Personal Budget Spreadsheet

advertisement

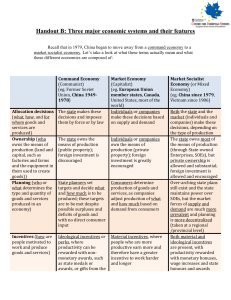

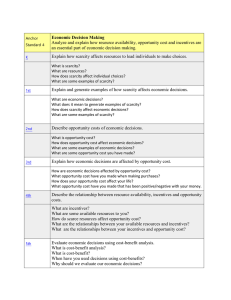

Seven Principals of Economics & Economic Systems Seven Principles of Economic Thinking 1. 2. 3. 4. 5. 6. 7. Scarcity forces trade-offs Costs versus benefits Thinking at the margin Incentives matter Trade makes people better off Markets coordinate trade Future consequences count Scarcity forces trade-offs Scarcity is most basic problem of economics It forces people to decide how to use limited resources to fill unlimited needs/wants Tradeoffs are what you give up to buy or do something else What was the scarcity forces tradeoff decision you made this morning? Costs vs. Benefits People only choose something when its expected costs are less than it expected benefits. Decisions require comparing costs and benefits of alternatives. Whether to buy Starbucks coffee instead of brewing their own coffee at home? Whether to go to college or to work? Whether to study or go out on a date? Whether to go to class or sleep in? Thinking at the margin Similar to costs vs. benefits you are looking at if one more unit of input improves/hurts my output Deciding whether to do or use one additional unit of some resource. Basically, it is an analysis to find the optimal return on actions. Should you study one more hour for this test or go to bed? Incentives matter People respond to incentives in generally predictable ways. There is evidence that people respond significantly to incentives even in situations where we do not usually imagine their behavior to be rational. Apparently psychologists have discovered by experiment that when you hand a person an unexpectedly hot cup of coffee, he typically drops the cup if he perceives it to be inexpensive but manages to hang on if he believes the cup is valuable. Why do you stand in line for hours at Christmas to buy newest video game or electronic device? Trade makes people better off We end up with more and better products by trading You trade your ham and cheese sandwich for a peanut butter and jelly sandwich. Suppose I am in the market for a new laptop computer. If I am permitted to trade freely with anyone in the world, I will choose the computer that best fits my preferences. What if that trade made someone lose their job at HP? Are both people involved in both situations happy? Markets coordinate trade Markets are defined as anything where buyers and sellers are brought together to do business with each other examples include flea markets, e-bay, stores, garage sales Buyers and sellers can trade with each other until both parties leave satisfied. This leads to the efficient use of market systems. Adam Smith made the observation that households and firms interacting in markets act as if guided by an “invisible hand.” Future consequences count Decisions made today have consequences in the future Law of unintended consequences occurs when a decision is made and the effects were not expected or the opposite of what was expected. Raising speed limit to 75 may “encourage” drivers to drive even faster. Economic goals Answers come from these goals and how they are ranked: Freedom – make own economic decisions Security – provide less fortunate members with basic needs Stability – goods/services we need are provided Equity – fair & just distribution of society's wealth Growth – improve standard of living Efficiency – makes most of resources (full employment) 3 Basic Economic Questions What are you going to make? Who are you making it for? How are you going to make it? Who answers the 3 questions? Traditional – based on customs, traditions, culture Command – government Highest goals are economic security & stability Main goal was economic stability & accumulation of wealth Market – millions of individuals acting independently Market Economies Also known as freemarket or capitalist What are the benefits of living in the United States? • Get to pick your own job • Competition • Choices Socialism & Communism Founded by Karl Marx & Friederich Engels Answer to working conditions in capitalist countries Socialism – society owns property Communism – final phase of socialism where government owns property and wealth and no classes are left Communism Economic planning – government planned all aspects of economy Did not allow for private ownership Led to shortages and/or few choices No incentives for workers to produce high quality goods/services Mixed Economies Most economies in world today are mixed – some government, some private How much government involvement depends on country In United States – it is limited in some areas and more involved in others • Child labor laws, OSHA • Competition, choice in market, private property Key Characteristics of Economic freedom Competition Equal Opportunity Binding contracts Property rights Profit motive Limited government