Credit Matters Credit Concepts Workshop (CMCCW

advertisement

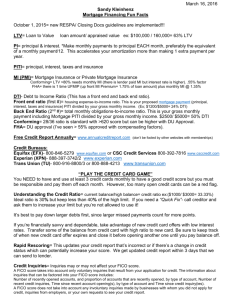

Credit Concepts Workshop Presentation Script (Part I of II) (HAND OUT QUIZ PRIOR TO PRESENTATION) Opening Slide: Welcome and thank you for participating at this Credit Education Workshop. My name is __________, and I am a________ with _________. With the short time that I have to give this presentation I hope to convey some helpful information regarding credit. And, because our time is limited, I would ask that if you have any questions, to please hold them until the end of my presentation. I’ll be handing out some information today that you can take with you. I’ll also be providing you with a form to fill out if you would like more information on any of the things I share with you today. This is the first of two presentations, both of which I believe are essential for everyone to attend. As a (loan officer, financial planner, real estate agent, data security specialist, etc.), I have found that credit plays a very important role in lives of my clients. So, having said that, let’s jump right in. Workshop Goal and Objectives: THE MAIN GOAL IN BOTH PRESENTATIONS IS TO PROVIDE USABLE INFORMATION TO HELP YOU MANAGE AND PROTECT YOUR CREDIT WORTHINESS. This presentation will achieve 2 objectives. OUR FIRST OBJECTIVE IS TO LEARN ABOUT THE PRINCIPLES OF CREDIT. Here I will be discussing the emphasis that has been placed upon credit scores, what is in your credit report and how scoring works. OUR SECOND OBJECTIVE CENTERS ON HOW CREDIT AFFECTS OUR ABILITY TO OBTAIN FINANCING, EMPLOYMENT OPPORTUNITIES, AND INSURANCE RATES. Quiz: Take 2 minutes for a quiz that tests your knowledge of credit and financing. (ALLOW A MAX OF 2 MINUTES FOR QUIZ) 1 (WHILE THEY ARE FILLING OUT THE QUIZ, HAND OUT THE FOLLOWING: PRESENTATION WORKBOOK HANDOUT AND OPT-IN FORM) The 3 C’s of Financing: Now let’s look at the principles of credit and financing. THE THREE C’S OF CREDIT AND FINANCING ARE THE THINGS THAT CREDITORS CONSIDER WHEN YOU APPLY FOR CREDIT. They are your character, your capacity, and you’re collateral. COLLATERAL IS AN ASSET THAT SERVES TO SECURE A LOAN. Your house would be collateral for a mortgage loan, for example. THE SECOND “C” IS CAPACITY AND REFERS TO YOUR INCOME. More specifically, lenders look at your income compared to your debt payments, otherwise known as your debt to income ratio, as a factor in determining your ability to pay back a loan. THE THIRD “C” IS YOUR CHARACTER…OR YOUR CREDIT HISTORY. Before 1980, it was your relationship with your banker. Today it is your credit score. The C’s - What Changed? WHAT CAUSED THIS CHANGE? QUITE SIMPLY, THE SECURITIZATION OF MORTGAGE LOANS. NOW WHAT IS THAT? In laymen’s terms, mortgage loans are bundled into investment portfolios and graded for their risk level. These investment portfolios are then sold to investors in the form of “bonds” on Wall Street. In order for these bonds to be graded and given a risk level of say, B+, the mortgage loans within the portfolios have to meet standardized parameters. These parameters relate to the 3 C’s (Collateral, Capacity, and Character). Collateral is standardized by an appraisal. The income is standardized by income documentation (paycheck stubs). The Character was the component that needed to be standardized. A lender relationship was not a realistic parameter for a loan portfolio. There needed to be a quantifiable “Character” or “credit history” value…a credit score. This may seem a bit complex…but the bottom line is…today, every consumer needs to understand the importance of effectively managing their credit worthiness. 2 The Cost of Bad Credit: CREDIT AFFECTS OUR FINANCING COSTS, INSURANCE RATES, & EMPLOYMENT OPPORTUNITIES. Here is an example of a $100, 000, 30-year mortgage loan. As most of you know, the credit score will affect the interest rate, but it also affects the amount you can borrow against your home’s appraised value; also known as the max loan to value ratio (LTV). The higher the score, the more of your home’s value you can finance. You can also see that with a low credit score you have a higher payment. According to the numbers on this diagram, your payment could be more than $350 a month higher due to a higher loan interest rate. TODAY, I WILL BRIEFLY SHARE A FEW THINGS YOU CAN DO TO IMPROVE YOUR SCORE, BUT IF YOU’D LIKE MORE INFORMATION MAKE SURE TO INDICATE THIS ON THE OPT-IN FORM. The Role of the Credit Bureaus: The 3 Credit Reporting Agencies, are TransUnion, Equifax, and Experian. THESE THREE CREDIT BUREAUS ARE PROFIT-MAKING COMPANIES THAT GATHER YOUR CREDIT DATA AND SELL IT TO THE FINANCIAL INDUSTRY IN THE FORM OF CREDIT REPORTS. Even though the bureaus are separate companies, they all aim to protect financial institutions such as banks and creditors. It is obvious that banks and creditors want to avoid lending to consumers that may be a bad credit risk. Creditors rely on the credit bureaus to report ANY “potentially” negative credit data about consumers. WHAT DOES THIS MEAN? THE BUREAUS HARDLY CARE WHEN THEY MISREPORT ITEMS THAT HURT YOUR SCORES BECAUSE THEY ARE NOT TRYING TO PROTECT CONSUMERS. CREDITORS AND LENDERS DON’T MIND THIS AT ALL BECAUSE IT ASSURES THAT THEY ARE ONLY LENDING TO CONSUMERS WITH HIGH CREDIT SCORES AND LOW CREDIT RISKS. Errors In Your Credit Report: 30% OF ALL CREDIT REPORTS CONTAIN “SERIOUS” ERRORS THAT RESULT IN THE DENIAL OF CREDIT. These errors truly damage your score. Some examples are: Paid items still showing an unpaid balance Medical items sent to collection prior to insurance payment Someone else’s items reporting; people with similar names or family members Items reported in bankruptcy still showing balances owed 3 THIS IS WHY EVERYONE SHOULD REGULARLY OBTAIN A CREDIT REPORT. IF YOU’D LIKE TO MEET AND TALK ABOUT YOUR REPORT, MAKE SURE TO FILL OUT THE PROPER SECTION ON THE OPT-IN FORM. What’s in Your Credit Report? Information the bureaus collect and report about you includes personal information such as your DOB, SSN, driver’s license, employment, past addresses and aliases. (ex: maiden name) YOUR INCOME IS NOT IN YOUR CREDIT REPORT. The next portion of your credit report contains past and current trade lines – these include accounts you make payments on, as well as judgments, liens, collections and bankruptcies. Finally, your report displays your inquiries. We’ll discuss these in more detail shortly. FINALLY ALL POSITIVE AND NEGATIVE ACCOUNTS REPORT FOR 7 YEARS FROM THE DATE OF LAST ACTIVITY, EXCLUDING BANKRUPTCIES (10 YRS) AND UNPAID TAX LIENS (15 YRS). Closing an account, making a payment, or reopening an account are all examples of account activity. Credit Scores: FICO Credit scores range from 300 to 850. Above 700 is an excellent credit score; creditors consider you a low credit risk and extend you the best lending rates. Between 600-700 is generally viewed as an OK credit score usually is the cutoff point for a prime rate loan. Anyone below a 600 is categorized as having credit problems. WE WILL DISCUSS HOW YOU CAN IMPROVE YOUR CREDIT BY REMOVING NEGATIVE ITEMS FROM YOUR REPORT IN THE NEXT PRESENTATION. Who is FICO? ESTABLISHED IN 1956, FICO IS KNOWN FOR CREATING RISK MODEL FORMULAS THAT GENERATE CREDIT SCORES. Lenders such as banks and creditors use these scores to determine financing. 4 THESE RISK MODEL FORMULAS ARE TRADE SECRETS OF FICO AND ARE NOT SHARED WITH FINANCIAL INSTITUTIONS OR CREDIT BUREAUS. FICO USES DIFFERENT FORMULAS FOR DIFFERENT TYPES OF FINANCING, GENERATING DIFFERENT SCORES. For example, an auto score has different risks, so is different from a mortgage score, which is different from a credit card score. OBTAINING YOUR OWN CREDIT SCORE HAS NO MEANING SINCE IT IS NOT TIED TO ANY CREDIT APPLICATION. Key #1 – Payment History: Let’s now look at the key factors that affect your credit score. 35% OF YOUR SCORE IS DETERMINED BY HOW WELL YOU MAKE YOUR PAYMENTS ON TIME IN THE PAST 24 MONTHS. This area considers both positive accounts such as auto loans, mortgage loans, credit cards and negative accounts, like collections, late pays, bankruptcies, and judgments. Creditors want to know if you can make payments on time, so they put a lot of weight on how well you have made on-time payments in last 12-24 months. They put less weight on what your payment track record was 4 years ago. Key #2 – Utilization Ratio: The next factor that you need to be concerned about is your utilization ratio. THE UTILIZATION RATIO - THE TOTAL OF ALL BALANCES YOU CARRY ON CREDIT CARDS AND CHARGE ACCOUNTS COMPARED TO THE TOTAL OF THE CREDIT LIMITS, CAN DRAMATICALLY IMPACT YOUR SCORE. FICO’S RISK MODELS REDUCE CREDIT SCORES WHEN THE UTILIZATION RATIO IS OVER 30%. If for example your credit card limits add up to $10,000 and your credit card balances are currently $3,000, your utilization ratio is 30%. PEOPLE THAT HAVE UTILIZATION RATIOS IN EXCESS OF 60% CAN EXPECT TO SEE A SCORE REDUCTION OF 50 POINTS OR MORE. Don’t close revolving accounts with high credit limits, as this increases utilization ratio and decreases your score. Key #3 – Credit Inquiries: AN INQUIRY IS A RECORD OF SOMEONE CHECKING YOUR CREDIT INFORMATION. 5 At this point you might think, the more inquiries you have on your credit report, the worse your score will be. This is only partially correct. THERE ARE TWO TYPES OF INQUIRIES: HARD INQUIRIES, THOSE THAT AFFECT YOUR SCORE AND SOFT INQUIRIES, THOSE THAT DON’T. HARD INQUIRIES ARE REPORTED WHEN APPLYING FOR CREDIT. AUTO AND MORTGAGE INQUIRIES WITHIN THE LAST 30 DAYS ARE IGNORED. AUTO AND MORTGAGE INQUIRIES IN ANY 14-DAY PERIOD COUNT AS ONE INQUIRY. For example it is common when applying for auto financing that a dealership runs your credit with 6-10 different finance companies, seeing which one of them will approve you for a loan. This will show as multiple inquiries on your credit report, but will only count as one credit inquiry against your score, because these inquires are within a 14-day period. Let’s say you apply for a mortgage with three different banks and they all run your credit. Again, this will count as only one inquiry against your score 30 days later. The reason for this is that the credit formula takes into consideration that people shop and people will not buy 3 houses next week and 6 cars the following week. However, if you apply for 6 credit cards at once, this will show as 6 credit inquiries and each one will affect your score, because you may get 6 credit cards at once. INQUIRIES ACCOUNT FOR LESS THAN 5% OF YOUR TOTAL SCORE AND SELDOM IMPACT YOUR SCORE BY MORE THAN 10-15 POINTS. WHEN YOU OBTAIN YOUR OWN CREDIT REPORT ONLINE, IT IS CONSIDERED A SOFT INQUIRY AND WILL NOT HARM YOUR CREDIT SCORE. Other soft inquiries are generated from promotional offers made by lenders, when current creditors and collection agencies review your credit, when prospective employers check your credit, and when applying for insurance. None of these affect your score. Credit Counseling Ruins Scores: DO NOT CONFUSE CREDIT RESTORATION WITH CREDIT COUNSELING. With credit counseling, the consumer agrees to make a payment to the credit counseling company who, acting as a trustee negotiates for a reduced payment with each creditor and will make their payments for them. Although they take on a limited power of attorney and stop collection harassment, the creditor considers these reduced payments as partial payments and reports them late. This is similar to a Chapter 13 bankruptcy, which is why most lenders view it as just that—a Chapter 13. With late payments being reported and lenders viewing it as a Chapter 13, Credit Counseling ruins scores and is therefore considered, a work of the devil. 6 Thank You for Coming: Because our time was limited, I apologize if I ran over the information too fast. I hope each of you feels this has been beneficial and that everyone attends the next presentation. IF WOULD LIKE TO RECEIVE MORE INFORMATION ABOUT CREDIT, PLEASE FILL OUT THE TOP HALF OF THE OPT-IN FORM TO RECEIVE OUR NEWSLETTER. IF YOU WOULD LIKE TO PERSONALLY MEET AND TALK ABOUT A CERTAIN TOPIC, PLEASE FILL OUT THE BOTTOM HALF OF THE FORM. OUR NEXT WORKSHOP IS SCHEDULED FOR:________. WE WILL BE ADDRESSING HOW TO IMPROVE CREDIT SCORES AND PROTECTING YOUR CREDIT FROM IDENTITY THEFT QUIZ ANSWERS THE ANSWER TO NUMBER 1 WAS B & C. CREDIT SCORES AFFECT INTEREST RATES AND DOWN PAYMENTS. INCOME IS NOT REPORTED. NUMBER 2 WAS C. YOUR CHARACTER, YOUR CAPACITY, AND YOUR COLLATERAL. NUMBER 3 WAS D. FAIR ISAAC CORPORATION ASSIGNS CREDIT SCORES IN THE UNITED STATES. THE ANSWER TO NUMBER 4 WAS C. YOU ARE ENTITLED TO ONE FREE CREDIT REPORT EVERY TWELVE MONTHS. THE FTC THOUGHT YOU SHOULD BE ABLE TO REGULARLY MONITOR YOUR CREDIT REPORT FOR ID THEFT. NUMBER 5 WAS C. MOST ACCOUNT INFORMATION REMAINS ON YOUR CREDIT REPORT FOR SEVEN YEARS FROM THE DATE OF YOUR LAST ACTIVITY. NUMBER 6 WAS A, B, & D. INVESTING DOES NOT REQUIRE CREDIT. 7