Annuities

advertisement

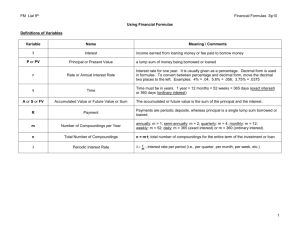

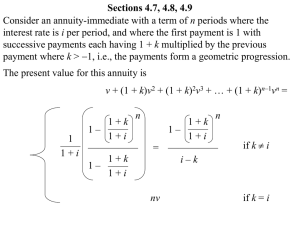

Basics Annuities are streams of payments, in our case for a specified length Boil down to geometric series (1 − 𝑟 # 𝑜𝑓 𝑡𝑒𝑟𝑚𝑠 ) 𝑆𝑢𝑚 = 𝐹𝑖𝑟𝑠𝑡 𝑡𝑒𝑟𝑚 ∗ (1 − 𝑟) Two main formulas 𝑛 1 − 𝑣 𝑎𝑛 = 𝑣 + 𝑣 2 + ⋯ + 𝑣 𝑛 = 𝑖 𝑠𝑛 = (1 + 𝑖)𝑛−1 (1 + 𝑖)𝑛 − 1 + ⋯+ 1+ 𝑖 + 1 = 𝑖 For annuities due (double dots), simply change denominator from i to d Once again, if unsure make a TIMELINE 𝑎𝑛 = (1 + 𝑖)𝑎𝑛 =1+𝑎𝑛−1 𝑠𝑛 = (1 + 𝑖)𝑠𝑛 =𝑠𝑛+1 − 1 Deferred Annuities Annuity with the whole series of payments pushed back No need to know formulas, just use TVM factors to shift Perpetuities No new formulas, just plug in infinity for n in the originals 𝑎∞ 1 = 𝑖 𝑎∞ 1 = 𝑑 Interestingly, this leads to 1 1 − =1 𝑑 𝑖 Annuities with off payments 1st method- Find equivalent interest rate for payment period This is the easiest/quickest, so use this if possible 1 + 𝑗 = (1 + 𝑖)𝑛 2nd Method- More complicated, but may have to use if you are only given symbols Multiple payments during interest pd- mthly annuity Mthly annuity- divide by # payments and use i^(m) 𝑎(𝑚 ) 𝑛 1 − 𝑣𝑛 = (𝑚 ) 𝑖 Multiple interest pds per payment- split up payments (show) Varying Interest For whatever reason, the interest environment is going to change partway through your series of payments Find accumulated value of first set (up until interest changes), then compound these payments using new rate for the rest of the time. Add to this the accumulated value of the next set of payments Example: We get a ten year annuity immediate. For the first four years, interest is 5%. After this, interest decreases to 4%. What is the accumulated value of this annuity? More Annuities If payable continuously, continue pattern and change i to δ 1 − 𝑣𝑛 = = 𝛿 𝑎𝑛 𝑛 𝑣 𝑡 𝑑𝑡 0 Double dots and upper m’s cancel 𝑎(𝑚 ) 𝑥 𝑎𝑥 𝑎(𝑚 ) 𝑥 𝑎𝑥 = = (𝑚 ) = (𝑚 ) 𝑎𝑦 𝑎𝑦 𝑎 𝑦 𝑎 𝑦 If payments vary continuously and/or interest varies continuously (unlikely) 𝑛 𝑃𝑉 = 0 𝑓(𝑡)𝑒 𝑡 0 𝛿𝑟𝑑𝑟 𝑑𝑡 Arithmetic progression General formula- annuity of first payment plus increasing annuity of the common difference 𝐴 = 𝑃𝑎𝑛 (𝑎𝑛 − 𝑛𝑣 𝑛 ) +𝑄 𝑖 This leads to 3 other forms by bringing through time (show) From these, you can derive all 4 increasing/decreasing formulas (show) Geometric Progression Can usually figure out using geometric series, without any special formulas Calculator Highlights Beg/End option Always clear TVM values and check beg/end, compounding, etc options Problems A man turns 40 today and wishes to provide supplemental retirement income of 3000 at the beginning of each month starting on his 65th birthday. Starting today, he makes monthly contributions of X to a fund for 25 years. The fund earns a nominal rate of 8% compounded monthly. Each 1000 will provide for 9.65 of income at the beginning of each month on his 65th birthday until the end of his life. Calculate X. ASM p.121, #1 Answer: 324.73 To accumulate 8000 at the end of 3n years, deposits of 98 are made at the end of each of the first n years and 196 at the end of each of the next 2n years. The annual effective rate of interest is i. You are given (1+i)^n=2.0 Determine i. ASM pg. 136 Answer: 12.25% Dottie receives payments of X at the end of each year for n years. The present value of her annuity is 493. Sam receives payments of 3X at the end of each year for 2n years. The present value of his annuity is 2748. Both present values are calculated at the same annual effective interest rate. Determine v^n. ASM p.150, #2 Answer: .858 A loan of 10,000 is to be amortized in 10 annual payments beginning 6 months after the date of the loan. The first payment, X, is half as large as the other payments. Interest is calculated at an annual effective rate of 5% for the first 4.5 years and 6% thereafter. Determine X. ASM p.167 Answer: 655.70 Kathryn deposits $100 into an account at the beginning of each 4-year period for 40 years. The account credits interest at an annual effective interest rate of i. The accumulated amount in the account at the end of 40 years is X, which is 5 times the accumulated amount in the account at the end of 20 years. Calculate X. ASM p.179 Answer: 6,195 Olga buys a 5-year increasing annuity for X. Olga will receive 2 at the end of the first month, 4 at the end of the second month, and for each month thereafter the payment increases by 2. The nominal interest rate is 9% convertible quarterly. Calculate X. ASM p.219 Answer: 2,729 A perpetuity-immediate pays 100 per year. Immediately after the fifth payment, the perpetuity is exchanged for a 25-year annuity-immediate that will pay X at the end of the first year. Each subsequent annual payment will be 8% greater than the preceding payment. Immediately after the 10th payment of the 25-year annuity, the annuity will be exchanged for a perpetuity-immediate paying Y per year. The annual effective rate of interest is 8%. Calculate Y. ASM p.228 Answer: 54 A continuously increasing annuity with a term of n years has payments payable at an annual rate t at time t. The force of interest is equal to 1/n. Calculate the present value of this annuity. ASM pg. 257, #4 Answer: