What is Economics?

advertisement

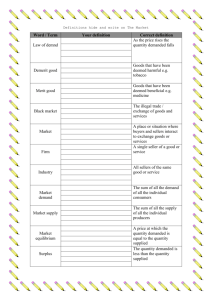

What is Economics? What is Economics? • Definition: study of how individuals & societies make choices about ways to use scarce resources to fulfill their wants Wants vs. Needs • Wants: anything other than what is needed for basic survival • Needs: things required for basic survival (Food, Clothing, Shelter) Wants vs. Needs • Example: In 1901, people discovered oil in Texas – but they were actually looking for water. Disappointed, they offered to trade the oil for water at a ratio of 1:1 (1 barrel of oil for each barrel of water). Problem of Scarcity • Scarcity is THE fundamental problem in economics • Maintains that all resources are limited • People will compete for these limited resources • Scarcity exists because people cannot satisfy their every want Factors of Production • Definition: what goes into producing a product • 4 Factors of Production: 1. Capital: previously manufactured goods used to make other goods & services 2. Entrepreneurship: ability of individuals to start new businesses & develop new products; Risktaker; lemonade stand example 3. Land: natural resources & surface land & water 4. Labor: human effort directed toward production 3 Basic Questions??? 1. What should be produced? – Always a Trade off – Ex. More $$$ on roads = less $$$ for salt in the winter 2. How should it be produced? – Always look for Profit Maximization – Ex. Jobs overseas, Pink slime 3. For whom should it be produced? – In the US we use a Price System – Can everyone afford a Ferrari? – NOT A CHANCE! Only high-rollers like Mr. Green Supply & Demand • Is what determines this price system • Demand: represents a consumer’s willingness and ability to pay; how we define this is with... • Law of Demand: As price goes up, quantity demanded goes down; as price goes down, quantity demanded goes up Supply & Demand • Factor effecting quantity demanded of a product: – Real Income: people are limited by income as to what they can buy; only a few that can afford a Ferrari – Substitution Effect: people can replace one product with another if it satisfies the same need – Diminishing Marginal Utility: how one’s additional satisfaction for a product lessens with each additional use/purchase of it Supply & Demand • Supply: willingness and ability of producers to provide goods and services • Law of Supply: As prices increase, the quantity supplied increases, as prices decrease, the quantity supplied decreases Supply & Demand • Factors Determining Supply: • Price of Inputs: how much it costs to produce the product • Number of firms in the industry: competition; more = more supply; less = less supply • Taxes: increase = reduction of supply (not making as much money off product) • Technology: increase can reduce cost of production and increase supply Putting Supply & Demand Together • Equilibrium Price: point at which quantity demanded & quantity supplied meet • Shortage: causes prices to rise, while a Surplus causes prices to drop…Why??? • Price Ceiling: prevents prices from going above a specified amount; Ex. Rent in NYC • Price Floor: prevents prices from dropping too low; Ex. Minimum wage