Exercises on Discounted Cash Flow Valuation (I)

advertisement

")

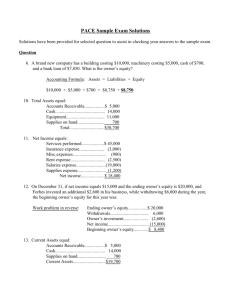

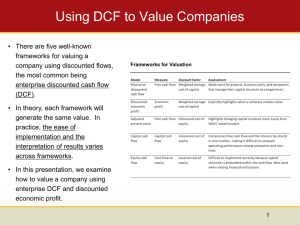

Exercise II: Discounted Cash Flow & Relative Valuation 14. Calculate the Capital Cash Flow using the following data (all amounts are in EUR 1000): EBIT Depreciation Net Investment Tax paid Payments to debt holders: Interest Repayment 2400 700 900 570 120 250 15. Use the following data about the firm 3 Ways Ltd., all amounts are in EUR 1,000. The company to be valued generates a constant annual expected EBIT in perpetuity. Assumptions Invested Capital Annual EBIT in perpetuity Tax rate t Firm’s borrowing rate kd D/E ratio Equity beta βE Riskfree interest rate Market equity risk premium Annual depreciation D Annual gross CAP. EX. Change in net working capital 8,000 2,000 40% 10% 2/3 1.2 10% 6% 1,000 1,000 0 Calculate the value of the firm, of its debt and equity by the following approaches: (a) Discounting Capital Cash Flows (b) Adjusted Present Value model (c) Economic-Profit-Based Valuation model 16. The following information is given for the 10-year forecast period: Assumptions NOPLAT in the current year 2,000 Investment rate 40% Return on new invested capital 15% WACC 10% Suppose the firm will last forever, but after the 10-year forecast period, the return on new invested capital is 12% and the annual growth rate of the NOPLAT is 2%. What will be your estimate of the firm value now? 17. Eutech AG paid dividends per share of EUR 3.56 in 2005, and dividends are expected to grow at a rate of 5.5% forever. The stock has a beta of 0.90, and the treasury bond rate is 6.25%. Assume that the equity risk premium is 5.5%. (a) What is the value per share, using the Gordon Growth Model? (b) The stock is trading for EUR 80 per share. What would the growth rate in dividends have to be to justify this price? 18. Suppose that A1 merges with Max. Assume that A1’s PE ratio is 20 and Max PE ratio is 15. If A1 accounts for 60% of the earnings of the merged firm, and if there are no synergies, what is the PE ratio of the combined firm? Where can you use insights from this exercise? 19. An analyst tells you that he uses PE multiples, rather than DCF, to value stocks, because he does not like making assumptions about fundamentals – growth, risk, payout ratios. Is his reasoning correct?