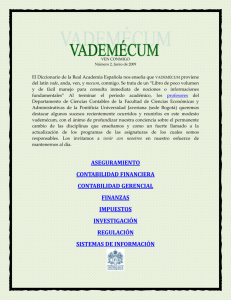

Número 10 - Pontificia Universidad Javeriana

advertisement