Basic Concepts

advertisement

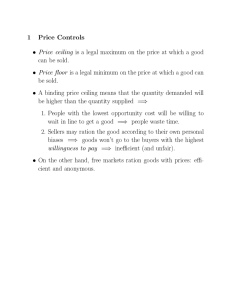

Managerial Economics 2015 Topic 7 Self-assessment Problems (Answers) Basic Concepts 1. a. A market is an institution that facilitates trading (exchange) of goods or services or factors of production or future commitments. b. Over to you. 2. Market equilibrium is point at which the demand and supply curves intersect. At the equilibrium price, the quantities of the good or service or factor that buyers are willing and able to buy equal the quantities that sellers are willing and able to sell. If the market price is set below that level, buyers are demanding larger quantities than sellers are willing to sell (excess demand) and the competition between buyers allows sellers to raise the price until the equilibrium price is reached and the balance between supply and demand is restored. The converse is true if the market price is set above the equilibrium price. In the latter case, competition between sellers forces the market price down until excess supply is eliminated. 3. The ‘invisible hand’ of the market place refers to market forces that ensure that prices are set at levels that balance supplies and demands and that trading, production and consumption decisions made by atomistic, self-interested individuals produce desirable social outcomes. 4. A price ceiling is a maximum price set by law for a particular good or service. Example: rent control. A price floor is a minimum price set by law for a good or service. Example: minimum wage. 5. When the price of petrol increases, the demand for second hand cars is likely to decrease. Second hand cars tend to be purchased by lower income people who may find car travel too expensive if the price of fuel is high. For similar reasons, the supply of second hand cars is likely to increase as many existing owners decide to sell and substitute public transport for car travel. However, some owners of new cars may switch from new to second hand cars, thus, increasing demand for the latter, when higher fuel bills reduce drivers’ ability to meet the capital cost of new cars. 6. The short run effect of a price ceiling is excess demand, eg, rent controls in housing make landlords unwilling to supply rented accommodation at the price. Potential tenants will also try to bypass rent ceilings by offering landlords capital inducements in the form of ‘key money’. In the long run, the stock of rented accommodation will decline as vacant dwellings are removed from the rental market. 7. Price controls are hardly ever effective as they can be sabotaged by buyers and sellers and are usually poorly targeted by (price) administrators. They may be desired by some vested interests but are socially harmful as they reduce market efficiency and send signals that encourage the misallocation of resources. Multiple Choice Problems 8. Breakeven analysis allows a firm to determine the level of output necessary to enter or to remain in a market. This is where Total Revenue = Total Cost. a-d are False and e is True. 9. MR=MC (see the previous discussion of monopoly) a-c and e are False and d is True. 10. Mark-up pricing ignores elasticity of demand. However, if it took the latter into account it would be more likely to coincide with the profit maximising rule MR=MC where MR reflects the price elasticity of demand. a-c and e are False and d is True. 11. If there is a binding price ceiling (and thus, excess demand), an increase in market demand will not affect market price and will not lead to a change in quantity supplied. Those who purchase the good are the lucky ones to get it. a and c-e and e are False and b is True.