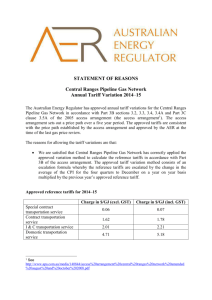

5. Transmission grid tarification in the natural gas sector

advertisement