Export Refinance under Islamic Banking

advertisement

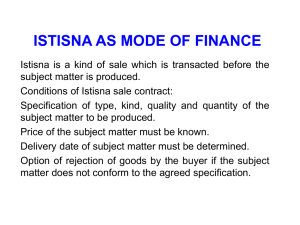

Financing under Islamic Export Refinance Scheme Muhammad Faisal Shaikh Head, Product & Business Development BankIslami Pakistan Limited Shawwal 24, 1433 A.H Septemeber 12, 2012 Introduction Alhamdolillah Islamic Banking and Finance has gained momentum during the last couple of years. Product Developer in Islamic Banking have developed alternate products for almost all kind of services required by the businesses. Similarly different products are being used to finance Exporters under Islamic Export Refinance Scheme (IERS). Introduction The most common Product is which is being used is Murabahah. A few banks are using Istisna to provide financing under IERS. MURABAHAH Murabahah Islam prohibits charging fixed interest on money, but obligates to charge fixed profit on trading of goods. Islamic Banks use Murabahah based trade transactions to finance purchase of assets by their customers, especially for working capital financing requirements. A large portion of all business volume of Islamic banks comprises of Murabahah based transactions. Murabahah Murabahah is a particular kind of sale. the transaction is done on a “cost plus profit” basis i.e. the seller discloses the cost to the buyer and adds a known profit to it to arrive at the final selling price. Where The distinguishing ordinary sale is feature of Murabahah The seller discloses the cost to the buyer And a known profit is added from Murabahah As per the rules of Shariah, the seller cannot sell the goods unless they come into his ownership. However, since the bank cannot deal in the commodity markets, the bank may appoint the customer its agent to procure the goods on its behalf. Murabahah Once the customer purchases the goods, the risk of the goods transfers to the Bank. Bank can now sell these goods to the customer. Please note that the customer plays two different roles in this transaction. One that of Bank’s agent and other of purchaser. These roles should be clearly segregated to make the transaction halal. This process is explained in detail in slides ahead. Murabahah Step by Step Murabahah Financing 1. Client and Bank sign Main Murabahah Facility Agreement (an agreement to enter into Murabahah). Main Murabahah Facility Agreement Bank Client Murabahah Step by Step Murabahah Financing 2. Client appointed as Bank’s agent to purchase goods on Bank’s behalf. Main Murabahah Facility Agreement Bank Client Agency Agreement Murabahah Step by Step Murabahah Financing 3. In advance payment Murabahah cases, Bank gives money to Client for purchase of goods from Supplier. Main Murabahah Facility Agreement Bank Client Agency Agreement Disbursement to the supplier or agent Supplier Murabahah Step by Step Murabahah Financing 4. Client purchases goods on Bank’s behalf from Supplier and takes their possession. Transfer of Risk Bank Supplier Delivery of goods Agent Murabahah Step by Step Murabahah Financing 5. Client makes an offer to purchase goods from the Bank. Bank Client Offer to purchase Murabahah Step by Step Murabahah Financing 6. Bank accepts the offer and sale is concluded. Bank Client Murabaha Sale Document Murabahah Step by Step Murabahah Financing 7. Client pays agreed price to Bank according to an agreed Schedule, usually on a deferred payment basis (Bai Muajjal). Bank Client Payment of Price Murabahah Application: Murabahah can be used to finance purchase of any asset which is recognized as Mal-e-Mutaqawam (valuable) as per Shariah and possess tangible form. ISTISNA' Istisna' DEFINITION It is an order from purchaser (buyer) to a producer (seller) to manufacture a specific commodity for him (buyer) against mutually agreed price and period for manufacturing and delivery. ISTISNA GOODS Goods are not Agricultural yield instead, they are manufactured products. Istisna' CONTRACT PRICE All business contracts of production (i.e. manufacturing, construction and assembling etc.) and value addition (i.e. processing and packaging etc.) can be executed through Istisna transaction. Istisna contract price can be paid by the buyer in advance, in tranches or at the time of delivery of goods. Similarly, Istisna goods can be delivered by the manufacturer in one consignment or in tranches. Istisna'-Features SUBJECT MATTER (ISTISNA GOODS) The subject matter of Istisna transaction should be a thing which requires production or value addition. For example; Manufacturing Leather jackets Cement Assembling Assembling of vehicles Machineries Istisna'-Features SUBJECT MATTER (ISTISNA GOODS) Construction Building Highways Value Addition Packaging Cotton bales for certain specifications i.e. type, kind, quality and quantity Subject matter should be identified unambiguously. Istisna'-Features CONTRACT PRICE Contract Price of Istisna may be tied up with the time of delivery. The price may be decreased by an agreed amount (per day or otherwise) in case the manufacturer delays the delivery of the subject matter. Similarly, price may be increased by an agreed amount (per day or otherwise) in case manufacturer delivers the goods earlier. NOTE: Any decrease/increase in the contract price should be agreed upon at the time of entering into Istisna contract. Istisna'-Features CONTRACT PRICE: Istisna Contract Price can be paid in advance, in installments or at the time of delivery of goods. Buyer can also connect payment of price with stages of completion of the work. The parties agree that the goods would be manufactured against the agreed contract price. Istisna'-Applications Unlike Murabahah, Istisna can fulfill all working capital requirements of the Corporate/SME clients i.e. for payment of overheads, salaries, utility bills etc. Istisna transactions should be executed by Islamic Banks only after proper risk mitigation. Istisna'-Applications Following are some of the cases where Istisna is possible: Short-term financing for manufacturers; Financing purchase of certain intangible assets, such as electricity and gas; Manufacturing of plant/ machinery and equipment; Real Estate Finance (construction of residential and commercial buildings); Infrastructure financing, construction of buildings, hospitals, highways, bridges, government projects; Assembling of machinery/assets; Development of IT System. Istisna'-Applications Istisna may be used as a mode of financing in a case where client requires funds to meet running cost of its business. For the purpose of financing using Istisna transaction, Islamic Bank will have to place an order with the Corporate or SME Client to manufacture specified goods for itself (Islamic Bank) against agreed Istisna contract price. This contract price will be the financing amount from Islamic Bank to its client. Istisna'-Applications Islamic Bank will be buyer and the client will be seller/manufacturer. The price may be paid by Islamic Bank completely in advance or in tranches. Whereas, the client will agree to deliver the goods on agreed Delivery Date(s). As a result of Istisna transaction, Islamic Bank will receive certain goods rather than cash amount from the Client. Murabahah- Istisna Financing Murbahah -Istisna' Financing Customer especially exporters some times needs financing for processing of raw material. In Pakistan textile composite units purchase cotton to manufacture finished cloth, these unit cannot rely on Murabahah Finance, since their main raw material also include labor and overhead expenses. Murabahah alone cannot fulfill their requirements. Murbahah -Istisna' Financing These exporters can be financed using the following Islamic Financing instruments: A Istisna Murabahah Wakalah step by step process in discussed next Murbahah -Istisna' Financing Having the LC in hand, the exporter primarily needs funds to Purchase To raw material manufacture the finished product The Bank fulfills the need of the exporter by providing funding Murbahah -Istisna' Financing This funding is provided under the following two agreements: Murabahah Istisna Murabahah Istisna goods is provided for purchase of Raw Material is provided to manufacture the required Murbahah -Istisna' Financing The process will consist of the following steps 1. The Bank will finance the purchase of Raw Material through a Murabahah transaction. 2. It will also give funds to the customer under a separate Istisna agreement to manufacture and deliver the goods to the bank as per the LC. 3. Once the goods are manufactured they will become the property of the Bank. (Contd..) Murbahah -Istisna' Financing 4. The Bank will appoint the exporter as its agent to export the goods on its behalf under a Wakalah agreement. 5. The Wakalah agreement is required because under Istisna the customer is liable to deliver goods to the bank. 6. The exporter will now export the goods, acting as the Bank’s agent. Murbahah -Istisna' Financing 7. The export proceeds will be remitted to the Bank 8. Which will deduct from the proceeds The cost of goods ( Istisna price) And profit 9. Client will pay Murabahah price to the Bank. Graphical flow of the new process is explained next. Exporter Request for financing Islamic Bank Exporter Murabahah Facility for purchase of Raw Material Islamic Bank Exporter Istisna Facility to manufacture goods Islamic Bank Exporter Agreement to Wakalah Islamic Bank Exporter Delivery of Goods manufactured under Istisna Islamic Bank Exporter Wakalah Agreement Islamic Bank Exporter Islamic Bank Goods Exported Importer Exporter Islamic Bank Remittance of Export Price Importer Islamic Bank Islamic Bank will deduct the cost of goods from the export proceeds and will pay the balance as bonus to the exporter Exporter Payment of Murabahah Price Islamic Bank Challenges Awareness & R&D services Skill set of product development team and utilization of tools Shariah Issues and availability of the structures and collaterals The Alignment of Business Sense with Shariah Board Mind set of the management ... Is it Business oriented & Shariah IT infrastructure Product Structuring Issues 47 Challenges-Industry Level A challenge to move from a Shariah confirming Business to a Sharia Based Business… A challenge to move from a Shariah confirming Product to a Shariah Based Product… ...And whosoever fears Allah and keeps his duty to Him, He will make his matter easy for him... (Surah Al Talaq Ayat 04) .