Course: FIN3001EF Personal Financial Planning

Review Exercise

Short Questions:

1. State 4 advantages of personal financial planning.

i.

Increased effectiveness in obtaining, using, and protecting your financial

resources.

ii.

Increased control of your financial affairs.

iii.

Improved personal relationships.

iv.

A sense of freedom from financial worries obtained by looking to the future.

2. What are the steps involved in the financial planning process?

i.

Determine your current financial situation.

ii.

Develop your financial goals.

iii.

Identify alternative course of action.

iv.

Evaluate your alternatives.

i.

Create and implement your financial action plan.

v.

Review and revise your plan.

3. What are the purposes of personal financial statement?

The purposes of personal financial statement are

Report your current financial position in relation to the value of the items you

own and the amounts you owe.

Measure your progress toward your financial goals.

Maintain information on your financial activities.

Provide data you can use when preparing tax forms or applying for credit.

4. Which 4 budget systems are common to use?

Mental budget

Physical budget

Written budget

Computerised budget

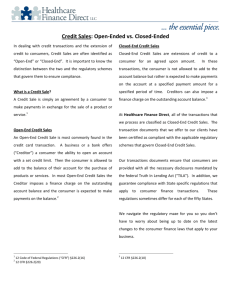

5. What are the two basic types of credit? Give an example for each.

Two basic types of consumer credit are closed-end and open-end credit. With

closed-end credit, one-time loans that the borrower pays back in a specified

period of time and in payments of equal amounts. With open-end credit, a

line of credit in which loans are made on a continuous basis and the borrower

is billed periodically for at least partial payment.

Examples for closed-end credit: mortgage loans, automobile loans, and

installment loans.

Examples for open-end credit: overdraft protection, credit cards, revolving

cheque credits.

6. What is consumer credit?

Credit is an arrangement to receive cash, goods or services now, and pay for them in

the future. Consumer credit is the use of credit for personal needs except a home

mortgage , by individual and families.

7. What are the Five Cs of Credit?

i.

Character

ii.

Capacity

iii.

Capital

iv.

Collateral

v.

Conditions

8. What are the danger signals to show you are in debt problems ?

Paying only the minimum balance each month.

Increasing the total balance due each month.

Missing or alternating payments or paying late.

Intentionally using overdraft protection or taking frequent cash advances.

Using savings to pay routine bills such as food.

Getting second or third payment notices.

Not talking to your partner about money or talking only about money.

Depending on overtime to meet routine expenses.

9. State 4 types of health care coverages?

Hospital expenses insurance.

Surgical expense insurance.

Physician expense insurance.

Major medical expense insurance.

Comprehensive major medical insurance.

Dread disease and cancer insurance policies.

Hospital indemnity.

Dental expense insurance.

Vision care.

Long term care insurance.

10. What is the whole life policy and one of policy options given?

Whole life policy is also called straight life insurance. Policyholder pays the

premium as long as his/her live. The amount of premium depends on your age when

you start the policy. The policy provides death benefits and accumulates a cash

value. The policyholder can borrow against the cash value or draw it out at

retirement. e.g. limited life policy, variable life policy, adjustable life policy and

universal life.

11. What is the definition of life insurance, and the purpose of the life insurance?

Life insurance is an insurance company promises to pay a lump sum at the time of

the policyholder’s death, or sometimes while they are still alive.

Purpose of life insurance is protecting someone who depends on you from financial

loss related to your death.

12. Explain what role(s) are you playing in the investment process?

As an investor the role should be most important in the investment process, namely

evaluate potential investments, seek the assistance of a financial planner, monitor

the value of the investments, keep accurate and current records, and consider the

tax consequences of selling investments.

13. What is the difference between straight-life annuity and joint-and-survivor annuity?

Straight-life annuity provides more income than any other type, but payments stop

when you die. Joint-and-survivor annuity pays until the last survivor you designate

dies.

14. What are the ways to manage risk?

There are 4 ways to manage the risk, namely risk avoidance, risk reduction, risk

assumption, and risk shifting.

15. What are the 5 components of risk factor?

Inflation risk

Interest rate risk

Business failure risk

Market risk

Global investment risk

16. What is the difference between Pure Risk and Speculative Risk?

Pure Risk is a risk which is insurable. There is chance of loss and no gain. The

incident is happened accidentally and unintentional. Nature and financial loss of the

risk can be predicated.

Speculative Risk is a risk which is uninsurable. There is chance of loss or gain such

as starting a business.

17. How does tax avoidance differ from tax evasion?

Tax avoidance refers to the use of legitimate methods to reduce one’s tax evasion is

taxes. Tax evasion is the use of illegal actions to reduce taxes.

18. What are the characters of taxation system in Hong Kong?

Schedular Tax System which is charging separately for 3 different types of

income under 3 headings: salaries tax, property tax and profits tax

Simplicity – direct and indirect tax

Territorial source concept – only income derived from Hong Kong is taxable.

Low tax rate

Year of assessment – between 1st April of the current year and 31st March of

the next year.

Provisional tax assessment system – required to pay provisional tax for the

next year in advance.

Forms of assessment – separate assessment, joint assessment, and personal

assessment.

19. What is the different between the guardian and trustee?

The guardian will take the responsibility for providing the children with personal care

and managing the estate for them. Trustee will manage property for benefit of

children.

20. What are the responsibilities of an Executor?

Take control of assets of the estate.

File an inventory of assets and liabilities with the court.

Liquidate assets if necessary to pay claims.

Distribute assets based on the instructions in the will.

Make a final accounting to the court.

Financial Problems:

1. Use the items in the following table to calculate the ratios required:

Liabilities

Liquid assets

Monthly credit payments

Monthly savings

Net worth

Current liabilities

Take-home pay

Gross income

Monthly expenses

$12,000

$2,200

$150

$130

$36,000

$550

$900

$1,500

$850

Debt ratio: Liabilities/Net worth = $12,000/$36,000 = 0.3333

Current ratio: Liquid assets/Current Liabilities = $2,200/$550 = 4

Debt-payment ratio: Monthly credit payment/Take-home pay = $150/$900 = 0.1667

Saving ratio: Amount saved per month/Gross monthly income = $130/$1,500 = 0.0867

Liquid ratio: Liquid assets/Monthly expense=$2,200/$850 = 2.5882

2. Use the following items to prepare a balance sheet and a cash flow statement. Determine

the total assets, total liabilities, net worth, total cash inflows, and total cash outflows.

Rent for the month, $650

Cash in checking account, $450

Spending for food, $345

Current value of automobile, $7,800

Credit card balance, $235

Auto insurance, $230

Stereo equipment, $2,350

Lunches/parking at work, $180

Home computer, $1,500

Clothing purchase, $110

Monthly take-home salary, $1,950

Savings account balance, $1,890

Balance of educational loan, $2,160

Telephone bill paid for month, $65

Loan payment, $80

Household possessions, $3,400

Payment for electricity, $90

Donations to church, $70

Value of stock investment, $860

Restaurant spending, $130

Total assets = $18,250 ($450 + 1,890 + 7,800 + 2,350 + 1,500 + 3,400 + 860)

Total liabilities = $2,395 ($235 + $2,160)

Net worth = $15,855 ($18,250 - $2,395)

Total cash inflows = $1,950

Total cash outflows = $1,950 ($650 + 345 + 230 + 180 + 110 + 65 + 80 + 90 + 70 + 130)

3. Based on the following data, calculate the ratios requested:

Net worth $48,000

Take-home pay $2,600

Gross income $2,850

Current liabilities $950

Monthly credit payments $540

Liquid assets $5,200

Liabilities $7,000

Monthly savings $180

i. Debt ratio:

7,000/48,000=0.1458

ii. Current ratio:

5,200/950=5.47

iii. Debt-payment ratio:

540/2,600=0.21

iv. Saving ratio:

180/2,850=0.06

4. Based on the following data, calculate the ratios requested:

Long-term liabilities $854,321

Net worth $1,448,000

Liquid assets $55,200

Current liabilities $45,650

Mortgage repayment $84,000

Mortgage loan outstanding $555,234

Credit card repayments $5,540

MPF $12,000

Interest earned on savings $150

Gross income $281,850

Car loan repayment $38,087

Property market value $685,483

i.

Debt-payment ratio:

(5,540 + 38,087) / (28,1850 + 150 – 12,000) = 0.16

ii.

Debt-to-equity ratio:

(854,321 + 45,650 – 555,234) / (1,448,000 -685,483) = 0.45

5. What would be the 6-month’s interest earnings for a person who deposits $2,000 monthly in

savings at an annual interest rate of 5.5 percent?

$2,000(1+5.5%/12)6 +$2,000(1+5.5%/12)5 +$2,000(1+5.5%/12) 4 +$2,000(1+5.5%/12)3

+$2,000(1+5.5%/12)2 +$2,000(1+5.5%/12)

= $12,193.98

$12,193.98 - $12,000 = $193.98

6.

If a person spends $100 a week on coffee (assume $5,200 a year), what would be the

future value of that amount over 3 years if the funds were deposited into his savings

account earning interest of 4 percent per annum (interest will be paid twice a year in 6th

and 12th month)?

$2,600(1+2%)6 +$2,600(1+2%)5 +$2,600(1+2%)4 +$2,600(1+2%)3 +$2,600(1+2%)2

+$2,600(1+2%) = $16,729.14

7. You plan to open a fast food shop after 3 years and $150,000 of capital is required. You

decide to deposit a lump sum of money into a time deposit with every 3-month's renewal.

The interest rate is 3.5%p.a. How much the lump sum of money does you need to deposit?

$150,000/[(1+3.5%/4)12]

= $135110.37

0

0