the most frequent industries cited were computer hardware and software, with a number of 20%. One reason of the different results is that the COSO study measured samples by numbers of schemes occurred in total while the researcher measured samples by numbers of firm. In general, Table 2 shows no significant difference in industries so it is a good idea to limit behavior of prevention in any particular industry. 6 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Table 2: Sample Firms Distribution by Types of Industry Services 17% Mining 12% Finance, Insurance and real estate 11% Retail trade 6% Wholesale trade , 6% Transportation, communications, electric, gas and sanitary services 6% Manufacturing 42% Table 3 reports summary statistics of the sample. The company data are picked from their SEC 10-K filings and those financial numbers are cited at the first year of violation date. It shows zero in net sales and total assets because one incidence is startups with not assets or revenues in its construction phrase. There is a significant difference between median and mean in net sales, net income and total assets, which implies that some big numbers occurred and greatly pull up the average number. Johnson et al. (2002) stated that “In the United States, there is no mandatory audit firm rotation and companies tend to change auditors after relatively long tenure. Consequently, the age of the client and the tenure of the audit firm may be correlated”. Consistent with their research, the researcher measured the audit firm tenure as the number of consecutive years that the audit firm has audited the client and used SEC files to collect audit tenure. The table indicates that most schemes lasted several years. They average violation period is 4.36 years, with median fraud period 4 years. In another point of view, frauds or violation behaviors are not easy to prevent in a single fiscal year. 7 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES The average audit tenure is about 2 times longer than the length of GAAP violation. Since client-specific knowledge is useful in detecting material misleading presentation in the financial reports, the longer tenure of the audit firm, the more likely the auditor will be able to detect financial fraud or errors. Table 3: Descriptive Statistics of Sample Firms No. of Sample Median Mean Std. Deviation Max Min Company Data: No. of Employees 66 3,920 22,145 68,259 426,751 6 Net Sales (In thousands) 66 $502,604 $3,547,150 $7,190,884 $38,300,000 0 Net Income (In thousands) 66 $16,926 $371,785 $1,679,639 $13,425,000 ($370,000) Total Assets(In thousands) 66 $491,949 $5,406,624 $14,791,796 $109,022,000, 0 Auditor Data: Audit Tenure (In years) 66 8 7.89 4.72 18 1 Length of Violation (In years) 66 4 4.36 2.92 15 1 Money Involved (In thousands) Penalty (In thousands) 51 45 Violation Data: $8,800 $1,000 $72,340 $9,800 $173,685 $31,497 $921,000 $177,000 $80 $25 Note: One observation reported zero in net sales and total assets because it is startups with no assets or revenues in its construction phrase. In order to obtain a more comprehensive understanding between audit tenure and violation length, the author makes a scatter diagram and use a Pearson correlation test to determine if the two variables are linearly related. Consistent with peer research, Table 4 shows a positive liner relationship connects audit tenure and length of violation. The correlation coefficient r = 0.25 (p=0.04). 8 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Table 4: Scatter Diagram about Audit Tenure and Violation Length Audit Tenure (In Years) 16 14 12 10 8 6 4 2 0 5 10 15 20 Violation Length (In Years) Table 5 presents the violation length by audit tenure type of audit firm. Because the average audit tenure is 7.89 years, the researcher defined short audit tenure as less than eight years, and long audit tenure as eight years or more. Even though client-specific knowledge is useful in detecting material misleading presentation in the financial reports, sample firms which maintain longer audit tenure have longer length of violation. On the one side, it supports the advice of New York Stock Exchange (2003) which states mandatory audit firm rotation would have positive effect on financial reporting. On the other side, the results of independent samples t-test show mean of 4.0 for Short and 4.67 for Long Tenure, p=.26, which indicates the means of the two factors do not indeed differ significantly. There are 50 out 66 sample firms (76%) employ Big Four auditors. The difference of audit tenure between Big Four auditor and other auditors seems significant, compared 9.24 years to 3.69 years. It implies that Big Four auditors are likely to maintain longer clientcustomer relationship than other auditors. One important finding is that there is no significant difference between length of violation and audit tenure when sample firms employ Big Four 9 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES auditors. However, firms employ non Big Four auditors show about 2-year difference in length of violation. Table 5: Exhibit Violation Length by Audit Tenure Type of Audit Firm Average Audit Tenure Others Big Four Total No.of Sample Mean (In Years) St.Dev (In Years) No.of Sample Mean (In Years) St.Dev (In Years) No.of Sample Mean (In Years) St.Dev (In Years) 16 3.69 2.39 50 9.24 4.43 66 7.89 4.68 Violation Length Short Tenure Long Tenure 14 3.57 2.92 16 4.38 2.20 30 4.00 2.63 2 5.50 3.50 34 4.62 3.03 36 4.67 3.06 Average Tenure16 3.81 3.13 50 4.54 2.79 66 4.36 2.90 Based on information provided by AAERs cases, the researcher identified techniques used for fraudulent financial reporting. Table 6 offers a recap about methods of fraud. Misleading presentation includes all frauds related to the financial statement, including misreported statement and note disclosure, such as fictitious transactions, misstatement of assets and improper use of accounting practice. Overstated income techniques represent fraud behavior driven to boost income illegally, such as fictitious revenue recognition, and understatement expenses or liabilities. Insufficient internal controls would lead a company to unreliable financial reporting and ineffective operations, examples include improper payment and bribery. Regulation violation relate to other miscellaneous issues related to legal regulations, like illegal procedures in acquisitions. Among the 66 observations, 58 (88%) of them are investigated by SEC because of misleading presentation and 38 (58%) of them overstated their income. The main motivation for violation and fraud behavior is to boost profit and bolster financial performance. In speaking of internal controls, they have significantly impacted on the reliability of financial reporting and effectiveness of operations, which may lead to fraud occurrence. When more 10 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES than half of the observations are involved in insufficient internal control, it is not surprising to notice they are on the list of AAERs. Table 6: Exhibit Fraudulent Reporting Methods Types of Violation Mislead Presentation Overstate Income Insufficient Internal Controls Regulation Violation Total Numbers of Firms 58 38 28 5 - Percentage of Total 88% 58% 42% 8% - Note: Most AAERs describe multiple infractions. Thus, the table does not sum to 100%. As noted in Table 7, the most common scheme used for fraudulent reporting is improper payment (32%), which is the result of insufficient internal controls. One instance for improper payment is Watts Water Technologies, Inc. (AAERs No.3328). Its subsidiary (CWV) in China made illegal payments to employees of an institute, who assisted in design and construction to CWV’s project. The purpose and effect of those payments was to force the institute to recommend its value of products and facilitate its sales. The improper payments generated profits for Watts of more than $2.7 million. Twenty-seven percent of the 66 sample firms’ financial statements were misstated through the understatement of expenses or liabilities. Cablevision Systems Corporation (AAERs No. 2920) is a diversified entertainment and telecommunications company. From 1999 through 2003, it recognized certain costs as current expenses when the cost should not have been recognized in those periods. It overstated expense in earlier fiscal periods and understated expenses in later periods. The improper recognized expenses understated $7,895 million expenses from 2001 to 2003, which results 5.1% understatement in net loss of 2003. Even though bribery has relatively small percentage compared to others, it is a very specific scheme and cannot be neglected. The SEC alleges that a subsidiary of Maxwell Technologies, Inc. (AAERs No.3236) for repeatedly paying bribes to government officials in China to obtain business from several Chinese state-owned entities. Maxwell manufactures 11 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES energy storage and power delivery products. A Maxwell subsidiary paid over $2.5 million in bribes from 2002 through May 2009 for contracts that generated more than $15 million in revenues. There are 7 incidents (11%) found related to backdate stock options. One example is about Hain Celestial Group, Inc. (AAERs No. 3045). At least from1998 to 2002, Hain fraudulently backdated stock options granted to Company officers, directors, and employees, concealing millions of dollars in expenses from the Company's shareholders. It granted stock options at earlier dates in order to gain profit of low stock prices and misreport it on its SEC filings. Misconduct inventory is one of the most common techniques to overstate of assets. Among all 66 samples firms, there are 6 of them committed misconduct inventory. Thor Industries, Inc. (AAERs No.3280) was filed by SEC because Thor engaged in a fraudulent accounting scheme to understate Dutchmen’s cost of goods sold. Thus, it would avoid recognizing inventory costs that were not reflected in Dutchmen’s financial accounting system. Table 7: Exhibit Types and Frequencies of Schemes 35% 30% 25% 20% 15% 10% 5% 0% 32% 27% Improper payment Understate expense 9% 11% 9% Bribery Backdate stock option Misconduct inventory Note: Those are the most common schemes employed by sample firms and most of firms committed multi-schemes at single fiscal year. Thus, the sum of percentage does not equal to 100 percent 12 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Table 8 indicates the detail information about descriptive statistics of dollar amount money involved in the incidents and the penalty by the schemes presented in Table 7. In this research, the researcher found 51 AAERs cases (77%) specifically indicated the dollar amount of money involved in schemes and 45 cases (68%) were fined by monetary penalties. One important discover provided by Table 8 is that bribery comes with a heavier penalty than other GAAP violation. The average dollar amount associated with bribery is $5 million, which is the smallest number compared to other four violations. However, the average penalty for firms committed bribery is about $42 million, which is almost 10 times higher than improper payment and inventory misconduct, and 70 times higher than backdating stock options. It is not difficult to understand this finding because bribery is not only a business behavior violation, but also relates to ethical or moral issue. Table 3 of Appendix presents the detail information of percentage distribution about penalty over dollar amount of fraud. The average percentage influence of penalty over fraud amount is 37% while the median percentage is 11%. As mentioned above, each AAERs case engaged in more than one GAAP violations and detailed information is not presented well in the documents, so I cannot clearly allocate the specific dollar amount in every violation. In other words, numbers shown in the table for infractions are overlapped and overstated. However, Table 8presents the general relationship tendency between dollar amount of fraud and penalties. 13 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Table 8: Descriptive Statistics about Dollar Amount of Fraud and Penalty by Types of Scheme. Dollar amount of fraud Type of Fraud Involving Improper payment Understate expense Bribery Backdate stock option Misconduct inventory Penalty Type of Fraud Involving Improper payment Understate expense Bribery Backdate stock option Misconduct inventory No. % Mean Median St.Deviation Max Min 21 32% 18 27% 6 9% 7 11% 6 9% 82,984,631 75,930,279 5,036,000 109,439,571 139,890,000 13,000,000 20,500,000 2,500,000 37,000,000 27,000,000 177,189,488 155,046,949 5,348,082 133,307,340 241,375,327 622,000,000 622,000,000 15,000,000 399,500,000 622,000,000 81,000 185,673 80,000 2,677,000 250,000 21 32% 18 27% 6 9% 7 11% 6 9% 4,254,059 1,881,415 42,149,344 637,581 4,242,800 1,839,325 283,500 8,000,000 162,320 973,100 4,800,249 4,048,295 67,923,279 936,974 6,257,143 15,000,000 15,000,000 177,000,000 2,500,000 15,000,000 30,000 46,200 217,000 25,000 25,000 In Table 9 and Table 10, the changes are varied in every percentage number and the influence of net income is much greater than net sales. The average impact percent on net sales is 3.75% and on net income is 8%. Those tables provide distribution of Penalty impact on net sales and net income by penalties respectively. Most changes are less than 1 % of both net sales and net income, which implies that monetary punishment may not enough to prevent fraud. Table 9: Distribution of Penalty Amount as a Percentage of Net Sales 76% 11% 9% 2% Less than 1% 1%-5% 5%-10% 14 2% 10%-100% Over 100% AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Table 10: Distribution of Penalty Amount as a Percentage of Net Income 47% 18% 13% 16% 7% Less than 1% 1%-5% 5%-10% 10%-100% Over 100% Note: Percentage changes are both negative and positive, because 20 out of 66 sample firms have net loss and 1 firm is a startup with no net income and net sales. V. Conclusion Based on the results and the discussions above, this study explores several key conclusions. Firstly, fraudulent financial reporting occurs in a variety of industries. Even though fraudulent financial reporting is more likely to occur in some particular industries, we can never limit behavior of prevention fraud in those industries. Secondly, fraud reporting needs to be watched and prevented at the very first time, because the occurrence is not easy to prevent in a single fiscal year. Thirdly, audit tenure and length of violation are linearly related to each other, and longer audit tenure tends to have longer length of violation. Big-Four audit firms tend to obtain longer audit tenure compared with others. Moreover, whether or not periodically 15 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES change audit firms would shorten the length of violation is still unclear because the means of violation length and audit tenure do not differ significantly. Fourthly, improper revenue recognition is the leading type of fraud, which implies the main motivation for violation and fraud behavior is to boost profit and bolster financial performance. Fifthly, the consequences of fraudulent scheme are severe to fraud firms and monetary punishment differs in types of scheme. Penalties do not have significant impact on companies, because percentage changes on both net sales and net income are less than 1 %. VI. Limitations There is a significant time lag between the occurrence of fraud and the issuance of AAERs case, and most of frauds are happened before 2009. Thus, the information and conclusion offered in this study may be behind. The use of AAERs has limitations. For example, because the SEC selects cases for which it has the best chance of winning a judgment, they are likely to include instances of the most extreme misleading reporting. Therefore, the results of this study are not likely to be generalized to the entire population of firms that report fraudulently. 16 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Almost every sample firms committed more than one scheme at the same time period. The researcher is unable to allocate the specific dollar amount of fraud for each scheme and according penalties. The data in Table 8 is inevitably overrated and inaccurate. 17 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES References Accounting and Auditing Enforcement Releases. Retrieved from http://www.sec.gov/divisions/enforce/friactions.shtml Beasley, M.S. (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. The Accounting Review 71 (October): 443465. Beasley, M. S., Carcello, J.V., and Hermanson, D.R. (1997). Fraudulent Financial Reporting: 1987-1997, An Analysis of U.S. Public Companies. New York: COSO. Beasley, M. S., Carcello, J.V., Hermanson, D.R., and Neal, T.L. (2010). Fraudulent Financial Reporting: 1998-2007, An Analysis of U.S. Public Companies. New York: COSO. Carcello, J., and Nagy, A. (2004). Audit Firm Tenure and Fraudulent Financial Reporting. Auditing:A Journal of Practice and Theory 23 (2): 55–70. Coffee, J. C. (2002). Understanding Enron: It’s about the gatekeepers, stupid. Working paper, Columbia University School of Law. Cox, J. D. (2003). Reforming the culture of financial reporting: The PCAOB and themetrics for accounting measurements. Washington University Law Review 81 (2):301–27. General Accounting Office (GAO). (2003). Public Accounting Firms Required Study on the Potential Effects of Mandatory Audit Firm Rotation. Retrieved from http://www.gao.gov/assets/250/240738.pdf 18 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Johnson, V., Khurana, I.K, and Reynolds, J.K. (2002). Audit-firm tenure and the quality of financial reports. Contemporary Accounting Research 19: 637-660. Lennox, C., and Pittman, J. A (2007). The importance of IRS monitoring to accounting fraud. Working paper, Hong Kong University of Science and Technology. Lennox, C. and Pittman, J.A. (2010), Big Five Audits and Accounting Fraud. Contemporary Accounting Research, Vol. 27, No. 1, pp. 209-247, March 2010. Maksimovic,V., and Titman, S. (1991). Financial policy and reputation for product quality. Review of Financial Studies 4 (1): 175–200. New York Stock Exchange. (2003). Final NYSE Corporate Governance Rules. Retrieved from http://www.nyse.com/pdfs/finalcorpgovrules.pdf O’Malley, S. (2002). Oversight Hearing on “Accounting and Investor Protection Issues Raised by Enron and Other Public Companies.” Senate Committee on Banking, Housing, and Urban Affairs. 107th Cong., 2nd sess. Top-down investment approach. Retrieved from http://www.investopedia.com/terms/t/topdowninvesting.asp#axzz1dEgF9OHm Vinod, K. (2002). Note on industry structure. Retrieved from http://info.umuc.edu/mba/public/AMBA607/IndustryStructure.html 19 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Appendix Table1: Table of Sample Firms from AAERs AAERs No. Firm Name State location Industry 2951 Allion Healthcare, Inc. NY Bituminous Coal & Lignite Mining 3348 Aon Corporation IL Crude Petroleum & Natural Gas 2972 Apogee Technology, Inc., MA Drilling Oil & Gas Wells 3242 ArthroCare Corporation TX Drilling Oil & Gas Wells 3109 Assurant, Inc. NY Drilling Oil & Gas Wells 3021 Avery Dennison Corporation CA Drilling Oil & Gas Wells 3069 Bancinsurance Corporation OH Drilling Oil & Gas Wells 2920 Cablevision Systems Corporation NY Oil & Gas Field Services, Nec 3063 China Holdings, Inc. CA Food And Kindred Products 3127 Collins & Aikman Corporation MI Converted Paper & Paperboard Prods 2982 CSK Auto Corporation AZ Industrial Inorganic Chemicals 3048 Dana Holding Corporation OH Agricultural Chemicals 2955 Delphi Corporation MI Fabricated Plate Work 3134 Diatect International Corp. UT Miscellaneous Fabricated Metal Products 3007 Doral Financial Corporation PR Industrial Trucks, Tractors, Trailors & Stackers 20 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES AAERs No. Firm Name State location Industry 3060 ECO2 Plastics, Inc. CA Pumps & Pumping Equipment 3036 Entrade, Inc. IL Computer & Office Equipment 3321 Escala Group, Inc. CA Computer Storage Devices 3108 General Re Corporation CT Computer Peripheral Equipment, Nec 3201 GlobalSantaFe Corp. TX Calculating & Accounting Machines 3283 GSI Group, Inc MA Electric Lighting & Wiring Equipment 3045 Hain Celestial Group, Inc. NY Telephone & Telegraph Apparatus 2935 Halliburton Company TX Radio & Tv Broadcasting & Communications Equipment 3026 Helmerich & Payne, Inc. OK Communications Equipment, Nec 2968 Ingram Micro Inc. CA Semiconductors & Related Devices 3254 International Business Machines Corporation NY Miscellaneous Electrical Machinery, Equipment & Supplies 3050 Isilon Systems, Inc. WA Miscellaneous Electrical Machinery, Equipment & Supplies 2934 ITT Corporation NY Motor Vehicles & Passenger Car Bodies 3268 Kentucky Energy, Inc. KY Motor Vehicle Parts & Accessories 2941 Krispy Kreme Doughnuts, Inc. NC Motor Vehicle Parts & Accessories 3297 LaBarge, Inc, MO Motor Vehicle Parts & Accessories 3213 LocatePlus Holdings Corporation MA Motor Homes 3015 LSB Industries, Inc. OK Search, Detection, Navagation, Guidance, Aeronautical Sys 21 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES AAERs No. Firm Name State location Industry 3236 Maxwell Technologies Inc. CA Measuring & Controlling Devices, Nec 3022 MedQuist Inc. NJ Surgical & Medical Instruments & Apparatus 3067 Merge Healthcare Incorporated IL Electromedical & Electrotherapeutic Apparatus 2970 Monster Worldwide, Inc. NY Water Transportation 3102 NATCO Group Inc. TX Airports, Flying Fields & Airport Terminal Services 3165 Navistar International Corporation IL Cable & Other Pay Television Services 3229 NIC Inc. KS Hazardous Waste Management 3206 Noble Corporation TX Wholesale-Computers & Peripheral Equipment & Software 3199 Office Depot, Inc. FL Wholesale-Jewelry, Watches, Precious Stones & Metals 2943 Pediatrix Medical Group, Inc. FL Wholesale-Drugs, Proprietaries & Druggists' Sundries 3203 Pride International, Inc. TX Wholesale-Farm Product Raw Materials 2949 Quest Software, Inc. CA Retail-Food Stores 3274 Rockwell Automation, Inc. WI Retail-Auto Dealers & Gasoline Stations 3068 SafeNet, Inc. MD Retail-Auto & Home Supply Stores 2963 Stratum Holdings, Inc. TX Retail-Miscellaneous Shopping Goods Stores 3189 Sunopta, Inc., ON Commercial Banks, Nec 3157 Sunrise Senior Living, Inc. VA Mortgage Bankers & Loan Correspondents 3064 Symbol Technologies, Inc. NY Accident & Health Insurance 22 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES AAERs No. Firm Name State location Industry 3047 Tenet Healthcare Corporation TX Hospital & Medical Service Plans 3035 Terex Corporation CT Fire, Marine & Casualty Insurance 3280 Thor Industries, Inc. OH Fire, Marine & Casualty Insurance 3207 Tidewater Inc. LA Insurance Agents, Brokers & Service 3202 Transocean Inc. TX Services-Help Supply Services 3154 Trident Microsystems, Inc. CA Services-Prepackaged Software 3187 True North Finance Corporation FL Services-Prepackaged Software 2995 Ulticom, Inc. NJ Services-Computer Integrated Systems Design 3093 UTStarcom, Inc. F4 Services-Computer Integrated Systems Design 3044 VeriFone Holdings, Inc. CA Services-Computer Processing & Data Preparation 3117 Verint Systems Inc. NY Services-Computer Processing & Data Preparation 3217 Vitesse Semiconductor Corporation CA Services-Nursing & Personal Care Facilities 3328 Watts Water Technologies, Inc MA Services-Hospitals 2971 WellCare Health Plans, Inc. FL Services-General Medical & Surgical Hospitals, Nec 3019 West Marine, Inc. CA Services-Management Consulting Services 23 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Table 2: Exhibit Violation Types Information of Each Sample Firms Company Name Allion Healthcare, Inc. Types of Violation 5,1,2 Aon Corporation 2,4,1 Apogee Technology, Inc. ArthroCare Corporation 1 2,1,5 It lacks internal control over sales. It materially overstated sales revenue. Assurant, Inc. 1 10,000,000 3,500,000 Avery Dennison Corporation Bancinsurance Corporation Cablevision Systems Corporation 4,2 It is an insurance company and improper booked $10 million payment as a bona fide reinsurance recovery. It materially overstated the net income that it reported for the quarter ended September 30, 2004 to the public and in Commission filings. Its subsidiary in China made illegal payment about $30,000 to foreign officials. It failed to accurately record these payments in books and records. It failed to account properly for more than $2 million of reinsurance claims 81,000 318,470 2,000,000 60,000 56,049,900 N/A China Holdings, Inc. 3 N/A N/A Collins & Aikman Corporation 2,1 It o overstated expenses in earlier fiscal periods, and understate expenses in later periods. It made improper prepays to its subsidiary. It made material misrepresentations in nine public filings in 2008 and 2009, including improper audit reports from current and former auditors. It inflated reported income between 2001 and 2004. It used false documents from suppliers designed to mislead its external auditors. 24 N/A 7,200,000 5, 2,4,5 Description It understated interest expense for the warrants in conformity with GAAP It overstated its net income and understated its loss per share in 2005. It failed to maintain an adequate system of accounting controls. It failed to maintain an adequate internal control system designed to detect and prevent the improper payments. Its subsidiaries made over $3.6 million in improper payments to foreign government officials between 1983 and 2007 to get favorable business treatment. It is a publicly traded company alleged to inflate earnings in 2003 and 2004. Amt of Fraud ($) 932,517 Penalty ($) N/A 3,600,000 1,764,000 200,000 35,000 N/A N/A AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Company Name CSK Auto Corporation Dana Holding Corporation Types of Violation 3 2,1,4,5, Delphi Corporation 4 Diatect International Corporation Doral Financial Corporation 5 ECO2 Plastics, Inc. 3 Entrade, Inc. 3,2 Escala Group, Inc. General Re Corporation 4,1 1,2 GlobalSantaFe Corporation GSI Group, Inc 2,4, Hain Celestial Group, Inc. 1,5,7, 2,1 1,2, Description It made material misrepresentations in 2009 in public filings. It improperly recognized revenue or income on several transactions and delayed recording expenses in the appropriate period from 2004 and mid-2005. It filed materially false and misleading periodic reports with SEC. It understated steel surcharge costs. Its deficient system of internal controls contributed to the restatement of its financial statements for the first two quarters of fiscal year 2005, fiscal year 2004 and prior years. It filed materially false and misleading financial statements in the company's 2001 Form 10-K. It improperly recorded a $20 million payment from an IT company in December 2001, made in connection with a new contract between the IT company and Delphi. It filed materially false and misleading financial statements. It overstated income by approximately $921 million or 100 percent on a pre-tax, cumulative basis between 2000 and 2004 by improperly accounting for the purported sale of non-conforming mortgage loans. $ 123 million to its investors harmed by accounting fraud. It has never registered a class of securities under the Exchange Act but has registered offerings of securities under the Securities Act of 1933. It did not maintain adequate books and records of liabilities arising from acquisition. It lacked a system of internal accounting controls designed to assure accurate transactions. It overstated $80 million to its revenues to boost its stock price in 2003. Its foreign subsidiary made sham transactions with AIG in 2000. It improperly recognized more than $200 million in revenues from 2000 to 2002. It made illegal payments to its customers brokers from January 2002 through July 2007. It improperly recognized revenue $7.8 million from 2004 to 2008. It has numerous deficiencies of internal controls that were attributable to its fraud. It backdated stock options granted to Company officers, directors, and employees, concealing millions of dollars in expenses from the Company's shareholders. 25 Amt of Fraud ($) N/A 43,000,000 Penalty ($) N/A N/A 20,000,000 30,000 N/A 216,281 921,000,000 123,000,00 0 N/A N/A N/A N/A 80,000,000 200,000,000 164,584 8,100,000 N/A 5,900,000 7,800,000 N/A 20.500,000 N/A AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Company Name Types of Violation Halliburton Company 2,6 Helmerich & Payne, Inc. Ingram Micro Inc. 2,4,5, International Business Machines Corporation 2,4,6, Isilon Systems, Inc. 1 ITT Corporation 1,2,4 Kentucky Energy, Inc. Krispy Kreme Doughnuts, Inc. LaBarge, Inc, 1,4, 1,2 LocatePlus Holdings Corporation LSB Industries, Inc. 1 Maxwell Technologies Inc. 4,1,2,6 MedQuist Inc. 1,2 1,4,5,2,8 5,1,2 1,5,8 Description It materially understated expenses and overstated its income in disclosures to the Commission and the investing public, and falsely represented in filings that Hain had incurred no expenses for option grants. It paid bribes to official within the Nigerian Government in to obtain the construction contracts. Its internal control failed to detect bribery. It made improper payment to its subsidiaries. It overstated revenues by $622 million from 1998 to 2000. It made illegal payments to its suppliers and take extraordinary sales discounts. It improperly recorded excess inventory fees. It subsidiaries paid cash bribes and provided improper gifts and payments of travel and entertainment expenses to various government officials in South Korea in order to secure the sale of IBM products. It cut secret side deals with Isilon customers to allow the company to report inflated sales to its shareholders. It misreported $4.8 million in improper revenue during 2006 and 2007. Its subsidiaries made illicit payments to generated sales and realized improper profits of more than $1 million. It accounted for warrants it had issued before and overstated its assets by 43%. It fraudulently inflated earnings in 2003. Its internal controls lapses and inaccurate records misstatement in fillings in 2006 and 2007. It fraudulently inflated revenue as well as a scheme to manipulate the stock of another company. It failed to comply with GAAP in connection with LSB’s change in inventory pricing methodology from LIFO to FIFO. Its subsidiary paid over $2.5 million in bribes to officials at several Chinese stateowned entities through a third-party sales agent for contracts that generated more than $15 million in revenues for Maxwell It inflated customer bills to increase revenues and profit margins 26 Amt of Fraud ($) Penalty ($) 6,000,000 177,000,00 0 185,673 375,681 622,000,000 15,000,000 N/A 2,000,000 4,800,000 N/A 4,000,000 1,678,650 13,000,000 528,323 N/A N/A 437,000 200,000 2,000,000 N/A 250,000 N/A 15,000,000 8,000,000 6,600,000 75,000 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Company Name Merge Healthcare Inc. Types of Violation 1,2,4 Monster Worldwide, Inc. NATCO Group Inc. 7 Navistar International Corporation NIC Inc. 5,1,2, , Noble Corporation 2,4, Office Depot, Inc. 2 Pediatrix Medical Group, Inc. 7,5 Pride International, Inc. 1,6 Quest Software, Inc. 1, 7 Rockwell Automation, Inc. 1,4 5,2,3,7 4 Description Its misstatements to the public, Merge’s stock price dropped from $24.50 to $7.30 per share, reflecting a $500 million loss in market capitalization. Its multi-year scheme to secretly backdate stock options granted to thousands of Monster officers, directors and employees. Its subsidiaries created and accepted false documents in filings. Its subsidiaries bribed Kazakstan’s officials to get contract interest. It overstated its pre-tax income by a total of approximately $137 million as the result of various instances of misconduct. It failed to disclose more than $1.18 million in perquisites to Fraser from at least 2002 to 2007. It failed to disclose its payment of $1 million to fly and operate planes. It made improper payments through its custom agents to officials of the Nigeria Customs Service to obtain permits and permit extensions necessary for operating offshore oil rigs in Nigeria. It violated fair disclosure regulations when selectively conveying to analysts and institutional investors that the company would not meet analysts' earnings estimates. It recognized approximately $30 million in funds received from vendors in exchange for the company's merchandising and marketing efforts. It backdated stock options grants to executives and employees and with reporting false financial information to shareholders. It illegally avoided expense for in-the-money options. It and its subsidiaries bribed government officials in Venezuela, India, Mexico, Kazakhstan, Nigeria, Saudi Arabia, the Republic of the Congo, and Libya. The bribery schemes allowed Pride and its subsidiaries to extend drilling contracts, obtain the release of drilling rigs and other equipment from customs officials, reduce customs duties, extend the temporary importation status of drilling rigs, lower various tax assessments, and obtain other improper benefits. It improperly granted undisclosed in-the-money stock options to executives and employees by backdating millions of options from 1999 through 2002. Its subsidiary made payment not directly related to business purposes for employees and customers. 27 Amt of Fraud ($) 500,000,000 Penalty ($) 870,000 399,500,000 2,500,000 80,000 N/A 137,000,000 1,049,503 1,800,000 500,000 N/A 5,576,998 30,000,000 1,000,000 8,800,000 N/A 2,500,000 23,529,718 113,600,000 150,584 1,700,000 400,000 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Company Name SafeNet, Inc. Types of Violation 7 Stratum Holdings, Inc. 3 Sunopta, Inc. 8, 5,1,2 Sunrise Senior Living, Inc. Symbol Technologies, Inc. 1 1 Tenet Healthcare Corporation 1 Terex Corporation 1 Thor Industries, Inc. 2,5,8 Tidewater, Inc. 2,4,5,6, Transocean, Inc. 1, 4, Trident Microsystems, Inc. 5,1,7 Description It engaged in a scheme to backdate option grants to senior executives and employees in order to take advantage of low points in the company's stock price, without recording the requisite compensation expense for these option grants. It failed to comply with Item 307 and 308T of Regulation S-B in its 10-KSB report filed in 2008. It failed to identify necessary downward adjustments to account for such inventory at its net realizable value and understated its cost. It made improper adjustments to its reserve for self-insured health and dental benefits and its accrual for corporate bonuses to meet public earnings forecasts. It engaged in a fraudulent scheme to inflate revenue, earnings and other measures of financial performance in order to create the false appearance that Symbol had met or exceeded its financial projections. It inflated its earnings by exploiting Medicare's outlier reimbursement regulations, which provided for additional reimbursement to hospitals to cover the additional costs for treating extraordinarily sick patients. It aided and abetted the fraudulent accounting by URI for two year-end transactions that were undertaken to allow URI to meet its earnings forecasts. These fraudulent transactions also allowed Terex to prematurely recognize revenue from its sales to URI. Its subsidiaries engaged in a fraudulent accounting scheme to understate Dutchmen’s cost of goods sold in order to avoid recognizing inventory costs that were not reflected in Dutchmen’s financial accounting system. It paid bribes to foreign government officials in Azerbaijan disguised as payments for legitimate services. It authorized improper payments to customs officials in Nigeria that were inaccurately recorded as legitimate expenses in the Company's books and records. It made illicit payments through its customs agents to Nigerian government officials to extend the temporary importation status of its drilling rigs, to obtain false paperwork associated with its drilling rigs, and obtain inward clearance authorizations for its rigs and a bond registration. It backdated stock option documentation to make it appear as if options had been granted on earlier dates, resulting in disguised "in-the-money" option grants to Company employees, officers, and on at least one occasion to directors. 28 Amt of Fraud ($) 1,600,000 Penalty ($) 1,000,000 N/A N/A N/A 46,200 N/A 50,000 3,091,539 250,000 11,000,000 2,000,000 N/A 8,000,000 27,000,000 1,900,000 1,600,000 217,000 10,243,056 7,265,080 37,000,000 350,000 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Company Name Types of Violation True North Finance Corporation Ulticom, Inc. 1 UTStarcom, Inc. 4,6 VeriFone Holdings, Inc. 1 Verint Systems, Inc. 1,2 Vitesse Semiconductor Corporation 1,5,7 Watts Water Technologies, Inc 1,2,4 WellCare Health Plans, Inc. 4,1 7 Description It engaged in a fraudulent and deceptive scheme to provide undisclosed compensation to executives and other employees, concealing millions of dollars in expenses from the Company's shareholders. It improperly recognized revenue on interest from borrowers which were not paying True North and which were in poor financial condition. It improperly recorded the grant dates of eight company-wide grants of employee stock options. It involved certain long-standing and improper accounting practices that were not in conformity with GAAP. It subsidiary paid nearly $7 million between 2002 and 2007 for hundreds of overseas trips by employees of Chinese government-controlled telecommunications companies that were customers of UTStarcom, purportedly to provide customer training. It made unsupportable alterations to its records to compensate for an unexpected decline in gross margins, overstating VeriFone’s operating income by a total of 129 percent. Its books and records falsely and inaccurately reflected, among other things, the Company's liabilities, expenses, net income, and general financial condition through at least the fiscal year ended January 31, 2005. It failed to maintain a system of internal accounting controls sufficient to provide assurances that its reserve activity was recorded as necessary to permit the proper preparation of financial statements in conformity with GAAP. It manipulated grant dates in order to award in-the-money options and failed to ensure that Vitesse properly recorded compensation expenses for the backdated grants. It compounded their fraudulent revenue recognition practices by failing to timely record credits related to the invalid accounts receivable that were generated by the distributor's return of product. Its subsidiary made improper payment to its employees in order to facilitate its sales. It fraudulently retained over $40 million it was required to return to Florida state agencies under programs that provided mental health services to Medicaid recipients and health care services to uninsured children. 29 Amt of Fraud ($) Penalty ($) 74,000,000 N/A 2,677,000 25,000 7,000,000 3,000,000 37,000,000 25,000 6,500,000 N/A 184,000,000 162,320 2,700,000 3,776,606 40,000,000 10,000,000 AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Company Name West Marine, Inc. Note: Types of Violation 1,8 1-Overstate Revenue; 2-Insufficient Internal Controls 3-Regulation Violation 4-Improper Payment Description It filed numerous false financial statements from 2004 to 2006 after making undisclosed accounting changes designed to offset an unexpected earnings shortfall. It improperly increased its pre-tax income for the year, offsetting the undisclosed reduction in earnings caused by the change in inventory valuation. 5-Undserstate Expense 6-Bribery 7-Backdated Stock Option 8-Inventory Misconduct 30 Amt of Fraud ($) 13,200,000 Penalty ($) N/A AN EMPIRICAL STUDY ON ACCOUNTING AND AUDITING ENFORCEMENT RELEASES CASES Table 3: Exhibit Penalty Percentage Impact on Dollar Amount of Fraud Name VeriFone Holdings, Inc. Vitesse Semiconductor Corporation Dollar Amount of Fraud ($) 37,000,000 184,000,000 Penalty ($) 25,000 162,320 Penalty as Percent of Fraud Amount 0.07% 0.09% Quest Software, Inc. 113,600,000 150,584 0.13% Delphi Corporation 20,000,000 30,000 0.15% 500,000,000 870,000 0.17% 80,000,000 164,584 0.21% Monster Worldwide, Inc. 399,500,000 2,500,000 0.63% Navistar International Corporation 137,000,000 1,049,503 0.77% Merge Healthcare Incorporated Escala Group, Inc. Ulticom, Inc. Trident Microsystems, Inc. MedQuist Inc. Ingram Micro Inc. Bancinsurance Corporation Office Depot, Inc. General Re Corporation Thor Industries, Inc. Symbol Technologies, Inc. Doral Financial Corporation Tidewater Inc. 2,677,000 25,000 0.93% 37,000,000 350,000 0.95% 6,600,000 75,000 1.14% 622,000,000 15,000,000 2.41% 2,000,000 60,000 3.00% 30,000,000 1,000,000 3.33% 200,000,000 8,100,000 4.05% 27,000,000 1,900,000 7.04% 3,091,539 250,000 8.09% 921,000,000 123,000,000 13.36% 1,600,000 217,000 13.56% 200,000 35,000 17.50% Apogee Technology, Inc., Tenet Healthcare Corporation 11,000,000 2,000,000 18.18% Rockwell Automation, Inc. 1,700,000 400,000 23.53% WellCare Health Plans, Inc. 40,000,000 10,000,000 25.00% Assurant, Inc. 10,000,000 3,500,000 35.00% ITT Corporation 4,000,000 1,678,650 41.97% NIC Inc. 1,180,000 500,000 42.37% UTStarcom, Inc. 7,000,000 3,000,000 42.86% 437,000 200,000 45.77% 15,000,000 8,000,000 53.33% 1,600,000 1,000,000 62.50% 10,243,056 7,265,080 70.93% 2,700,000 3,776,606 139.87% 185,673 375,681 202.33% 81,000 318,470 393.17% LaBarge, Inc, Maxwell Technologies Inc. SafeNet, Inc. Transocean Inc. Watts Water Technologies, Inc Helmerich & Payne, Inc. Avery Dennison Corporation 31