Purchasing Audit

Audit Objectives

1. To ensure purchasing process is adequately controlled.

2. To ensure proper segregation of duties in the purchasing process.

Planning

1. Obtain and document an understanding of the overall operating organization structure.

Consider the following areas:

Personnel - organization chart, total number of personnel, divisions, job descriptions,

etc.

Transactions -- volume/value of various transaction types processed

Systems

“Customers” - who are the key external and internal customers for the process?

2. Obtain electronic copies of relevant files as considered necessary to facilitate testing and

process analysis.

Understand the Process

1. Conduct interviews with key Purchasing individuals to gain an understanding of the

Purchasing process.

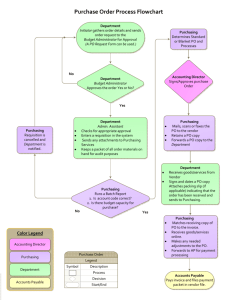

2. Create process maps to visualize the flow of information and to identify key points of

control and risk.

3. Review relevant written departmental policies and procedures/goals and objectives,

including all Purchasing policies.

4. Evaluate current practice against known best practices.

5. Interview key management in the Purchasing department to gain an understanding of the

workflow within each area. Document discussion.

Detail Testing

1. Perform detail testing on 20 selected purchasing transactions to assess the operation and

effectiveness of key controls. A wide variety of dollar value procurements from all commodity

groups will be selected. The selection will be tested for the following:

Purchase properly authorized – confirm the existence of properly approved Purchase.

Requisition (PR) and Purchase Order (PO).

PO accurately completed – description of items compared between the PR and PO.

Timely placement of the Purchase Order – number of days elapsed between PR and

placement of PO.

Completeness – all items tested from the PR were in fact ordered.

Vendor Selection is accurate between the PR and PO.

Pricing between the PR and the PO is accurate.

Testing will be performed to facilitate the following:

2.

Enhance our understanding of the “nuts and bolts” of the process.

Test our understanding of key controls.

Assess if key controls were operating consistently.

Test all transactions selected for the following, if not specifically noted in step #1 above:

Authorization

Validation

Accuracy

Proper process

Completeness

Timeliness

Discuss sample size and approach with IA manager prior to commencing testing.

3. Test to see if adequate controls exist in the receiving function.

Does receiving match the amount of goods received to the PO?

Does receiving receive goods that do not have a PO? How often does a product come in

that a PO needs to be generated for then?

4. Analyze the Return to Vendor (RTV) process. Test for:

Quantity outstanding

Length of time outstanding

Processes in place to track outstanding goods

5. Purchasing Proper Process

What should be on a PO and what shouldn’t?

Do cutoff testing to see if purchasing is cutting PO’s that don’t need to be cut.

Ensure purchasing isn’t processing transactions that do not have a PO.

6. Identify metrics used by management to monitor/ manage entire process.

Test accuracy of metrics as deemed necessary.

Assess need for additional/different metrics.

0

0