EBF.310 - Touro College

advertisement

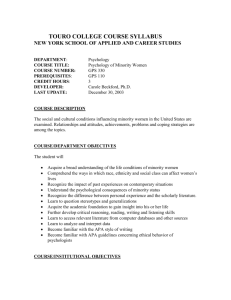

TOURO COLLEGE COURSE SYLLABUS DEPARTMENT: COURSE TITLE: COURSE NUMBER: PREREQUISITES: CREDIT HOURS: DEVELOPER: LAST UPDATE: Finance Security Analysis EBF 310 EBE 332 3 Meyer Peikes September 1, 2003 COURSE DESCRIPTION This course is a continuation of the introductory investments’ course. In this course we will probe deeply into the valuation methodologies employed by securities analysts. These include, but are not limited to, CAPM, dividends and earnings models, growth models, etc. The models will be applied to stocks, bonds and options. Portfolio analysis and the Markowitz approach will be dealt with in great detail. A hands-on, real world related perspective will be utilized throughout the course. Students are urged to read the appropriate text material, as detailed in the attachment, prior to class. In addition, daily readership of the financial section of The New York Times or the Wall Street Journal is encouraged. A mid-term and final will each count toward half of the final grade. It is strongly recommended that students bring a financial calculator to class, and participate in class discussions. Homework problems will be continuously assigned to measure the comprehension of the students and the degree of absorption of the lecture materials. COURSE / DEPARTMENTAL OBJECTIVES In this course the student will: Learn many methods and approaches to valuation Learn how to evaluate information Techniques of portfolio construction How to analyze portfolio performance Do a hands on project putting many of the ideas of the course to practical use Learn how many important measures are calculated About innovation & creativity in the financial world COURSE/ INSTITUTIONAL OBJECTIVES This course is intended to develop students’ quantitative skills in evaluative investments. It will further their professional career interests in finance by seeing up close what securities analysts really do and how to do it. The research project will enhance the students writing & communication skills in addition to enhancing their research abilities. COURSE CONTENT: Topic I. Introduction II. Value and Price 1) Supply, demand and equilibrium 2) Effect of short sales 3) Market efficiency III. Risk free securities 1) Nominal and real rates of return 2) Spot rates and forward rates 3) Yield curves 4) Duration 5) Theories of term structure IV. Risky securities 1) The insurance approach 2) State preference approach and complete markets 3) Probabilistic forecasting 4) Expected (holding period) return V. Portfolio analysis and selection 1) Measures of return and risk 2) Two-security portfolio analysis 3) Non satiation and risk-aversion 4) Efficient portfolios and investment selection Midterm VI. CAPM 1) Capital market line 2) Security market line 3) The market model 4) Unique, market and total risk VII. Bonds 1) 2) 3) 4) 5) Yield spreads and arbitrage Coupon rates and time to maturity Immunization and duration Promised ytm and default premiums Bond theorems 6) Bond swaps VIII. Common stock valuation 1) Dividends and valuation models 2) Growth models 3) Informational content of dividends 4) Other valuation models and approaches IX. Options 1) Calls and puts 2) Profit-loss diagrams 3) Value boundaries 4) Binomial model 5) Black-Scholes formula 6) Portfolio insurance X. Investment companies 1) Mutual funds 2) Evaluation techniques 3) Performance-risk analysis XI. APT 1) Factor models 2) Arbitrage portfolios 3) Synthesis of APT and CAPM HARDWARE/ SOFTWARE/ MATERIALS REQUIREMENT Students are strongly recommended to read the Wall Street Journal (daily) & Barron’s (weekly). Software is utilized for the evaluation portion of the term project. COURSE REQUIREMENTS Students are strongly urged to try to read the appropriate text material of the topic that will be covered in class, beforehand. In addition, all students are required to keep current on all relevant financial current events by reading the Wall Street Journal daily. Student subscription rates will be made available in order to ease the financial burden of this requirement. References to specific articles will be made in class. It is highly recommended that students attend all classes and participate in class discussions. Class participation will be used to “fine tune” the final grade. Homework problems will be assigned continuously. The possession of a scientific or financial calculator will prove to be a valuable aid in problem solving. GRADE GUIDELINES Midterm Examination 35% Final Examination Term Project 35% 30% METHODOLOGY Lectures combined with comprehensive homework exercises are utilized to get the material across to the students. In addition a term project in which there is continuous analysis of a firm and its underlying security is essential to the learning process. COURSE TEXT Title: Author: Pub. Date: Publisher: ISBN: Investments W. Sharpe, G. Alexander. & J. Bailey 1999 Prentice Hall 0-13-010130-3 BIBLIOGRAPHY: Value & Price Title: Author: Pub. Date: Publisher: Constraints on Short-Selling and Asset Price Adjustment to Private Information Douglas Diamond & Robert Verrecchia June 1987 Journal of Financial Economics 18, no. (2 pg. 277-311) Title: Author: Pub. Date: Publisher: Efficient Capital Market: A Review of Theory and Empirical Work Engere F. Fama May 1970 Journal of Finance 25, no. 5 (pg. 383-417) Title: Author: Pub. Date: Publisher: Efficient Capital Market II Engere F. Fama December 1991 Journal of Finance 46, no. 5 (pg. 1575-1617) Risk-Free Securities Title: Author: Pub. Date: Publisher: About the Term Structure of Interest Rates Mark Kritzman July/ August 1993 Financial Analysts Journal, no. 4 (pg. 14-18) Title: Author: Pub. Date: Understanding the Term Structure of Interest Rates: The Expectations Theory Steven Russell Federal Reserve Bank of St. Louis, Review 74, no. 4 (pg. 36-50) Risky Securities & Portfolio Analysis Title: Author: Pub. Date: Publisher: Portfolio Selection Harry Markowitz March 1952 Journal of Finance 7, no.1 (pg. 77-91) Title: Author: Pub. Date: Publisher: Measuring Investment Risk: A Review Leslie Balzer Fall 1995 Journal of Investing 4, no. 3 (pg 5-16) Title: Author: Pub. Date: Publisher: A Simplified Model for Portfolio Analysis William Sharle January 1963 Management Science 9, no. 2 (pg. 277-293) Title: Author: Pub. Date: Publisher: The Minimum Number of Stocks Needed for Diversification Gerald Newbould & Percy Poon Fall 1993 Financial Practice and Education 3, no. 2 (pg. 85-87) Title: Author: Pub. Date: Publisher: Portfolio Optimization in Practice Philippe Jorion January/ February 1992 Financial Analysts Journal 48, no.1 (pg. 68-74) Title: Author: Pub. Date: Publisher: Portfolio Selection Based on Return, Risk and Relative Performance George Chow March/ April 1995 Financial Analysts Journal 51.no.2 (pg. 54-60) CAPM Title: Author: Pub. Date: Publisher: Capital Asset Prices: A Theory of Market Equilibrium Under Conditions of Risk William Sharle September 1964 Journal of Finance 19, no.3 (pg. 425-442) Title: Author: Pub. Date: Publisher: Securities Prices, Risk and Maximal Gains From Diversification John Lintner December 1965 Journal of Finance 20, no.4 (pg. 587-615) Title: Author: Pub. Date: Publisher: Risk, Return and Equilibrium: Some Clarifying Comments Engere Fama March 1968 Journal of Finance 23, no.1 (pg. 29-40) Title: Author: Pub. Date: Publisher: The CAPM is Granted Dead or Alive Engere Fama December 1996 Journal of Finance 51, no. 5 (pg. 1947-1958) Bonds Title: Author: Pub. Date: Publisher: The Credit Rating Industry Richard Cantor December 1995 Journal of Fixed Income 5, no. 3 (pg. 10-34) Title: Author: Pub. Date: Publisher: The Effect of Bond- Rating Changes on Bond Price Performance Gailen Hite & Arthur Waga May/ June 1997 Financial Analysts Journal 53, no. 3 (pg. 35-51) Title: Author: Pub. Date: Publisher: Ganging the Default Premium Rye Gordon January/ February 1974 Financial Analysts Journal 30, no. 1 (pg. 49-52) Title: Author: Pub. Date: Publisher: Determinants of Risk Premiums on Corporate Bonds Lawrence Fisher June 1959 Journal of Political Economy 67, no. 3 (pg. 217-237) Title: Author: Pub. Date: Publisher: Ratio Stability and Corporate Failure Ismael Dam Bolena & Sarkis Khoury September 1980 Journal of Finance 35, no. 4 (pg. 1017-1026) Title: Author: Pub. Date: Publisher: How to Immunize a Bond Investment Charles H. Gushee March/ April 1981 Financial Analysts Journal 37, no.2 (pg. 44-51) Stocks Title: Author: Pub. Date: Publisher: Dividend Earnings & Stock Prices M. J. Gordon May 1959 Review of Economics and Statistics 41, no.2 (pg. 99-105) Title: Author: Pub. Date: Publisher: Industry Costs of Equity Fama, Engere & Kenneth French February 1997 Journal of Financial Economics 43, no. 2 (pg. 153-193) Title: Author: Pub. Date: Publisher: Price Earning Ratios and Fundamental Stock Valuation Bajikowski, John July 1991 AAII Journal 13, no.6 (pg. 33-36) Title: Author: Pub. Date: Publisher: The Response of Stock Prices to Permanent and Temporary Stocks to Dividends Lee, Bong-Soo March 1995 Journal of Financial and Quantitative Analysis 30, no. 1 (pg. 1-22) Title: Author: Pub. Date: Publisher: Dividend Policy, Growth, and the Valuation of Shares Miller, Merton & Franco Modigliani October 1961 Journal of Business 34, no. 4 (pg. 411-433) Title: Distribution of Incomes of Corporations Among Dividends, Retained Earnings and Taxes Lintner, John May 1956 American Economic Review 46, no. 2 (pg. 97-113) Author: Pub. Date: Publisher: Options Title; Author: Pub. Date: Publisher: Simplifying Portfolio Insurance Black, Fisher & Robert Jones Spring 1988 Journal of Portfolio Management 14, no. 3 (pg. 48-54) Title: Author: Pub. Date: Publisher: The Pricing of Options and Corporate Liabilities Black, Fisher & Myron Scholes May/ June 1973 Journal of Political Economy 81, no. 3 (pg. 639-654) Investment Companies Title: Author: Pub. Date: Publisher: Returns from Investing in Equity Mutual Funds Malkiel, Burton June 1995 Journal of Finance 50, no. 2 (pg. 549-572) Title: Author: Pub. Date: Publisher: On Persistence in Mutual Fund Performance Carlart, Mark March 1997 Journal of Finance 51, no. 1 (pg. 57-82) Title: Author: Pub. Date: Publisher: Morning Star’s Risk- Adjusted Ratings Sharre, William July/ August 1998 Financial Analysts Journal 54, no. 2 (pg. 21-33) APT Title: Author: Pub. Date: Publisher: The Arbitrage Theory of Capital Asset Pricing Ross, Stephen December 1976 Journal of Economic Theory 13, no. 3 (pg. 341-360) Title: Author: Pub. Date: Publisher: Some Results in the Theory of Arbitrage Pricing Ingersoll, Jonathan September 1984 Journal of Finance, no. 4 (pg. 1021-1039) Title: Author: Pub. Date: Publisher: Portfolio Management Grinold, Richard 1995 Chicago: Probus (Chapter 7) Title: Author: Pub. Date: Publisher: The Number of Factors in Security Returns Brown, Stephen December 1989 Journal of Finance 44, no. 5 (pg. 1247-1262)