E15-18 (Dividends and Stockholders` Equity Section) Anne Cleves

advertisement

Anne Cleves")

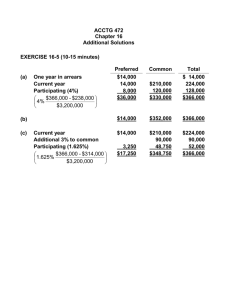

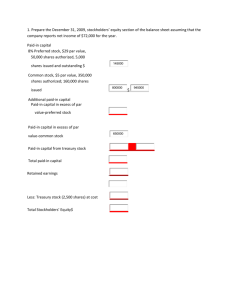

E15-18 (Dividends and Stockholders’ Equity Section) Anne Cleves Company reported the following amounts in the stockholders’ equity section of its December 31, 2006, balance sheet. Preferred stock, 10%, $100 par (10,000 shares authorized, 2,000 shares issued) $200,000 Common stock, $5 par (100,000 shares authorized, 20,000 shares issued) 100,000 Additional paid-in capital 125,000 Retained earnings 450,000 Total $875,000 (L0 4, 7, 8) (L0 6, 7, 8) During 2007, Cleves took part in the following transactions concerning stockholders’ equity. 1. Paid the annual 2006 $10 per share dividend on preferred stock and a $2 per share dividend on common stock. These dividends had been declared on December 31, 2006. 2. Purchased 1,700 shares of its own outstanding common stock for $40 per share. Cleves uses the cost method. 3. Reissued 700 treasury shares for land valued at $30,000. 4. Issued 500 shares of preferred stock at $105 per share. 5. Declared a 10% stock dividend on the outstanding common stock when the stock is selling for $45 per share. 6. Issued the stock dividend. 7. Declared the annual 2007 $10 per share dividend on preferred stock and the $2 per share dividend on common stock. These dividends are payable in 2008. Instructions (a) Prepare journal entries to record the transactions described above. (b) Prepare the December 31, 2007, stockholders’ equity section. Assume 2007 net income was $330,000. (a) 1. 2. 3. 4. 5. Dividends Payable—Preferred (2,000 X $10) ................................. 20,000 Dividends Payable—Common (20,000 X $2) .................................. 40,000 Cash.................................................................................... 60,000 Treasury Stock ............................................................................ 68,000 Cash (1,700 X $40) ............................................................ 68,000 Land ............................................................................................. 30,000 Treasury Stock (700 X $40) ............................................. Paid-in Capital From Treasury Stock ............................ Cash (500 X $105) ....................................................................... 52,500 Preferred Stock (500 X $100) .......................................... Paid-in Capital in Excess of Par— Preferred ........................................................................ Retained Earnings (1,900* X $45) ............................................. 85,500 Common Stock Dividend Distributable (1,900 X $5)..................................................................... Paid-in Capital in Excess of Par— Common ......................................................................... 28,000 2,000 50,000 2,500 9,500 76,000 *(20,000 – 1,700 + 700 = 19,000; 19,000 X 10%) 6. 7. Common Stock Dividend Distributable .................................... 9,500 Common Stock .................................................................. Retained Earnings....................................................................... 66,800 Dividends Payable—Preferred (2,500 X $10)................................................................... Dividends Payable—Common (20,900* X $2)................................................................. 9,500 25,000 41,800 *(19,000 + 1,900) (b) Anne Cleves Company Stockholders’ Equity December 31, 2007 Capital stock Preferred stock, 10%, $100 par, 10,000 shares authorized, 2,500 shares issued and outstanding Common stock, $5 par, 100,000 shares authorized, 21,900 shares issued, 20,900 shares outstanding Total capital stock Additional paid-in capital Total paid-in capital Retained earnings Total paid-in capital and retained earnings Less: Cost of treasury stock (1,000 shares common) Total stockholders’ equity Computations: Preferred stock $200,000 + $50,000 = $250,000 Common stock $100,000 + $ 9,500 = $109,500 Additional paid-in capital: $125,000 + $2,000 + $2,500 + $76,000 = $205,500 $250,000 109,500 359,500 205,500 565,000 627,700 1,192,700 40,000 $1,152,700 Retained earnings: $450,000 – $85,500 – $66,800 + $330,000 = $627,700 Treasury stock $68,000 – $28,000 = $40,000