Chapter 15

advertisement

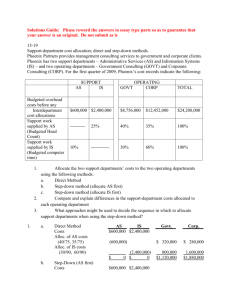

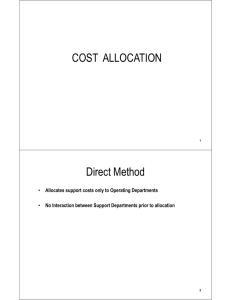

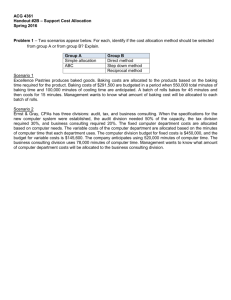

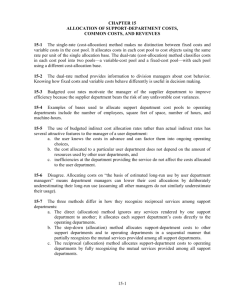

CHAPTER 15 Allocation of Support Department Costs Allocating Costs of a Support Department to Operating Departments • Support (service) department—provides the services that assist other internal departments in the company • Operating (production) department—directly adds value to a product or service Methods to Allocate Support Department Costs • Single-rate method—allocates costs in each cost pool (service department) to cost objects (production departments) using the same rate per unit of a single allocation base – No distinction is made between fixed and variable costs in this method. Methods to Allocate Support Department Costs • Dual-rate method—segregates costs within each cost pool into two segments: a variablecost pool and a fixed-cost pool. • Each pool uses a different cost-allocation base. Allocation Method Trade-Offs • Single-rate method is simple to implement, but treats fixed costs in a manner similar to variable costs. • Dual-rate method treats fixed and variable costs more realistically, but is more complex to implement. An Example Allocation Based on the Demand for (Usage of) Computer Services The Central Computer Department costs are allocated to the two divisions on the basis of actual hours used: Allocation Based on the Demand for (Usage of) Computer Services Dual-Rate Method Allocation Based on Supply of Capacity Allocation Based on Supply of Capacity Methods of Allocating Support Costs to Production Departments 1. Direct 2. Step-down 3. Reciprocal Data Used in Cost Allocation Illustrations Direct Method • Allocates support costs only to operating departments. • Direct method does not allocate supportdepartment costs to other support departments. Direct Allocation Method Illustrated Direct Allocation Method Illustrated Step-Down Method • Also called the sequential allocation method • Allocates support-department costs to other support departments and to operating departments in a sequential manner • Partially recognizes the mutual services provided among all support departments Step-Down Allocation Method Illustrated Step-Down Allocation Method Illustrated Reciprocal Method • Allocates support-department costs to operating departments by fully recognizing the mutual services provided among all support departments. • Reciprocal method fully incorporates interdepartmental relationships into the supportdepartment cost allocation. Reciprocal Allocation Method (Repeated Iterations) Illustrated Linear Equations Linear Equations (cont) Linear Equations (cont) Reciprocal Allocation Method Illustrated Reciprocal Allocation Method Illustrated Confusion? A Comparison of the Methods