Here are the Solutions to the FRQs

advertisement

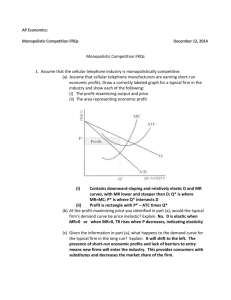

Mr. Maurer AP Economics Name: ____________________________ 2004 Free Response Question (Short) – Monopolistic Competition 1. Assume that a profit-maximizing firm in a monopolistically competitive industry is in longrun equilibrium. (a) Draw a correctly labeled graph that shows the profit-maximizing firm’s price and output. (b) Assume that the city in which this industry operates eliminates the business license fee (a fixed cost) for all firms in this industry. How does the elimination of the license fee affect each of the following for the individual firm in the short run? Explain your answers. (i) output: Output will not change because the elimination of the business license fee will reduce fixed costs (and total costs), but not variable costs or marginal cost. Since output is based on marginal cost, output will not change. (ii) economic profit Economic profit will increase because profit is total revenue minus total cost and the elimination of the business license fee reduces total cost. 2007B Free Response Question (Long) – Monopolistic Competition 1. Assume that the cellular telephone industry is monopolistically competitive. (a) Assume that cellular telephone manufacturers are earning short-run economic profits. Draw a correctly labeled graph for a typical firm in the industry and show each of the following. (i) The profit-maximizing output and price. (ii) The area representing economic profit. (b) At the profit maximizing price you identified in part (a), would the typical firm’s demand curve be price inelastic? Explain. No, the typical firm’s demand curve would be elastic at the profit-maximizing price because marginal revenue is positive in this portion of the demand curve, so total revenue increases as price decreases. (c) Given the information in part (a), what happens to the demand curve for the typical firm in the long-run? Explain. If a monopolistically competitive firm is earning economic profit, in the long run, the demand curve for the typical firm will shift to the left (or down) as new firms enter the industry to take advantage of these short-run profits. These new competing firms take some of the existing firm’s market share and so reduce demand for its product. (d) Using a new correctly labeled graph, show the profit-maximizing output and price for the typical firm in the long-run. (e) Does the typical firm produce at an output level that minimizes its average total cost in the long-run? No. (f) In long-run equilibrium, does the typical firm produce the allocatively efficient level of output? Explain. No, because price is greater than marginal cost. 2009B Free Response Question (Long) – Monopolistic Competition 1. Mary & Company, operating in a monopolistically competitive industry, produces a cleaning product called BriteKlean. The company currently produces the profit-maximizing quantity of BriteKlean but is operating at a loss. (a) Draw a correctly labeled graph for Mary & Company and show each of the following. (i) The profit-maximizing output and price, labeled as QM and PM, respectively (ii) The area of loss, shaded completely (b) What must be true in the short run for the company to continue to produce at a loss? Price must be greater than Average Variable Cost. (c) Assume now that the demand for cleaning products increases and that the company is now earning short-run economic profits. Relative to this short-run situation, how does each of the following change in the long run? (i) The number of firms The number of firms will increase. (ii) The company’s profit The company’s profit will decrease, reaching zero economic profit in the long-run. (d) In the long run, if the company continues to produce, will it produce the allocatively efficient level of output? Explain. No. Price for a monopolistically competitive firm will always be greater than marginal cost, so allocative efficiency is not attained. (e) In the long run, will the company be operating in a region where economies of scale exist? Explain. Yes, because long-run average total cost is decreasing at the company’s profit-maximizing level of output.