Cash and Liquidity Management

Reasons for Holding Cash

•

•

•

•

Speculative motive—the need to hold cash to take advantage

of additional investment opportunities, such as bargain

purchases.

Precautionary motive—the need to hold cash as a safety

margin to act as a financial reserve.

Transaction motive—the need to hold cash to satisfy normal

disbursement and collection activities associated with a firm’s

ongoing operations.

Compensating balance requirements—cash balances kept at

commercial banks to compensate for banking services the

firm receives.

Target Cash Balance

Key issues:

• What is the trade-off between carrying a large cash

balance versus a small cash balance?

carrying costs versus shortage costs.

That is,

• What is the proper management of the cash

balance? BAT model versus Miller–Orr model.

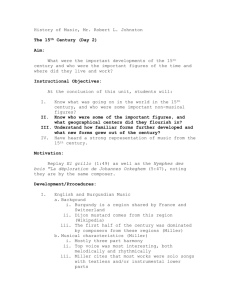

The BAT Model

Starting cash

C=$2 000 000

Average cash

$500 000=C/4

0

4

8

Weeks

The BAT Model

Assumptions

-Cash is spent at the same rate every day

-Cash expenditures are known with certainty

Optimal cash balance is where opportunity cost of holding

cash ([C/2]*R) = trading cost ([T/C]*F):

C

2T F /R

F = fixed cost of making a securities trade to replenish cash

T = total amount of new cash needed for transactions purposes over

the relevant planning period

R = the opportunity cost of holding cash (the interest rate on

marketable securities)

Miller–Orr Model

•

Assumes that, if left unmanaged, a company’s cash balance

would follow a random walk with zero drift.

•

Cash balance is allowed to wander freely between an upper

limit (U*) and a lower limit (L).

•

If cash holdings reach U*, management intervenes by

withdrawing U* – C* dollars to return the cash balance to the

target level C*.

•

If cash balance reaches L, management intervenes by

injecting C* – L dollars to return the cash balance to the

target level C*.

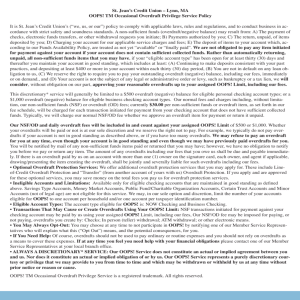

Miller–Orr Model

Cash

U*

C*

L

Time

X

Y

U* is the upper control limit. L is the lower control limit. The target

cash balance is C*. As long as cash is between L and U*, no

transaction is made.

Miller–Orr Model

L set by the firm

2

3

σ

C L F

R

4

U 3 C 2 L

Avg. cash balance 4 C L / 3

1

3

Example—Miller–Orr Model

Assume L = $0, F = $10, i = 0.5 per cent per month and

the standard deviation of monthly cash flows is $2000.

3

C $0 $10 $2000

0.005

4

$1 817

U 3 $1 817 2 $0

$5451

Avg. cash balance 4 $1 817 $0 /3

$2423

2

1

3

Miller–Orr Model Implications

• Considers the effect of uncertainty (through 2 in

net cash flows).

–

–

The higher the 2, the greater the difference between C*

and L.

The higher the 2, the higher is the upper limit and the

average cash balance.

• All things being equal:

–

–

the greater the interest rate, the lower is the C*

the greater the order costs, the higher is the C*.

Miller–Orr Model With Overdraft

•

Yield on short-term investments < cost of bank overdraft <

yield on long-term investments.

•

A dollar invested in short-term assets earns less than the

costs saved by applying that dollar to reduce overdraft usage.

•

The company invests nothing in short-term assets and as

much as possible in long-term assets, while meeting its

liquidity needs through using the overdraft facility.

Miller–Orr Model With Overdraft

U 0

3

2

C F / R d

4

L 3 C

Target overdrawn level 2 C

Where:

d = cost of bank overdraft

1

3

0

0