Document

advertisement

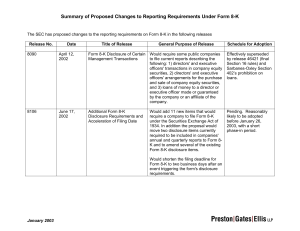

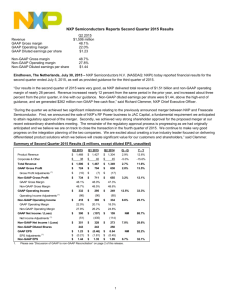

MEMORANDUM 3500 SunTrust Plaza, 303 Peachtree Street, N.E. Atlanta, Georgia 30308-3242 (404) 521-3939 Facsimile: (404) 581-8330 Real Time Issuer Disclosures This outline summarizes some of the key points of the SEC's rulemaking on real time issuer disclosures. This information should be considered in conjuction with the new rules on non-GAAP financial measures; see Tab D. If you have any questions on these rules, please feel free to call Lisa Stater at (404) 581-8255. IMPORTANT NOTE: The rules adopted with respect to the new Form 8-K disclosure requirements are effective as of March 28, 2003. As a result, all earnings releases and similar announcements made after March 28, 2003 will need to comply with these rules. I. II. Overview A. Section 409 of the Sarbanes-Oxley Act amended the Securities Exchange Act to provide that issuers must disclose to the public on a "rapid and current basis" information regarding the financial condition or operations of the issuer, as the SEC determines by rule. B. On January 22, 2003, the SEC adopted an amendment to Form 8-K - applies to earnings announcements and similar disclosures. Amendment to Form 8-K - Results of Operations and Financial Condition A. ATI-2041576v2 Reporting requirement: 1. If a registrant makes a public announcement or release (including an update) disclosing material nonpublic information regarding the registrant's results of operations or financial condition for a completed quarterly or annual period, the registrant shall briefly identify the announcement or release and include the text of it as an exhibit. 2. Requirements apply to press releases and reports to stockholders, but not to Forms 10-Q and 10-K. 3. Filing must occur within 5 business days (note that the SEC is considering reducing to 2 days) and is not deemed "filed." You may specifically state that you intend the material to be filed and/or incorporated by reference in other filings, which will reinstate the "filed" status for purpose of liability under the Securities Exchange Act. B. C. ATI-2041576v2 Exception: no Form 8-K is required to be filed in the case of disclosure of material non-public information that is disclosed orally, telephonically, by webcast, by broadcast, or by similar means if: 1. the information is provided as part of a presentation that is complementary to, and initially occurs within 48 hours after, a related, written announcement or release that has been furnished on Form 8-K pursuant to this item prior to presentation; 2. the presentation is broadly accessible to the public by dial-in conference call, by webcast, by broadcast, or by similar means; 3. the financial and other statistical information contained in the presentation is provided on the registrant's web site, together with any information that would be required under Reg. G; and 4. the presentation was announced by a widely disseminated press release that included instructions on accessing the presentation and the location of the registrant's web site where the information would be available. Required disclosures if non-GAAP financial measures included: 1. presentation of GAAP with equal or greater prominence than non-GAAP financial measure; 2. reconciliation of non-GAAP financial measure; 3. statement as to importance to investors of non-GAAP financial measure; and 4. any other material uses of non-GAAP financial measures by management. 2