Annuity Distributions What are annuity distributions? How are

advertisement

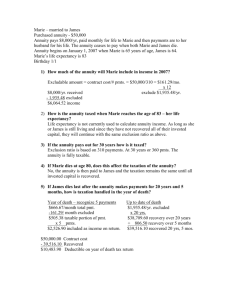

Annuity Distributions • What are annuity distributions? • How are annuity distributions made? • How are your annuity payouts computed if you elect to annuitize? • Who are the parties to an annuity contract? • How are annuity benefits paid out? • When are annuity benefits paid out? • What payout methods are available? • Options after death • What is the tax treatment of annuity payouts in the annuitization phase? What are annuity distributions? The second phase of an annuity contract, called the distribution phase, begins when you start receiving payments from the annuity. These payments are called annuity distributions. Distributions typically consist of principal and earnings. Caution: The examples used throughout this discussion are hypothetical. They do not reflect the actual performance of an annuity or the fees and charges associated with an annuity. How are annuity distributions made? Withdrawal option You can choose to simply withdraw earnings (or earnings and principal) from the annuity. There are several ways of doing this. You can withdraw all of the money in the annuity (both the principal and earnings) in one lump sum. You can also withdraw the money over a period of time through regular or irregular withdrawals. By choosing to make withdrawals from your annuity, you continue to have control over money you have invested in the annuity. In a sense, it is similar to a savings account at a bank. You can withdraw only earnings (interest) from the account, or you can withdraw both the principal and the interest. However, if you systematically withdraw the principal and the earnings from the annuity, there is obviously no guarantee that the funds in the annuity will last for your entire lifetime. Caution: Withdrawals made prior to age 59 ½ may be subject to a 10 percent federal penalty tax. Guaranteed income (annuitization) option A second distribution option is called the guaranteed income (or annuitization) option. If you select this option, your annuity will be "annuitized," which means that the current value of your annuity is converted into a stream of payments. This allows you to receive a guaranteed income stream from the annuity. The annuity issuer promises to pay you an amount of money on a periodic basis (e.g., Prepared By: Neal Lapierre Page 1 of 8 monthly, quarterly, yearly, etc.). If you elect to annuitize, the periodic payments you receive are called annuity payouts. You can elect to receive either a fixed amount for each payment period or a variable amount for each period. You can receive the income stream for your entire lifetime (no matter how long you live), or you can receive the income stream for a specific time period (10 years, for example). You can also elect to receive annuity payouts over your lifetime and the lifetime of another person (called a "joint and survivor annuity"). The amount you receive for each payment period will depend on the cash value of the annuity, how earnings are credited to your account (whether fixed or variable), and the age at which you begin receiving annuity payments. The length of the distribution period will also affect how much you receive. If you are 65 years old and elect to receive annuity payments over your entire lifetime, the amount you will receive with each payment will be less than if you had elected to receive annuity payouts over 5 years. Example(s): Over the course of 10 years, you accumulated $300,000 in an annuity. When you reach 65 and begin your retirement, you annuitize the annuity (i.e., elect to begin receiving distributions from the annuity). You elect to receive the annuity payments over your entire lifetime−−called a single life annuity. You also elect to receive a variable annuity payout whereby the annuity issuer will invest the amount of money in your annuity in a variety of equity portfolios. The amount you will then receive with each annuity payment will vary, depending in part on the performance of the portfolios. In the alternative, you could have elected to receive payments for a specific term of years. You could have also elected to receive a fixed annuity payout whereby you would receive an equal amount with each payment. Sally is 43 and is planning to retire when she turns 65. She purchases an annuity and makes annual premium payments of $3,000. For the next 22 years, the annuity accumulates tax−deferred income. When Sally turns 65, she chooses to annuitize. Sally stops making premium payments and starts receiving an annual payment of $8,000, which she will receive for the rest of her life. How are your annuity payouts computed if you elect to annuitize? Annuitization is computed using actuarial tables. These tables take into account the annuitant's life expectancy and interest earned. It's the annuitant whose life is of primary importance in determining the timing and amount of the payout. Thus, the annuitant's life is the "measuring life." The tables are gender based because women generally live longer. In the case of joint and survivor annuity options, an actuarial table containing both the annuitant's age and the designated survivor's age must be used to calculate the amount of the periodic payments. Example(s): Mr. Smith bought an annuity that now has an accumulation value of Prepared By: Neal Lapierre Page 2 of 8 $50,000. He is now 65 and decides to begin receiving annuity payouts under a life−only settlement option. Using the actuarial tables, Mr. Smith receives a monthly payment in the amount of $334. Mr. Jones, on the other hand, bought an annuity that now has an accumulation value of $50,000. He is now 75 and decides to begin receiving annuity payments under a life−only settlement option. Using the actuarial tables, Mr. Jones receives a monthly payment in the amount of $471. Mr. Lucky bought an annuity that now has an accumulation value of $50,000. He is only 55 when he decides to take early retirement, after which he begins receiving annuity payments under a life−only settlement option. Using the actuarial tables issued, Mr. Lucky receives a monthly payment in the amount of only $265. Who are the parties to an annuity contract? There are generally four parties to an annuity: the issuer, the owner, the annuitant, and the beneficiary. The issuer is the issuing insurance company and is the party that accepts the premiums and promises to pay the benefits under the annuity contract. The owner is generally the purchaser of the annuity, the party who pays the premiums, and, usually, the party that receives the annuity payouts during the distribution phase. The annuitant provides the measuring life for the determination of the annuity payments to be paid. The beneficiary receives the remaining benefits, if any, at the death of the owner. Typically, the owner and the annuitant are the same person. Can there be more than one annuitant? No. Because the annuitant's life is the "measuring life", there can be only one annuitant and the annuitant must be a real person. On the other hand, the owner or beneficiary may be an entity (e.g., a corporation or trust). There may, however, be more than one recipient of the annuity payouts, as in the case of a joint and survivor annuity. Technical Note: We are discussing commercial annuities here. Commercial annuities differ from private annuities , which are contractual arrangements between private parties. How are annuity benefits paid out? Fixed payout If the annuity is a fixed annuity (sometimes referred to as an ordinary annuity), the payout is a fixed Prepared By: Neal Lapierre Page 3 of 8 dollar amount that remains the same throughout the contract period. The fixed payments may be made monthly, yearly, or in some other periodic manner. The cash value accumulation is "annuitized" (i.e., it is converted into a stream of payments). Thus, the payout is guaranteed. This annuitization is computed using actuarial tables that take into account the annuitant's life expectancy and interest earned, as discussed above. Example(s): John buys a fixed annuity from Annuities Unlimited Life Insurance Company. John pays Annuities Unlimited a lump−sum premium of $80,000. Annuities Unlimited agrees to pay John $800 a month for life. Caution: If the insurance company fails, you may lose your investment. Therefore, be sure to check the financial strength of the insurance company before purchasing any annuity policies. Variable payout An annuity payout from a variable annuity fluctuates with the market value of the assets in the account (separate accounts are kept for each contract owner). The amount of the payments is determined by the performance of the investment portfolio. Thus, while the number of variable payments can be determined, the amount is not. Example(s): You have accumulated $300,000 in a variable annuity. When the annuitization phase begins, you elect to receive a variable payout. In the first year, you receive $15,000. In the second year, however, you receive only $13,000 because of the poor performance of your investments in the variable annuity. In the third year, after the investment performance improves, you receive $16,000. The remainder of the payments continues in this fashion. When are annuity benefits paid out? Immediate As the name implies, an immediate annuity is one that has no accumulation period (i.e., it is annuitized and the distribution period begins within 12 months after the purchase). Immediate annuities may be appropriate for people who have an immediate income need. Immediate annuities provide those who have accumulated money in other types of investments an opportunity to still enjoy the benefits of an annuity payout. For instance, an individual who has sold his or her business for a substantial amount of money and would then like to immediately retire may want to purchase an immediate annuity. Immediate annuities are typically purchased upon retirement or sometime thereafter through payment of a single large premium. They appeal to those who prefer the security of a fixed income and who are uncomfortable managing their own investments. Example(s): Steve has just retired as warehouse manager from Glide−Lite, one of the nation's leading running−shoe manufacturers. Glide−Lite has no pension plan, but Steve has built up a retirement nest egg through the company's 401(k) plan and Prepared By: Neal Lapierre Page 4 of 8 an individual retirement account he funded while previously self−employed. Never a whiz with finances, Steve has opted to use part of his retirement savings to purchase an immediate annuity that will guarantee him a monthly income for life. The remainder of his savings will be used to supplement his annuity payout income as needed. Caution: Because immediate annuities are annuitized almost immediately, they are irrevocable. Consequently, their purchase calls for thoughtful consideration and planning. Tip: When a person is less than seven years from retirement, planning to purchase an immediate annuity upon or after retirement may be preferable to buying a deferred annuity. Investment earnings within a deferred annuity need to accumulate for about this long to offset the annuity's management fees. Deferred A deferred annuity is one in which the distribution period will begin at some point in the future (usually more than one year after the purchase of an annuity). Deferred annuities delay the payment of benefits until some future date. A deferred annuity grows through a combination of premiums paid and investment earnings that occur during an accumulation period. The earnings portion grows tax deferred during this time and is taxed upon withdrawal, when your tax bracket is typically lower. Deferred annuities may be appropriate for those who find annuities generally preferable to other retirement savings alternatives. Tip: A single payment annuity may be a deferred annuity. For example, you purchase an annuity for a lump sum of $100,000 and then let the earnings accrue for 10 years before the distribution period begins. Tip: An accumulation period of seven years is generally required to break even on the management and other fees typically charged by companies offering deferred annuities. For shorter accumulation periods, mutual funds may provide better growth for a given investment amount. The investor can then still enjoy annuity payout benefits by purchasing an immediate annuity. Combination A combination annuity is, in reality, two annuities−−one immediate and the other deferred. The immediate annuity is typically designed to distribute all of its proceeds within a fixed number of years, while the deferred portion accumulates earnings tax deferred. After the fixed number of years has passed and when the immediate annuity's proceeds have been exhausted, the deferred portion begins to pay. What payout methods are available? Payments for life Prepared By: Neal Lapierre Page 5 of 8 This method provides the owner with payments for life only, and then they end. Payments can be made monthly, quarterly, semi−annually, or annually. There is no designated beneficiary with this type of policy because the policy terminates at the owner's death. Payments for life with term certain This method provides the owner with payments for life, and, after the owner's death, the payments continue to a named beneficiary for the remainder of the original specified period of time (generally 5, 10, 15, or 20 years). Payments for a specified period This method provides the owner with payments for a specified period of time (generally 5, 10, 15, or 20 years). If the owner dies before the specified time period has elapsed, the remaining payments are received by a named beneficiary. Refund life This method provides the annuitant with income for life, but if the owner dies before the total amount of the annuity is received, the balance is paid to a named beneficiary. The named beneficiary may receive the balance in a lump sum or in installments. Joint and survivor life This method provides two persons with income for life (first one, then the other−−but not both at the same time). When one dies, the other continues to receive the payment (or some portion of it) for life. This may be advantageous if you want to provide for yourself and then someone else (e.g., your spouse) or if you want to provide for others (e.g., your children). Also, because a survivor annuity may pay until the death of the designated survivor, it generally pays for a longer period of time than a single policy. However, because the benefits are expected to pay longer, monthly payments are lower. Typically, spouses purchase joint and survivor annuities, although nonspouses (e.g., elderly siblings) may purchase them as well. A joint and survivor annuity can end at the death of the last person or after a certain number of payouts. Some policies continue to pay the full income to the survivor (this is called a "joint and full to the survivor" policy). Some insurers offer policies that provide one−half or two−thirds of the income to the survivor after the first owner dies (these are called a "joint and one−half" policy or a "joint and two−thirds" policy, respectively). Tip: Joint and survivor annuity may be subject to estate tax. Joint and survivor annuities are included in the first owner's gross estate to the extent of the fair market value of the survivor's interest in the annuity. Options after death Prepared By: Neal Lapierre Page 6 of 8 In addition to different distribution options while the annuitant is alive, many annuities offer different options after the annuitant dies. If the annuitant dies before annuitization begins, typically the funds in the annuity will be distributed to the named beneficiary. If the annuitant dies after annuitization has begun, then, with some annuities (e.g., single life annuities), the periodic payments stop. With a single life annuity, if the annuitant has not completely depleted the money invested in the annuity, then the annuity issuer keeps the difference. However, many annuities also offer distribution options whereby if you die within a certain time period after annuitization begins, your named beneficiary will receive a certain amount from your annuity account. Example(s): You have accumulated $300,000 in a fixed annuity. When the time comes to start receiving payments, you elect to receive payments over your entire lifetime. However, you select a further option offered by the issuer whereby if you die within the first five years of the payout period, the annuity issuer will pay 75 percent of the monies in your annuity account at the time of your death to your named beneficiary. Of course, if you select this option, the annuity issuer pays you a lower amount per year than if you had not elected this option. But now you know that if you die within a short time after annuitization begins, 75 percent of your remaining investment will go to your named beneficiary. Cannot outlive payments to you if you elect to annuitize over your entire lifetime One of the unique features to an annuity is that you cannot outlive the payments from the annuity issuer to you if you elect to receive payments over your entire lifetime. If you elect to receive payments over your entire lifetime, the annuity issuer must make the payments to you no matter how long you live. Even if you begin receiving payments when you are 65 years old and then live to the age of 100, the annuity issuer must make the payments to you for your entire lifetime. The downside to this ability to receive payments for your entire life is that if you die after receiving just one payment, no more payments will be made to your beneficiaries. You have essentially given up control and ownership of the principal and earnings in the annuity. What is the tax treatment of annuity payouts in the annuitization phase? Each annuity payment is part nontaxable return of investment in the contract and part payment of accumulated earnings (until the investment in the contract is exhausted). Generally, only the portion of the payment that represents payments of accumulated earnings is subject to income tax. To determine the amount of each annuity payment treated as a nontaxable return of investment in the contract, divide the investment in the contract (i.e., premiums paid) by the expected return (i.e., premiums paid plus investment income) and multiply this amount by the amount of the annuity payment. For annuity contracts where the annuity starting date is after December 31, 1986, after the investment in the contract is fully recovered, all subsequent annuity payments are treated as coming entirely from taxable earnings. For more information, see the discussion on Taxation of Annuities . Prepared By: Neal Lapierre Page 7 of 8 Prepared By: Neal Lapierre Page 8 of 8