Tesla Motors - Great Lakes Graphite

advertisement

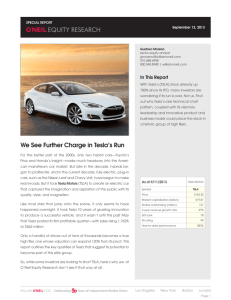

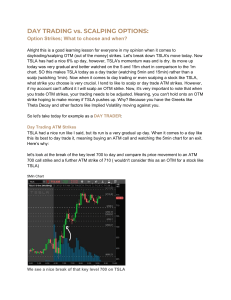

Tesla Motors (TSLA:NASDAQ) - On The Verge of Changing Everything, But Questions Remain August 1, 2014 By Chris Berry Charging Ahead Last week, TSLA released its Q2 2014 earnings. As a proponent of disruptive business models and the raw materials necessary to enable the upheaval, I always listen with rapt attention. The earnings of $0.11 per share on net income of $16 million (non-GAAP), and a loss of $0.50 per share on net income of $62 million (GAAP) were enough to satisfy the market and after a brief dip in after hours trading, the share price rebounded strongly. As is the case with many of the early-stage companies I follow, I’m more interested in production metrics, though revenue here is accelerating, indicating that TSLA is having no problem selling its cars. I’m willing to tolerate negative earnings and cash flow as long as the company is investing in future growth and increasing sales. This is clearly the case with TSLA which reported record production (8,763 Model S) and deliveries (7,579 Model S) in Q2 and is on track for more than 35,000 deliveries in 2014 with the stated goal of 100,000 deliveries by the end of 2015. Additionally, with a Cap Ex guidance of $850 million, TSLA has a Cap Ex/Sales ratio of over 20% unparalleled in the automotive business according to the FT. The next closest is Jaguar at 12%. TSLA is clearly a company in its early growth phase. Rather than dissect the numbers here, I think it’s important to look at the main takeaways from the call and consider any questions that arise for the company as they continue on an exciting journey to revolutionize the automotive and energy storage businesses. I came away with two main questions from the call. Key Takeaways and Subsequent Questions The long-stated goal here is to be able to produce an EV at a price which the mass market can afford. The conventional wisdom states that a price of $200/kWh is the minimum cost at which this could become a reality. The need to lower the battery cost was the main thrust behind the Gigafactory announcement and the recent news that Panasonic has committed to a portion of the estimated $5 billion cost for the factory is welcome. Source: Bloomberg New Energy Finance The chart above shows the trend in battery cost from various sources and the $200/kWh figure is in sight. Company management stated that 30% cost reduction in the battery could be “conservative”, though this is partially dependent upon full production from the Gigafactory, slated to commence in 2020. TSLA CEO Elon Musk also stated he foresees a cost of $100/kWh within ten years – making EVs more than competitive with traditional internal combustion engines. Question #1: How to finance the Gigafactory? This raises the first question yet to be answered from yesterday’s call: Based on what Panasonic will commit to the Gigafactory and what TSLA will provide, how will the remaining gap be filled? Other partners? State incentives? This could total up to $2 to $3 billion. Regarding the investment, Musk said: “Of that number, we see Tesla probably providing 40 to 50 percent of the total; Panasonic probably about 30 to 40 percent; the state maybe 10 percent; and other industrial partners maybe 10 to 15 percent, depending on how vertical we go with the factory,” With TSLA generating negative free cash flow (see below), if they are to raise the remaining funds to construct the Gigafactory, how will they do this in as non-dilutive a manner as possible? Source: TSLA Q2 2014 Investor Letter TSLA does have over $2.6 billion in cash on its balance sheet, but obviously can’t use all of this to fund Gigafactory construction. With Wall Street still in love with the stock, attaining capital shouldn’t be an issue, but minimizing dilution and optimizing the capital structure is a very important issue to consider. Demand for the Model S or Model X isn’t the issue here as Musk stated several times on the call that “We will not have a demand issue.” That said, what the financing package for the Gigafactory looks like will be a key issue going forward. Question #2: An alternate battery chemistry was discussed on the call. Will this have implications for raw materials demand? During the earnings call, an analyst asked a question surrounding battery chemistry and whether or not this would change to allow for further efficiencies and lower battery costs per kWh. The answer was particularly interesting in that while the geometry of the battery cell will change, so too will the chemistry. TSLA hopes to increase battery energy density by 10 to 15%. Energy density is defined as the amount of energy stored in a given system per unit mass or volume. Higher energy density helps lower the overall cost of the battery when produced at scale. Company management on the call said that “chemistry defines cost” and this is the key issue. TSLA uses a battery chemistry known as NCA (nickel cobalt aluminum) in the Model S where specific amounts and purities of various raw materials are all well known and are integrated into the company’s existing supply chain. The allure of supernormal metals demand from the Gigafactory has resuscitated numerous graphite and lithium junior mining companies in recent months but it remains to be seen how this metals demand will change based on slightly different chemistry – or whether or not it will change at all. As an aside, TSLA isn’t the only company ramping up battery capacity in anticipation of strong continued growth in vehicle electrification. This is important to keep in mind as TSLA isn’t the “only game in town.” LG Chem (051910:KR) recently announced plans (subscription req’d) to expand its own battery production capacity, entering into a JV agreement to build a plant in China which will produce enough batteries for 100,000 EVs by the end of 2015. With or without the Gigafactory, demand for raw materials such as lithium, graphite, or cobalt is set to increase – the only question is by how much. At risk of too much hyperbole, it is important to remember that each metal has different supply and demand characteristics and the long line of junior mining companies lined up to integrate into global lithium ion supply chains will likely get demonstrably smaller in the coming years. We can see below how much lithium is used in batteries, and this is with EVs (of all types) comprising a miniscule overall percentage of the existing global auto fleet. There is clearly a great deal of upside. Source: Roskill Takeaways Despite TSLA’s reputation as a “momo” stock, the company’s vision is compelling and becomes more believable with each milestone they hit. Ultimately vehicle electrification is about much more than cars and TSLA is just one of a number of companies investing in lithium ion battery capacity. Musk sees a run rate production of 100,000 Models S and X combined by the end of 2015 which would more than double the 2014 projected production of 35,000. It is growth like this, plus energy storage development, solar photovoltaic adoption, and emerging market growth with still color me optimistic on the future for select energy metals despite the rut the junior mining space finds itself in. TSLA’s stock price may or may not be rich depending upon your valuation model, but the company itself serves as a valid case study of nascent success in a market where many have failed before it. The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin. The information in this note is provided solely for users’ general knowledge and is provided “as is”. We at the Disruptive Discoveries Journal make no warranties, expressed or implied, and disclaim and negate all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose or non-infringement of intellectual property or other violation of rights. Further, we do not warrant or make any representations concerning the use, validity, accuracy, completeness, likely results or reliability of any claims, statements or information in this note or otherwise relating to such materials or on any websites linked to this note. I own no shares in any company mentioned in this note. The content in this note is not intended to be a comprehensive review of all matters and developments, and we assume no responsibility as to its completeness or accuracy. Furthermore, the information in no way should be construed or interpreted as – or as part of – an offering or solicitation of securities. No securities commission or other regulatory authority has in any way passed upon this information and no representation or warranty is made by us to that effect. For a more detailed disclaimer, please see the disclaimer on our website.