TOM TOM - Broker Bankia

advertisement

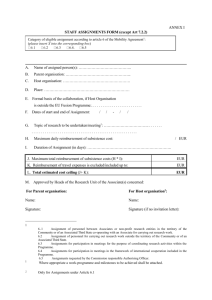

13 April 2015 TomTom Netherlands/Software & Computer Services Analyser SOFTWARE & COMPUTER SERVICES TomTom (Buy) Nokia’s sale of map business shows TT is Buy Nokia’s sale of map business shows TT is undervalued Recommendation unchanged 8.18 Share price: EUR closing price as of 10/04/2015 Target price: EUR 9.00 Target Price unchanged Reuters/Bloomberg TOM2.AS/TOM2 NA Market capitalisation (EURm) Current N° of shares (m) Free float 1,820 223 53% Daily avg. no. trad. sh. 12 mth Daily avg. trad. vol. 12 mth (m) Price high 12 mth (EUR) Price low 12 mth (EUR) Abs. perf. 1 mth Abs. perf. 3 mth Abs. perf. 12 mth 5,186,578 40,107 8.18 4.53 9.17% 40.17% 67.20% Key financials (EUR) Sales (m) EBITDA (m) EBITDA margin EBIT (m) EBIT margin Net Profit (adj.)(m) ROCE Net debt/(cash) (m) Net Debt/Equity Debt/EBITDA Int. cover(EBITDA/Fin. int) EV/Sales EV/EBITDA EV/EBITDA (adj.) EV/EBIT P/E (adj.) P/BV OpFCF yield Dividend yield EPS (adj.) BVPS DPS 12/14 949 136 14.3% 21 2.2% 60 3.1% (104) -0.1 -0.8 43.2 1.2 8.4 8.4 53.9 20.4 1.4 2.4% 0.0% 0.27 4.04 0.00 12/15e 1,019 149 14.6% 31 3.1% 63 2.6% (217) -0.2 -1.5 74.4 1.6 10.9 10.9 51.5 28.8 1.9 6.2% 0.0% 0.28 4.20 0.00 12/16e 1,035 185 17.9% 70 6.7% 99 6.0% (323) -0.3 -1.7 (154.0) 1.5 8.2 8.2 21.7 18.5 1.9 7.5% 1.7% 0.44 4.37 0.14 vvdsvdv sdy 8.5 8.0 7.5 7.0 6.5 6.0 5.5 5.0 4.5 4.0 Mar 14 Apr 14 May 14 Ju n 14 Ju l 14 Aug 1 4 Sep 1 4 Oct 14 Nov 1 4 Dec 14 Ja n 15 Feb 15 Source: Factset TOMTOM EuroNext (Rebased) Shareholders: P.Geelen 12%; P.F. Pauwels 12%; C.Goddijn 12%; H.Goddijn 12%; Analyst(s): Martijn den Drijver, SNS Securities Mar 15 Apr 15 The facts: Last Friday afternoon, Bloomberg reported that Nokia intends to sell its map business Nokia Here and that potential bidders include both strategic buyers as well as buy-out firms. According to BB, the company values the map business at EUR 2bn. Nokia has not reacted at all. But since the rumours surfaced on BB, TomTom’s shares have jumped significantly, ending up 11.5% on the day at a 52 week high. Our analysis: As we already wrote in an email on Friday, the EUR 2bn valuation is what is causing the TomTom share to react so positively because it implies a FY14 EV/EBITDA multiple of 25x and an FY14 EV/Sales multiple of 2.1. If we were to simply use those multiples on the FY14 results of TomTom, the implied enterprise value of TomTom would be EUR 3.4bn (EV/EBITDA) and EUR 1.9bn (EV/Sales). The enterprise value of TomTom before the rumours surfaced about Nokia’s intention to sell the maps business was EUR 1.6bn…. There are major differences between Nokia Here and TomTom. Nokia Here mainly sells its maps to the Automotive segment, which represents over 75% of the business, we assume. The remainder of the sales comes from the contract with Garmin (Nokia is the exclusive supplier of Garmin), some GIS and some LBS contracts. TomTom has a much more diversified business. It is also active in Automotive and Consumer (PND and Sports) but also has a thriving and high margin Fleet management solution business (the Telematics division) that Nokia does not have. If we were to really compare TomTom and Nokia Here, we would have to take out the Telematics business, value that separately using Fleetmatics of the US (the closest peer), and then use the Nokia multiples on the remainder of the business. In FY15, the Telematics unit is expected to generate sales of EUR 146m and an EBITDA of EUR 64m. Fleetmatics is currently valued at an FY15 EV/EBITDA of 16.7 giving Telematics an implied valuation of EUR 1.07bn. Let’s deduct 15% because of the difference between US and EU multiples, which gives TomTom Telematics an implied enterprise value of EUR 0.9bn. Having taken out Telematics leaves TomTom with an FY15 EBITDA of EUR 85m. We then use the implied EV/EBITDA multiple from Nokia to calculate the value of the remaining business, which gives it an enterprise value of EUR 2.23bn (25x EUR 85m). We realize we are using an FY14 multiple on a FY15 forecast EBITDA but we do not have estimates for Nokia Here EBITDA available. The total enterprise value would then be EUR 3.13bn or an equity value (TomTom is net cash EUR 103m) of EUR 3.23bn. This translates into EUR 14.4 per share. This is an imperfect calculation, we realize that. We are putting assumption on assumption, using high multiples from Fleetmatics. But it does show that TomTom remains undervalued. Who would be interested in buying Nokia Here? Given that cash flows are weak, we do not assume that a financial buyer will come out on top. Bloomberg names Microsoft, Yahoo, Apple and Uber as well as car manufacturers and Tier1s. We assume that the car manufacturers and the Tier1 suppliers have the best papers although Uber with its deep pockets cannot be ruled out either. martijn.dendrijver@snssecurities.nl +312 0 5508636 Conclusion & Action: The sale of Nokia Here will show what the value of a map business is and we expect it to come out higher than many have expected. The implied EUR 2bn valuation mentioned by Bloomberg already shows that TomTom is undervalued, especially as it has a thriving and high margin Telematics business that Nokia does not have.