Answers to Frequently Asked Tax Time Questions

advertisement

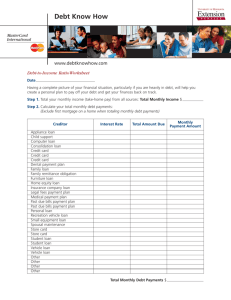

Smart Tips for Managing Your Debt Money Management – April 2008 Debt is not always a bad thing. Taking out a loan can make it possible to buy a home, purchase a new car or send your child to college. However, building up too much debt—-and failing to manage your outstanding balances wisely—-can be costly mistakes, according to the Missouri Society of CPAs. Many American families have allowed their debt to get out of control, but there are smart steps you can take to remedy the problem. CONSIDER CONSOLIDATION People often accumulate various debts over the years and end up paying off many small loans that all carry different interest rates. Consolidating all of these debts into one loan may be a better choice. When you consolidate, you take out one large loan and use it to pay off the smaller ones. While this can be a great convenience, remember that you should only take out a consolidation loan if you can find an attractive, low interest rate, which will allow you to pay less in finance charges and which will translate into a lower monthly payment. If you want to consolidate your debt, your choices include taking a bank loan or transferring your outstanding balances to a credit card with a low interest rate. You can also take out a home equity loan, which usually features a low rate as well as tax advantages, because you can deduct the interest on a qualifying home equity loan up to $100,000. No matter what your choice, be sure that you use the consolidation loan for its intended purpose rather than spending the money on new purchases. And if you consolidate using a home equity loan, remember that you could potentially lose your home if you fail to pay it off. Consider carefully whether you will be able to make your payments before risking your home ownership. CHOOSE THE BEST CREDIT CARD If you are carrying consumer debt on a credit card, make sure that you are paying the lowest rate possible on the outstanding balance. Low interest payments will be particularly important if you plan to carry a balance, transfer debt from another card or get a cash advance, because that interest will add up over time until you pay off your balance. Find out, too, about other charges such as annual fees or penalties for late payments. If you’re interested in getting rewards or rebates, check to see whether the card provides them, when they apply and when they expire. To evaluate your choices, create a chart with the name of each card issuer across the top and details—interest rates, fees, penalties—-listed vertically down the page. The chart will help you narrow your options and pick the best card for you. MAKE A NEW PLAN Debt consolidation and lowering your interest rates are great steps, but it’s important, too, to ensure that you don’t slide into debt again. Take time to analyze your current situation and consider whether you need to change your spending habits to avoid taking on more debt in the future. Creating an emergency fund can help to safeguard your finances when illness or loss of a job strikes. If day-to-day overspending is the culprit, take time to create a budget and then make sure your purchases do not exceed the amount you budgeted. CONSULT AN EXPERT Your local CPA can help you assess consolidation loans or compare your borrowing options. He or she can also provide advice on how to create a budget so that you can live within your income. Contact your CPA today for advice on questions about managing your debt or any other financial issues. To find a CPA near you, visit http://www.mocpa.org/public/referral/findcpa.aspx.