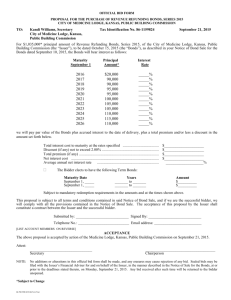

notes on debt management

advertisement