FDIC Money Smart-Financial Education Curriculum Writing a Check

advertisement

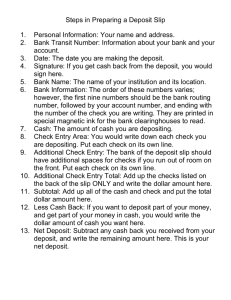

FINANCIAL EDUCATION MATERIALS 1 Financial Education Course Outline 1. Financial Basics 2. Introduction to Checking 3. Budgeting 4. Setting Financial Goals/Importance of Savings 2 SECTION 1 Banking Basics Learn the Nuts & Bolts Brief introduction on banking basics I. II. III. IV. Identify five reasons to use a financial institution. Describe the steps involved in opening an account. Describe two types of deposit accounts. Identify additional financial services that come with deposit accounts. 3 Brief introduction on financial basics A. Identify five reasons to use a financial institution. 1. Safety 2. Convenience 3. Cost 4. Security 5. Financial Future – Building a relationship with a bank will establish a record of paying bills, can help you save money, and is necessary for getting a loan B. Describe the steps involved in opening a bank account. 1. Before opening an account, most financial institutions will review your history of using checking accounts through companies such as TeleCheck or ChexSystems. Some financial institutions will run a full credit report to determine the level of risk. If you have a history of bouncing checks or misusing your accounts, financial institutions might not open an account for you. 2. The institution will need your photo identification, usually a driver’s license, and your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITN) to verify the information. 3. If you are not a citizen of the U.S., some financial institutions may accept other forms of photo identification. Other types of identification may include the matricula consular card, resident alien card (Green Card), or passport. C. Describe two types of deposit accounts. 1. Checking Account – Customers can deposit and withdraw money in this account. These can also be used to write checks for goods and services 2. Savings Account – Customers can deposit money into a savings account to earn interest and use for large purchases or other savings goals D. Identify additional financial institution services that come with deposit accounts 1. Direct Deposit of payroll checks 2. Money Orders 3. Loans 4 Section 2 Introduction to Checking 5 Writing a Check Writing checks is easy, after you have some practice. Make sure to always use a pen and write neatly. Don’t forget the #1 rule…Only write checks when you have enough money in your account. Every time you write a check, you’ll fill in these six spots: 1. Date: Write in the day you are filling out the check. 2. Pay to the Order of: Write in the name of the person(s) or place to whom you are writing the check. 3. $ Amount: Write the amount the check is for in numbers. When you write the number, start at the left and don’t leave space. People could add in more numbers if you don’t. 4. Dollars: Write, in words, how much the check is for. When you write the words for the dollars, starts at the left side. Write any cents as a fraction. Draw a line through the extra space. 5. Signature: Sign your name here, just like it is on the top of the check. Don’t sign it until you use it. If you sign it ahead of time, someone else could use the check. 6. Memo: Indicate what the check payment is for. Now your check is complete. Don’t forget to enter it into your check register. 2004 Consumer Debit Resource 6 How to Keep Track of Your Money The way you keep track of your money when you have a checking account is by using a check register. This is where you write down everything you do with your account. Whenever you deposit money or withdraw money, write it down in the check register immediately. This is called recording a transaction. Let’s take a look at a check register and how it works. 1. Number: This is the check number. You’ll find it in the upper right hand corner of each check. Every check has a different number. 2. Date: Write in the date of the transaction. 3. Description of Transaction: This tells what you did. Did you deposit money? Did you write a check? Use the Automated Teller Machine (ATM)? Make a telephone transfer? Describe your transaction here. 4. Payment/Debit: This is the amount of the check or how much the withdrawal is for. 5. Code for Transaction: This is where you fill in a code for transactions you make when you aren’t writing a check. When you get your statement, every month you’ll place a “” through this box if you see the transaction listed. 6. Service Fee: If your financial institution charges you money to write each check, or to withdraw money from the ATM, write that fee in this space. 7. Deposit / Credit: Did you deposit money into your account? Write down the amount here. 8. Balance: To find out how much money you have, add the deposited money to what you had before. Or subtract the withdrawal amount from what you had before. The money left is your balance. Note: When you write a check, withdraw money from the ATM, or deposit money into your account, write it down right away. It’s easy to forget if you wait. This is a completed register. Note the different types of entries. Next you’ll learn how to fill out a deposit ticket. 2004 Consumer Debit Resource 7 Deposit Money When you’re ready to deposit money at your financial institution, you need to fill out a form called a deposit ticket. You’ll find your deposit tickets in your checkbook, behind the checks. Just like checks and check registers, there are spots you need to fill in. It is very important that you use a pen and that you write neatly. 1. Date: The day you are depositing money. 2. Cash: The amount of cash you are depositing. Put each check on its own line. 3. Check Entry Area: This is where you write down each check you’re depositing. Put each check on its own line. 4. Additional Check Entry Area: The back also has space for checks, if you run out of room on the front. 5. Total From Other Side: If you have more than three checks and wrote them down on the back side, add them up and put the total here. If you are depositing three checks, this is the place you write down the third one. 6. Sub Total: Add all the cash and check amounts together and enter amount here. 7. Less Cash Received: If you want to deposit part of the money and get part of the money in cash, write down how much you want given back to you in cash. 8. Sign Here: If you want cash back, you need to sign your name here. 9. Net Deposit: Add all the cash and all the checks together. If you are getting any cash back, subtract that. The amount left is your net deposit. Write down that amount here. Note: You will get a receipt for your deposit. Keep receipts until you receive your monthly statement. 2004 Consumer Debit Resource 8 Here is your completed deposit ticket. Did you remember to endorse your checks? Next, you’ll see the different types of endorsements. Front 2004 Consumer Debit Resource 9 Endorse a Check To deposit a check, you need to endorse it. That means you sign your name in ink on the back of the check. You must sign your name the same way it’s written on the check. If your name is spelled wrong, also sign your name the correct way on the next line. There are a few ways to endorse your check. 1. Blank Endorsement: Sign your name the same way it’s written on the front of the check. Make certain to sign it only when you’re ready to cash it or deposit the money into your account. Once the check is signed on the back (endorsed), if you lose it, someone else could get your money. 2. Special Endorsement: Do this when you want to give someone else the money. Write “Pay To The Order Of “ and that person’s name below it. Then, sign your name underneath. Now, that person is the only one who can cash the check. 3. Restrictive Endorsement: When you want your check to be very safe, like when you send it to your financial institution in the mail, use this kind of endorsement. Write “For Deposit Only” and sign underneath. Now, the check can only be deposited into your account and not cashed. 2004 Consumer Debit Resource 10 Monthly Statement Every month, you’ll get a statement from your financial institution. Here are the different sections: 1. Return Address: This is where your financial institution sends your statement from. 2. Account Information: Here is where you will find your personal information, like the type of account you have, account number and social security number. 3. Deposits: This is where your deposits are listed. You’ll see the date and the amount of money you deposited. 4. Checks and Deductions: These are all the checks you wrote for the month that have been processed. You’ll see the date, the check number, and the amount you wrote the check for. If you see dots or stars between the check numbers, that means either you are missing a check, or that the check is outstanding. You’ll also find your ATM and other withdrawals here. 5. Daily Balances: You’ll see dates listed and how much money was in your account on that day. 6. Ending Balance: Here is a summary of your account for the month, you’ll see how much money you started with, how many withdrawals you made, how much money you deposited, and how much money you have left in your account. 7. Customer Service Number: This is the phone number you can call if you have any questions about your account or your statement. Remember, if there is something you don’t understand about your account, call the number you see on your statement to get your questions answered by your financial institution’s customer service department. Please remember that the style of statements for each financial institution may vary slightly, but typically contain the same information. 2004 Consumer Debit Resource 11 2004 Consumer Debit Resource 12 Balance Your Checkbook In this section, we’ll cover how to balance, or reconcile, your account. That just means you’ll see how much you deposited into your account, how much you spent, and how much you have left. To balance your account, look at your check register and your statement together and compare them. Here’s how to start: 1. If your financial institution returns your checks to you, put them in order according to the check number. 2. Look at the statement; find the first check number listed. 3. Look at your check register. Find that same check number and place a check mark in the column labeled “Code”. Do this for every check on your statement. If you see checks in your check register that are not listed on the statement, they have not cleared the financial institution yet. Don’t check them off. They will be listed on a future statement. 4. Now, just like you did with the checks look at the statement again and find the first deposit listed. Now, look at your check register and place a check mark in the column labeled “Code” for every deposit on your statement. 5. Look to see if you have any other service fees or charges for checks, ATM withdrawals, financial institution services, or automatic deductions (a car loan, for example) listed on your statement. Also, check to see if your financial institution pays interest on your checking account, the interest amount must be added to your check register. 6. Enter the fee or interest amounts in your checks register. Don’t forget to add or subtract these amounts from your balance. Now, your checkbook should be up-to-date. Most of the time, your checkbook balance and the statement won’t match. That is normal. This happens because of those outstanding checks we discussed earlier and any deposits that you made after the statement was printed. 2004 Consumer Debit Resource 13 7. Next, go to the reconciliation form usually on the back of the statement. This is a form to help you balance your account. Just like all the other forms we’ve talked about, there are spots for you to fill in. 8. List deposits, checks, and other withdrawals that you have written in your check register but are not listed on the statement in proper columns. 9. Write down the total of the deposit list and the checks/withdrawals list. 10. Write down the ending balance printed on the front of your statement. 11. Enter the total deposits from line 2. Add lines 3 and 4. Enter on subtotal line. 12. Enter the total withdrawals from line 2 and subtract from subtotal. 13. Now, the balance of your checkbook should match the ending balance on your reconciliation form. If the amounts match, you’re done! 2004 Consumer Debit Resource 14 If the amounts do not match, calculate the difference. Review your statement and check register to see if there is an item of the same amount that may have been missed or double counted. If you still don’t match, go back to where you balanced last month, and use a calculator to check your adding and subtracting. If you still have trouble reconciling your account, just call the customer service number listed on your statement for assistance. 2004 Consumer Debit Resource 15 Sample Check Complete the following areas when writing a check: 1. Date: Be sure to write the complete date, including the month, day, and year; for example, February 26, 20_ _. 2. Pay to the Order of: This is where you write the name of the person or company to whom you will give the check. After writing the name, you can draw a line to the end of the space. This prevents anyone from adding an additional name on your check. 3. $: Write the dollar amount of the check in numbers, for example, $19.75. 4. Dollars: Write the dollar amount of the check in words, for example, “Nineteen and 75/100.” After writing out the amount of the check, draw a line to the end. This prevents anyone from adding an additional amount after what you have written. 5. Memo: Writing in this area is optional. You can use it to remind yourself of the reason you wrote the check or to record the account number of the bill you are paying. 6. Signature Line: Sign your name here. Check Writing Tips Write in blue or black ink. Write clearly. Remember to record each check you write in your check register. If you make a small mistake, such as starting to write the dollar amount in the “Pay to the Order of” area, cross out the incorrect information and write your initials above what you crossed out. Then, write the correct information. Some stores will not accepts checks with crossed out information. If you make a large mistake, write “VOID” across the check or tear it up. A check with VOID across it is no longer usable. FDIC Money Smart-Financial Education Curriculum 16 Writing a Check Scenario On February 26, 20XX, you decide you want to buy a coffeemaker from a store called Coffee Mart. The coffeemaker costs $19.75, including tax. Instructions Take a look at your Practice Check Register. Do you have enough money in your checking account to write a check for this coffeemaker? _____________ Fill in the check below to record your purchase of the coffeemaker. When the instructor tells you to do so, record this information in your check register: Check #: 101 (preprinted) Date: 2/26/20XX Description of Transaction: Coffee Mart Payment/Debit ( - ): $19.75 Balance: $_________ FDIC Money Smart-Financial Education Curriculum 17 Practice Check Register Check Number Date 1/15 Description of Transaction Beginning Balance Payment/Debit (-) Fee Deposit/Credit (+) Balance 50 00 FDIC Money Smart-Financial Education Curriculum 18 Good Advice to Prevent ID Theft 1. Order checks from your financial institution. Many financial institutions offer a variety of checks including specialty checks. An independent company may not offer proper protections to secure your account information. DO NOT print your driver’s license number, unlisted phone number, social security number, or date of birth on your checks. 2. Sign the back of your credit cards. Also include, “PHOTO ID REQUIRED". 3. Utilize online bill pay through your financial institution to avoid mailing checks from home. 4. If mailing check payments from home, avoid placing the full account number on the memo line. Instead, write the last four digits of the account number (----1234). The credit card company can track the rest of the number using your name and address, which is printed on the check. 5. If you have a PO Box use that instead of your home address. 6. Do not leave your purse or wallet in the car out in plain view or in an unattended shopping cart. Doing so can encourage theft. 7. Lock your valuables at home in a safe, drawer, cabinet, etc. Consider unused credit cards and checks as valuables. 8. Don’t give out personal information over the telephone, Internet, or through the mail unless you have initiated contact and know who you are dealing with. Call anyone back using a phone number found in the Yellow Pages or an online directory assistance service. 9. Use a cross-cut shredder before putting any personal information in the trash. This includes old credit and debit cards, pre-approved credit applications, and anything with your social security number listed. 10. Don’t throw away pill bottles with the RX information on the bottle. permanent black marker to block the name and RX number. Use a 11. Verify the accuracy of your all account, credit card, and and/or billing statements. Make sure that no one has accessed your accounts and that all transactions are YOURS! 12. Update firewalls on home computers regularly. There are free firewalls available. ALWAYS REMEMBER IF IT SOUNDS TOO GOOD TO BE TRUE… IT IS! 19 Availability of Funds in Your Deposit Account Each bank has its own specific rules as to when you can have access to funds you deposit into your account based of various rules, however there is a federal regulation called regulation CC that they must use as a guide for designing their policies. When you open a deposit account ask your banker to review the specific regulation CC rules with you for their bank which will be listed in the deposit account agreement they are required to give you. In most cases when you make a deposit with a payroll check or other type of check those funds are not available for you to withdraw or spend with a check, debit card, ATM card or any other means for at least 1 to 2 days. The reason for that is the bank must send the check to the bank the check was written on to receive their payment for the check. Some banks may not allow use of cash deposits for 1 day also. Deposits into an ATM machine are often delayed by 1 day so the bank has time to verify the deposit. If you spend this money before it is available you will be charged on overdraft fee. Longer delays may apply for checks totaling more than $5,000 on any one day, suspicious checks, or checks which bounced the first time and you are redepositing them. If you repeatedly overdraw your account the bank also has the right to delay your availability of a deposit. There are also special rules that can apply to an account that has been opened for less than 30 days. In each of these cases the bank must specifically notify you that a longer delay will apply to your deposit, note that they do not specifically notify you of the standard availability schedule except by the original rules given to you at account opening. NOTE THAT MOST FINANCIAL INSTITUTIONS GIVE YOU IMMEDIATE AVAILABILITY TO YOUR FUNDS IF THEY ARE ELECTRONICALLY DEPOSITED INTO YOUR BANK ACCOUNT BY MEANS OF A DIRECT DEPOSIT FROM YOUR EMPLOYER OR GOVERNMENT PAYMENT. It is to your advantage to sign up with your employer to have your payroll direct deposited into your deposit account. Not only does this give you quicker availability to your funds but it is safer as it eliminates the risk that someone steals your check or that it is lost. Talk to your banker when you open up your account and they can give you advice on having this set up. 20 Section 3 Budgeting 21 How To Prepare a Budget Step 1: Track daily spending. Step 2: Determine income and expenses. Step 3: Find ways to decrease spending. Step 4: Find ways to increase income. If you want to be in control of your money, it is critical that you understand where your money goes. One way to do this is to keep a spending diary to record everything you spend. You can use this information to track your spending over a period of time, say a month, so that you can see how you are spending your money. FDIC Money Smart-Financial Education Curriculum 22 Daily Spending Diary Day What did I spend my money on today? Sunday Monday Tuesday Wednesday Thursday Friday Saturday FDIC Money Smart-Financial Education Curriculum 23 Monthly Income and Expense Worksheet My Income My Expenses Fixed Expenses Wages $__________ Public Assistance $__________ Child Support/ Alimony $__________ Interest/Dividends $__________ Social Security $__________ Advanced Earned Income Credit $__________ Other $__________ Rent/Mortgage $________ Property Taxes/Insurance $________ Trash Collection $________ Cable $________ Car Payment $________ Car Insurance $________ Other loan payments $________ Health Insurance $________ Day care/Elder care $________ Flexible Expenses Total Income $________ Savings $________ Gas/Oil $________ Electricity $________ Water $________ Telephone/Cell Phone $________ Food $________ Transportation/Gas $________ Car maintenance $________ Education $________ Personal expenses $________ Charity/Donations $________ _______________ $________ _______________ $________ Total Expenses $________ * Remember to plan for income and expenses that do not occur on a monthly basis. FDIC Money Smart-Financial Education Curriculum 24 Tips to Help You Decrease Spending or Save More Money Carry only small amounts of cash in your wallet so you will not spend it. Use direct deposit for your paycheck or federal benefits, such as Social Security (see “Myths and Facts about Direct Deposit” on the next page). Control your use of credit cards. Do not go shopping just for fun. Take your written savings goals with you as a reminder. Buy only what you need-do not buy things just because they are on sale. Use coupons to save money. Use a grocery-shopping list to prevent impulse buying. Take your lunch to work instead of eating out. Shop around to get the best deal on big-ticket items like cars and appliances. Pay your bills on time to avoid late fees, extra finance charges, utilities being turned off, eviction, repossessions, and the costs of a bad credit rating. FDIC Money Smart-Financial Education Curriculum 25 Other Budgeting Tools Here are a few other budgeting tools you can use at home. Use the one with which you are most comfortable. Expense Envelope System This tool is useful if you pay your bills in cash each month. Make an envelope for each expense category, such as rent, gas, electricity, and food. Label the envelope with the name of the category, the amount, and the due date. When you receive income, divide it into the amounts to cover the expenses listed on the envelopes. Pay bills right away so you won’t be tempted to spend the money on something else. Budget Box System The budget box is a small box with dividers for each day of the month. When you receive a bill, check the due date and place it behind the divider that represents the bill’s due date. As you receive income, pay all bills that are due. Computer System If you have access to a personal computer, you can create your own spreadsheet. You may also want to purchase a personal finance program. They are available for less than $75. Using a computer to manage your finances is relatively simple. Once you set up the system, updating information is quick and easy. It is important to enter transactions frequently to truly understand your financial position. FDIC Money Smart-Financial Education Curriculum 26 Section 4 Setting Financial Goals/Importance of Savings 27 Goal Setting Success Guide Financial Goal Setting - Four Steps There are no hard and fast rules for implementing a financial goal setting plan. The important thing is to at least do something as opposed to nothing, and to start NOW. Here are four steps you can apply to any financial goal setting exercise: Step 1: Identify and write down your financial goals, whether they are saving to send your kids to college or University, buying a new car, saving for a down payment on a house, going on vacation, paying off credit card debt, or planning for you and your spouse’s retirement. Step 2: Break each financial goal down into several short-term (less than 1 year), medium-term (1 to 3 years) and long-term (5 years or more) goals, which will make this process easier. Step 3: Educate yourself and do your research. Read Money magazine or a book about investing, or surf the Internet's investment Web sites. Step 4: Evaluate your progress as often as needed. Review your progress monthly, quarterly, or at any other interval you feel comfortable with, but at least semi-annually, to determine if your program is working. If you're not making a satisfactory amount of progress on a particular goal, re-evaluate your approach and make changes as necessary. Sometimes when people write down their goals, they discover that some of the goals are too broad in meaning and nearly impossible to reach, while others may seem smaller in scope and easier to achieve. Break your goals down into three separate time categories. By placing a time frame on your goals you are motivating yourself to get started and helping to allow you the chance to succeed. Just remember that you can adjust the time frame whenever you want to. Long-term goals (over 5 years) are those things that won't happen overnight, no matter how hard you work to achieve them. They make take a long time to accomplish (hence the reason they are called long term goals), so give yourself a reasonable amount of time, that are based on your best estimates of what it will take to achieve them. Examples of long-term goals might include college education for a child, retirement plan or purchasing a home. Whatever the case, these goals generally require longer commitments and often more money in the end. 28 Website – About-Goal-Setting Intermediate-term goals (1 - 5 years) are the type of goals that can't be executed overnight but might not take many years to accomplish. Examples might include purchasing/replacing a car, getting an education or certification, or paying off your debts like credit cards etc. (depending on the amount). Short-term goals (within one year) generally take one year or less to achieve, based on the date the task is needed, the total estimated cost, and the required savings. What are your goals? To find out, you need to make up a list, decide which timeline your goal fits into, detail the steps necessary to achieve your goals, then take action toward reaching those goals. It’s that simple. You might be wondering where to start with your financial goal plan. These are some basic tips to help you in making the best choices for you. After looking at these tips, it is best for you to go out and do some research to find the method(s) that suit you best. Begin by taking 5%-10% out of each pay check and put it in a savings account. Look into different investment strategies such as IRA’s, stocks, RRSP’s, Mutual Funds, personal investments, etc. There are many more and all can assist you in short and long term goals. Start making a budget for yourself that leaves you with some extra money and follow it. Use your coupons that is why they are there. It seems like small savings, but add together you could save $20 to $30 at each trip to the market. Shop around for bargains. Do not live outside of your means. Work with a credit counselor to get help in lowering your monthly expenses and get rid of your debt. These are just some of the things that you can do when beginning your financial goal setting plan. The steps to setting goals successfully don’t change, only the methods that you use to go about it. For example, when it is career wise, work to get noticed; for relationships, work on maintaining your intimacy or getting it back; in financial goal setting, work to save and invest money. It really is that easy. Website – About-Goal-Setting 29 Saving Tips 1. Consider needs versus wants. Think about the items you purchase on a regular basis. These add up. Where can you save? Do you eat out at restaurants a lot? Can you cut back on daily expenses, such as coffee, candy, soda, or cigarettes? Do you have services you do not really need, such as cable television or a cell phone? 2. Direct deposit or automatic transfer to savings. When you get paid, put a portion in savings through direct deposit or automatic transfer. If you have a checking account, you may sign up to have money moved into your savings account every month. What you do not see you do not miss! You may purchase U.S. Savings Bonds through payroll deduction. 3. Pay your bills on time. This saves the added expense of: Late fees Extra finance charges Disconnection fees for utilities such as phone or electricity Fees to reestablish connection if your service is disconnected The cost of eviction Repossession Bill collectors 4. If you use check-cashing stores regularly, you might pay $3 to $5 for each check you cash. This can easily add up to several hundred dollars in fees every year. Consider opening a checking account at a bank or credit union. FDIC Money Smart-Financial Education Curriculum 30 5. If you would like more information about checking accounts, you can take the Check it Out module. 6. If you get a raise or bonus from your employer, save that extra money. 7. If you have paid off a loan, keep making the monthly payments to yourself. You can save or invest the money for your future goals. 8. If you receive cash as a gift, save at least part of it. 9. Avoid debt that does not help you build long-term financial security. For example, avoid borrowing money for things that do not provide financial benefits or that do not last as long as the loan. Examples include: a vacation, clothing, and dinners out in restaurants. Examples of debt that helps build long-term financial security include: Paying for college education (for you or your child) Buying or remodeling a house Buying a car to get to work 10. Save your change at the end of the day. Take that change and deposit it into the bank every week or month. 11. When you get a tax refund, save as much of it as possible. 12. If your work offers a retirement plan, such as a 401(k) or 403(b) plan that deducts money from your paycheck, join it! Most employers will match up to $.50 on each dollar you contribute. The matched amount is free money! 13. If you decide to make investments, do your homework. Know what you are investing in. Get professional advice if you need it. You should have enough in savings to pay for 2 to 6 months of expenses in case of emergency. Make sure you have an emergency savings account before considering investing in nondeposit products. 14. If you own stocks, reinvest the dividends to purchase more stocks. Some companies offer an easy way to do this called a Dividend Reinvestment Program (DRIP). This process increases your investment faster, similar to compounding. 15. If you are interested in learning about investing, consider joining an investment club. Investment clubs are groups of people who work together to understand the process and value of investing even small amounts of money (as little as $5 to $10). FDIC Money Smart-Financial Education Curriculum 31 Evansville Financial Literacy Providers Catholic Charities “Neighbor to Neighbor” Budgeting and debt management (Outreach Program) Contact: Ms. Terry Lautner-Uebelhor 123 NW 4th Street Evansville, IN 47708 812-423-5456 Community Action Program of Evansville Pre-purchase homeownership counseling, debt management, credit management and budgeting Contact: Aretha Graves 27 Pasco Avenue Evansville, IN 47713 812-492-3967 Habitat of Evansville Pre-purchase counseling, debt management and budgeting for its partner families seeking to a home Contact: Amanda Sartore 1401 N. Fares Evansville, IN 47711 812-228-7797 Hope of Evansville Inc. /OGC Pre-purchase home ownership counseling, post-purchase homeownership counseling and debt reduction Contact: Tom Coe 608 Cherry Street Evansville, IN 47713 812-423-3169 Junior Achievement of Southwestern Indiana, Inc. Basic economics and financial education for elementary school students Contact: Ms. Theo Boots 233 SE 3rd Street Evansville, IN 47713 812-425-8152 Momentive Debt management, credit management and budgeting Contact: Sonja Williams Tri-State Professional Building 715 1st Avenue Evansville, IN 47710 812-422-1108 (ext 3068) 32 Financial Peace University Debt reduction and budgeting program offered at many local places of worship Blue Grass Church Budgeting and personal financial management (Financial Peace University) Contact: Jim Keepes 813 Herndon Drive Evansville, In 47711 812-437-2193 Or Contact Tracy McEuen 3631 E. Boonville-New Harmony Road Evansville, IN 47725 812-626-0120 33