Update - Philippines Development Forum

advertisement

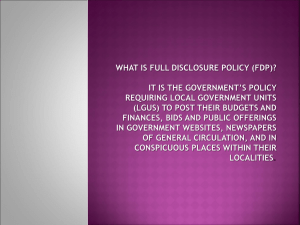

THE REVIEW OF THE 1991 LOCAL GOVERNMENT CODE Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services Results of Nationwide Consultations on the Review of the Local Government Code of 1991 Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services Result of Consultations Island-wide consultations in Luzon, Visayas and Mindanao attended by close to 400 LGU chief executives, council members, and officers Smaller meetings with selected officials of Leagues of Provinces, Cities, Municipalities, Vice Governors, Councilors, Vice Mayors, ULAP, Provincial Board Members Meetings with technical staff of ULAP, League of Provinces, League of Cities and League of Municipalities Consultations with business sector (PCCI, TMAP, BAP, BPO sector, etc.) Initial consultations with national government agencies Scope of LGC Review 1. 2. 3. 4. 5. 6. 7. Expenditure assignment Revenue assignment and taxing powers Intergovernmental fiscal transfers LGU borrowing and credit finance Creation of LGUs Inter-local cooperation/alliances Fiscal administration 1. Expenditure Assignment Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services Expenditure Assignment – who does what? Issue: Overlapping and, at times, unclear assignment of functions across various levels of government (NG and different levels of LGUs) Results in waste of resources Unfunded mandates Results in relevant services not being delivered at all or not delivered in sufficient quantities In either case, the welfare of local communities is adversely affected. Expenditure Assignment – who does what? Proposed amendment Amend Section 17 (a) of the 1991 LGC by inserting a proviso that will differentiate between fully devolved functions and delegated functions o Fully devolved functions are those for which exclusive responsibility for service provision is assigned to. o Delegated functions are those for which the national government has primary responsibility for provision but which are implemented by LGUs; delegated functions typically associated with national objectives and/ or externalities Delegated functions are best financed through conditional transfers Stakeholder support Consistent with PFM reform of NG; Strong support in principle from LGUs in Luzon, Visayas and Mindanao consultations; League officials want to see details of delineation * Studies now on-going with respect to functional assignment in health, environment and natural resources; study on agriculture to follow. 2. Own-Source Revenues and Revenue Assignment Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services Own-source revenues and revenue assignment Overarching issues Lack of productive source of local revenues ► high LGU dependence on transfers ► weak revenue autonomy ► perverse incentives and weak accountability Wide flexibility in taxes/ fees that LGUs are allowed to impose ► discourages prospective investors in local economy Revenue assignment - Schedule of market value (SMV) of real property Specific issue Outdated schedule of fair market value of real property in many provinces and cities o SMV at least 2 cycles behind in 59% of provinces & 72% of cities in 2014 Need to strengthen real property valuation standards to promote integrity and fairness of RPT system Revenue assignment - SMV Proposed Amendment Amend Sections 212 and Section 214 so as to assign the approval of the schedule of market values of real properties situated in each province/ city/ MM municipality to the Department of Finance instead of requiring that schedule of market value be enacted into an ordinance by the local Sanggunians Retain LGUs’ autonomy in setting assessment levels for RPT purposes (Section 218) and setting real property tax rates (Sections 232, 233, 235 and 236) Revenue assignment - SMV Impact If SMVs of all provinces and cities were to be fully updated, potential RPT revenues for all provinces in the aggregate will increase by 97% (or PhP 9.6 billion) while RPT revenues for all cities as group will increase by 138% (or PhP 40.8 billion) for a total of PhP 50.3 billion, other things being equal Stakeholder support DOF priority bill strong support from LGUs in Visayas and Mindanao consultations o LCP National Assembly passed resolution support this proposal General support from business sector Number of bills filed in Congress (e.g., Sarmiento bill) 3. Intergovernmental Fiscal Transfers Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services Intergovernmental Fiscal Transfers – IRA increase Issue Perception on part of LGUs that IRA does not provide sufficient resources needed for LGUs to deliver fully devolved services Proposed amendment (from LGU consultations) Amend Sec. 284 of LGC such that the IRA shall be set equal to 40%-50% of all national taxes (i.e., including collections of both BIR and BOC in the base) Intergovernmental Fiscal Transfers – IRA increase Impact Incremental revenue impact (based on actual NG tax collections in 2012) o Inclusion of VAT/ excise tax collections of BOC in base (Mandanas petition) – PhP 98.5 billion o 50% of BIR collection – PhP 97.3 billion o 50% of national internal revenue taxes incl. VAT/ excise tax collections of BOC – PhP 122 billion o 50% of all national taxes – PhP 245 billion Significant implications on macroeconomic flexibility Demand for increase may be mitigated by increase in LGU taxing powers Stakeholder support Very strong support from LGUs Many bills in House and Senate Mandanas petition pending at SC Opposition from DOF Intergovernmental Fiscal Transfers – Equalization grant Issue IRA does not assist fiscal equalization in the sense of providing more resources to LGUs with lower revenue capacity relative to their needs and less to LGUs with greater revenue capacity relative to their needs Proposed amendment Amend Section 3 (d) to specifically introduce principle that share of LGUs in national taxes shall take into account disparities in revenue raising capacity of LGUs in line with their expenditure needs (i.e., have equalization as an objective) Intergovernmental Fiscal Transfers – Equalization grant Impact can be designed and implemented in a marginal and sequential manner so as not to harm any LGU in the process and without impacting negatively on NG flexibility If distribution is calibrated relative to revenue capacity as measured by potential revenue, it will incentivize ownrevenue generation Stakeholder support Support from LGUs in Luzon, Visayas and Mindanao consultation 4. LGU Borrowing and Credit Finance Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services LGU Borrowing and Credit Finance Overarching issues Subnational borrowing important if LGUs are to be enabled to finance lumpy investments on local infrastructure At present, subnational borrowing is low relative to LGU financing for local infrastructure o Need to streamline procedures governing LGU access to credit market LGU Credit Finance – LGU deposits in PFIs Issue Preference for gov’t financial institutions as LGU depository bank (Section 311 of LGC) ► discourages entry of private institutions in LGU credit market o Greater competition has potential to reduce LGU borrowing cost Proposed amendment Amend Sec. 311 so as to explicitly allow LGUs to open depository account in PFIs if LGUs will be borrowing from PFIs without any need for prior government approval Stakeholder support Strong support from LGUs in Luzon, Visayas and Mindanao Some support from business sector DOF does not support this Inter-LGU Alliances /Cooperation Issues Inter-LGU cooperation deemed necessary and critical when delivery of devolved service involves: o economies of scale (e.g., solid waste management, water supply) o externalities or spillover effects (e.g., coastal resource management, environmental management) Attempts at inter-LGU cooperation to date have been hamstrung by questions related to how they will manage funds they have contributed to the alliance, how they can access financing from both credit and capital markets, etc. Inter-LGU Alliances /Cooperation Proposed amendment Establish regulatory framework for inter-local cooperation and alliances; register ILCs in a National Registry to vest ILC with legal personality Stakeholder support Some support from LGUs in Luzon an Mindanao consultation 6. Creation of LGUs Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services Creation of LGUs Issues Growing trend in favor of… o conversion of municipalities to cities o Breaking up of existing provinces/ municipalities/ barangays into two or more new provinces/ municipalities/ barangays Such a trend tends to result in inefficiently sized jurisdictions Proposed amendment Align income requirements for the creation/conversion of highly urbanized city, province and municipality with that in RA 9009 which provides new income criteria for the creation of cities Stakeholder support Support from LGUs in Luzon, Visayas and Mindanao 7. Local Fiscal Administration Improving Lives Through Local Governance Reform: Transparency, Accountability and Better Services Local Fiscal Administration (1) Issue Need to ensure transparency in LGU operations for greater accountability Proposed Amendment Legislate full disclosure policy for LGUs requiring them to post documents relating to income, expenditures, procurement, loans, etc. in conspicuous places for transparency Stakeholder support Strong support from LGUs in Luzon, Visayas and Mindanao consultation House bill file in Congress Local Fiscal Administration (2) Issues Need to promote PFM by strengthening internal control Proposed Amendment Amend Sec. 47 (b) to exclude “internal audit” from functions of Accountant; Insert Section on the creation of Internal Audit Service as a mandatory position Stakeholder support Supported by DBM Some support from LGUs Thank you very much!